Report to the Congress on the Availability of Credit to Small Businesses

Submitted to the Congress pursuant to section 2227 of the Economic Growth and Regulatory Paperwork Reduction Act of 1996

October 2007

Contents

- Executive Summary

- Flows and Terms of Business Credit

- Credit Use by Small Businesses

- Providers of Credit Lines, Loans, and Leases to Small Businesses

- Special Issues

- Appendix: The 2003 Survey of Small Business Finances

- References

- Footnotes

Executive Summary

Section 2227 of the Economic Growth and Regulatory Paperwork Reduction Act of 1996 requires that, every five years, the Board of Governors of the Federal Reserve System submit a report to the Congress detailing the extent of small business lending by all creditors. The act specifies that the study should identify factors that give policymakers insight into the small business credit market, including the demand for credit by small businesses, the availability of credit, the range of credit options available, the types of credit products used, the credit needs of small businesses, the risks of lending to small businesses, and any other factors that the Board deems appropriate.1

Since 2002, the year of the previous report on the availability of credit to small businesses, financing flows to both large and small firms have generally increased along with economic activity. From 2002 through June 2007, credit conditions were favorable for small and large firms, and there is no evidence that creditworthy borrowers faced substantial credit supply constraints during that period.2 More recently, financial markets have been volatile, but financing conditions for small businesses appear to have held up fairly well. The demand for credit by small businesses generally tracked the pattern of debt growth for nonfinancial businesses: Indicators of small business financing needs suggest that demand picked up in 2004 from low levels in 2003 but moderated in 2006 and early 2007. Equity financings, although well below their record pace of the late 1990s, have been solid and have steadily increased since 2003.

Small businesses--generally defined as firms having fewer than 500 employees--contribute significantly to the strength and vigor of the U.S. economy. Together they employ more than one-half of private-sector workers and produce more than one-half of the private-sector output. Large and successful companies often begin as smaller firms that prosper and grow. Likewise, most of the new firms that form and help the economy adapt to change start as small businesses.

The concerns of the Congress and other policymaking bodies about small business financing stem from the perception that small firms have more difficulty gaining access to credit sources than do large businesses or other types of borrowers. The source of this difficulty may be that lending to small businesses is generally considered riskier and more costly than lending to larger firms. Small businesses are much more affected by swings in the economy and have a much higher failure rate than larger operations.

In addition, lenders historically have had difficulty determining the creditworthiness of applicants for some small business loans. The heterogeneity across small firms, together with widely varying uses of borrowed funds, has impeded the development of general standards for assessing applications for small business loans and has made evaluating such loans relatively expensive. Lending to small businesses is further complicated by the fact that reliable information on the creditworthiness of a small business is often difficult to obtain because little, if any, public information exists about the performance of most small businesses. Small businesses rarely have publicly traded equity or debt securities, and many small businesses also lack detailed balance sheets and other financial information often used by lenders in making underwriting decisions.

Financial institutions, especially commercial banks, are often portrayed in the economics literature as having an advantage in dealing with information problems. Through interactions with a firm that uses its financial services, the lending institution can obtain additional information about the firm's activities, ownership, financial characteristics, and prospects that is important in deciding whether to extend credit. Employing what is often called "relationship financing," lenders can use information gathered over time through long-term relationships with business owners and other members of the local community to monitor the health of the business and to build appropriate incentives into loan agreements.

The 2003 Survey of Small Business Finances (SSBF) provides the most comprehensive and up-to-date information on small business finance available.3 The survey shows that among small businesses, larger firms were more likely than smaller firms to use each of the traditional credit types: credit lines, capital leases, motor vehicle loans, mortgages, equipment loans, and other loans.4 However, whether this pattern reflects a greater need for credit at larger firms or whether lenders are simply more willing to extend credit to larger firms is unclear. The relationship between firm age and credit use is similar to the relationship between size and use--that is, younger firms use fewer of the credit products.

Patterns of credit use by small businesses observed in data from the 2003 SSBF were similar to the patterns in the 1998 SSBF. The most significant difference was the greater use of lines of credit in 2003 than in 1998, which could be due in part to some financial institutions relying more heavily on credit scoring to evaluate certain loan applications.

Besides having access to traditional sources of credit, small businesses have alternative means of financing available, including credit cards, trade credit, and owner loans. Among these alternatives to traditional credit products, only business credit cards registered an appreciable increase in usage between 1998 and 2003. Although most small firms used credit cards and trade credit, the rapid payment of outstanding balances by a large percentage of these firms suggests that much of the use of these products was for convenience rather than for longer-term financing of expenses.

Some small businesses may have wanted to use more credit than was reflected on the 2003 SSBF but were unable to obtain it. Credit application behavior and denial and approval patterns provide information on the credit demands of small firms. According to the 2003 SSBF, slightly more than one-fifth of small businesses applied for new credit between 2000 and 2003. Larger firms were more likely than small firms to apply for new credit and were more likely to have their applications approved. Application rates for younger and older firms were similar, but younger firms were more likely than older firms to be denied credit. The finding that smaller and younger firms have their loan applications denied more frequently is consistent with the conventional wisdom that these firms are riskier, have shorter credit histories or less collateral to pledge as security, and are more informationally opaque.

Some firms that may have wanted additional credit may not have applied because they expected that their applications would be denied. In fact, 18 percent of the SSBF respondents indicated that, between 2000 and 2003, they had forgone applying when they needed credit because they expected to be turned down. The survey data show that younger and smaller firms were more likely to forgo applying for credit, a sign that the demand for credit at such firms may have been higher than the data on credit use indicate. However, some firms that failed to apply at some point between 2000 and 2003 were not shut out of the credit market because they often applied for, and sometimes received, credit at other times.

Small businesses obtain credit from a wide range of sources, including commercial banks, savings institutions, credit unions, finance companies, nonfinancial firms, and individuals such as family members or friends. According to the 2003 SSBF, of these sources, commercial banks are the leading provider: They supplied credit lines, loans, and leases to slightly more than two-thirds of small firms that obtained a traditional form of credit from any source. Banks were also the most common source of credit lines, mortgages, and equipment loans, and they were the second most common source, after finance companies, of automobile loans.

Because banks are the leading source of traditional credit to small business, much attention has been paid to developments in banking that may influence credit availability. The substantial consolidation of the banking industry over the past twenty years is one such development. Mergers and acquisitions have dramatically reduced the number of banks, thereby increasing the importance of large institutions and the concentration of industry assets. These changes to the structure of the industry have raised concerns about possible reductions in the availability of credit to small businesses. Although larger banks supply the majority of bank loans to small businesses, they tend to be proportionately less committed than smaller banks to small business lending.

The evidence suggests that the thousands of small banks still in operation continue to account for a meaningful share of small business lending activity--measured by holdings of business loans equal to or less than $1 million and equal to or less than $100,000--despite their declining numbers and the commensurate fall in their share of industry assets.5 For example, in 2006, banks with assets of $250 million or less accounted for 73.1 percent of all banking organizations but only 5.4 percent of all banking assets. However, they held 16 percent of bank business loans of $1 million or less and 21.3 percent of such loans of $100,000 or less. In addition, the results of studies that directly analyze the relationship between bank consolidation activity and the availability of credit to small businesses tend to suggest that although mergers and acquisitions may sever existing bank-firm relationships and may introduce some short-term uncertainty, overall they have not reduced credit availability to small businesses. After a merger, any reduction in small business lending by the newly consolidated bank is generally offset by an increase in small business lending by other banks.

Analysis of patterns within local areas is likely to capture the relevant structural conditions that face small firms seeking credit and that influence the level of competition in the market for small business loans. Data from the SSBF indicate that small businesses tend to obtain loans, leases, and lines of credit from providers located near them. For example, in 2003, the median distance between a small business and its lender was 11 miles, and in 66 percent of all business lending relationships the lender was located within 30 miles of the firm's headquarters. Among lending relationships with banks and thrifts of all sizes, the median distance between a small business and its depository institution was 4 miles, and 83 percent of lenders were located within 30 miles of the firm's headquarters. The proximity offers small firms convenient access to their lenders and suggests that credit providers focus their lending activities on entities with which they are familiar, partly because such entities are nearby.

Measures of the concentration of local banking markets are used to assess the likely competitive conditions that face small businesses seeking credit. In 2006, the average urban market was moderately concentrated with respect to banking deposits and had an average of twenty-eight banks with 193 offices.6 The average rural area had fewer banks and was highly concentrated. However, comparing these statistics with those of earlier years, we find that despite the significant amount of consolidation in the banking industry, local banking markets do not appear to have become less competitive. Generally, in both rural and urban markets, the number of banks and offices has remained constant or increased somewhat, whereas the concentration measures have either remained constant or decreased somewhat. Modest deconcentration, in conjunction with a small increase in the number of banks, suggests that the availability of credit from commercial banking organizations probably has not declined in recent years.

Savings institutions, defined as savings banks and savings and loan associations, provide much less credit to small businesses than do commercial banks. The differences between the lending volumes of the two groups of institutions reflect both the disparity in overall size between the two groups and the lower proportion of small business lending conducted by the typical savings institution. Among savings institutions, the most active, or leading, lenders to small businesses were not necessarily the largest institutions in terms of assets. A comparison of the shares of small business lending by thrifts for 2002 with the corresponding data for 2006 indicates that the leading savings institutions in terms of small business activity have been accounting for an increasing share of outstanding business loans in both loan-size categories of interest--equal to or less than $1 million and equal to or less than $100,000--while the share of industry assets for these institutions has remained relatively constant. This finding suggests that although some thrifts have increasingly specialized in small business lending, they are not predominantly the largest institutions.

Credit scoring may lead to an increase in the availability of credit for small businesses, in part because it may increase the consistency, objectivity, and speed of credit evaluations while lowering the cost of gathering relevant information. In addition, it may have the potential to increase a lender's ability to accurately predict loan performance and may increase access to capital markets. Credit scoring has been used for more than thirty years in underwriting consumer loans but only since the early to mid-1990s in small business lending (Board of Governors, 2007).

Except for a few banks that have developed proprietary models, most organizations use scoring models obtained from outside vendors, the largest of which is Fair Isaac Corporation. The reliance by a large proportion of the industry on one vendor's model has raised concerns that the resulting problems could be widespread if the model performs poorly. It is not clear how small business credit-scoring models perform relative to traditional reviews of such loans, especially during a major economic slowdown. However, users of the models generally report that, after their adoption, (1) the riskiness of the small business portfolio either remains about the same or declines and (2) the quality of the typical credit decision increases.

Evidence regarding the effect of credit scoring on credit availability is consistent with proponents' claims that the use of scoring models increases the availability of credit to some small businesses. However, concerns have been raised that the continued adoption of credit-scoring techniques may reduce the availability of credit for small firms that find it hard to qualify for loans based only on a formal credit score. At this time, it is unclear how often creditworthy firms that would not qualify for credit-scored products would be able to obtain financing from a lender that relied on traditional methods of loan evaluation. Nonetheless, community banks and other local lenders are likely to continue to provide this valuable service to many small firms that would not qualify for credit-scored loans, especially if loans are priced appropriately.

The securitization of small business loans is a development that could substantially influence the availability of credit. Potential benefits exist for lenders, borrowers, and investors. However, the obstacles to securitizing loans to small businesses are large, especially with loans not backed by a guarantee from the Small Business Administration. Securitization has so far remained modest, and recent developments suggest that the volume of securitized small business loans is unlikely to increase substantially over the next several years.

Community reinvestment activities help financial institutions meet the financing needs of small businesses. Beyond conducting lending programs that are part of a bank's normal operating process, banks often develop or work with specially created entities focused on providing credit in underserved communities. Some of these entities operate wholly within a bank's legal structure, some are partnerships with other service providers, and still others are standalone organizations in which banks invest. These programs encourage capital to flow where it otherwise might not.

Numerous trends in the community development field either are just beginning to significantly influence the delivery of capital to small businesses by financial institutions or have the potential to do so in the near future. Some of these trends--for example, the proliferation of financial literacy and outreach programs--are due primarily to the actions of financial services firms themselves. Others are due to the actions of government--such as the New Markets Tax Credit--to stimulate more lending. Still other trends involve new hybrid partnerships among banks and nonbank entities such as local microloan funds. These trends, should they continue, are likely to result in improved access to credit and capital for small businesses.

Flows and Terms of Business Credit

Since 2002, the year of the previous report on the availability of credit to small businesses, business financing flows to both large and small firms have generally increased along with economic growth. Credit conditions have been favorable for small and large firms, and there is no evidence that creditworthy borrowers have faced substantial credit supply constraints.7

Aggregate Business Financing

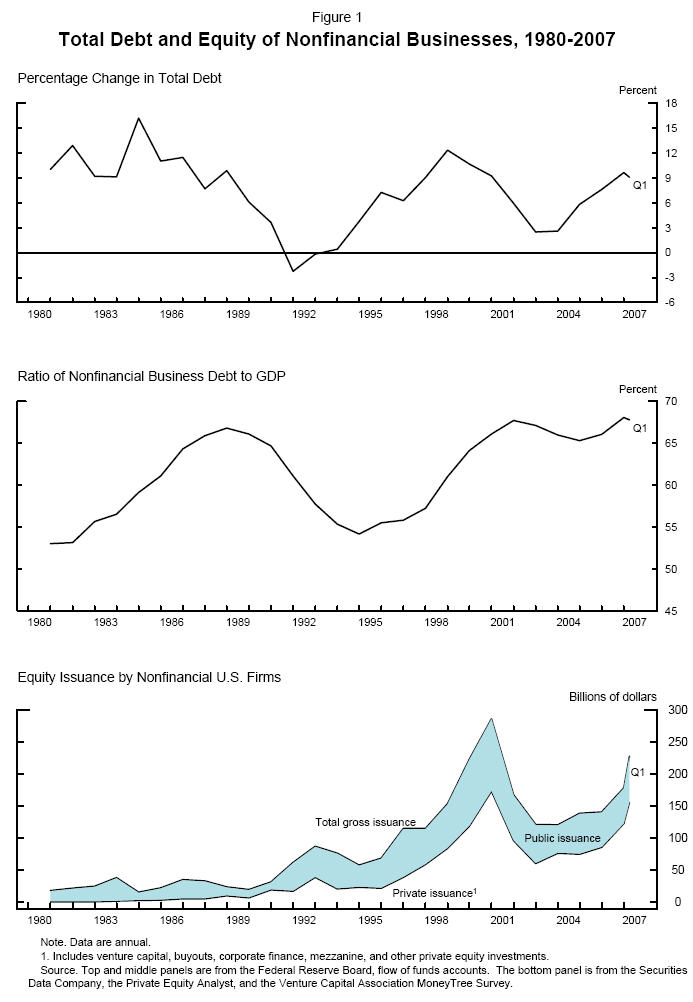

The recession of 2001 was marked by sharp reductions in the rate of real investment. Investment began to rebound in 2003 and has continued to rise since then, in part because of favorable credit conditions. Growth in total nonfinancial business debt, which mirrored these developments, surged from an annual rate of about 3 percent in 2002 and 2003 to a rate of 9 percent in the first quarter of 2007 (figure 1). As a result, the ratio of total nonfinancial business debt to gross domestic product (GDP) has increased to about 68 percent, the highest level in more than two decades.

Gross equity issuance by nonfinancial firms has also risen since 2002 (figure 1). Public equity issuance, through both initial and seasoned offerings, has maintained a steady but moderate pace by historical standards. In contrast, private issuance, boosted by the recent wave of leveraged-buyout transactions, has risen sharply from an annual rate of about $60 billion in 2002 to a pace of about $150 billion in the first quarter of 2007. Even so, net equity issuance, already negative in 2002, became even more negative over the period because of a surge in retirements of equity through cash-financed mergers (including leveraged buyouts) and share buybacks.

Financing by Nonfinancial Corporations

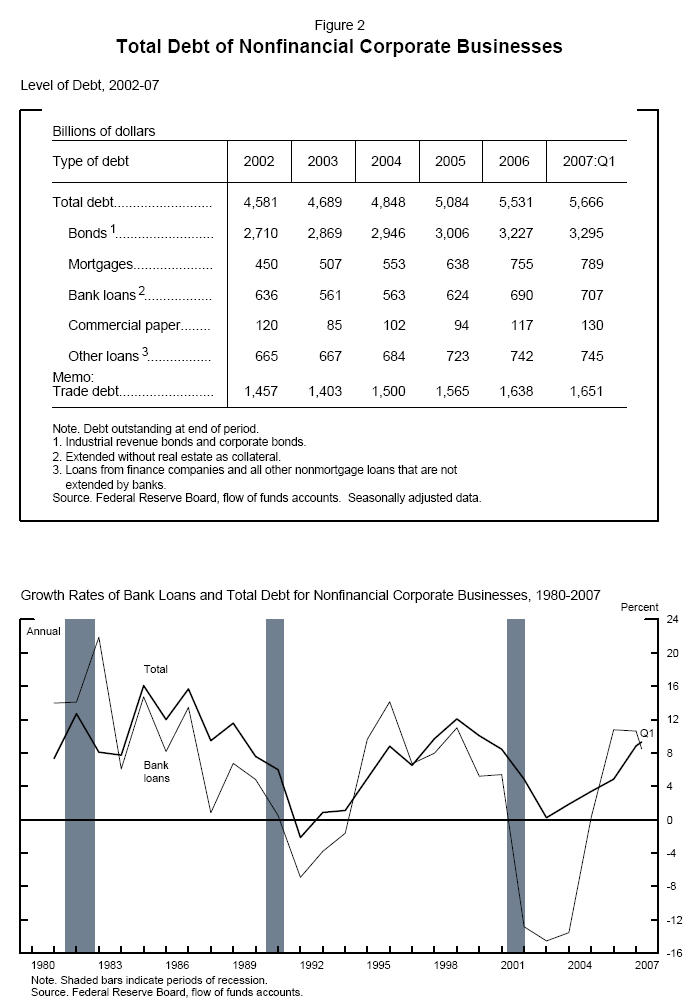

Growth in total nonfinancial corporate debt has risen steadily in the past five years (figure 2). It increased from an annual rate of a bit above zero in 2002 to a pace of about 9 percent in the first quarter of 2007. Corporate debt growth in 2003 and 2004 was weak; the small increase was due mainly to bond issuance, as decreases were recorded in bank loans extended without real estate as collateral and in commercial paper. Since then, nearly all components of corporate debt growth have expanded because of robust merger and acquisition activity and rising outlays for investment goods.

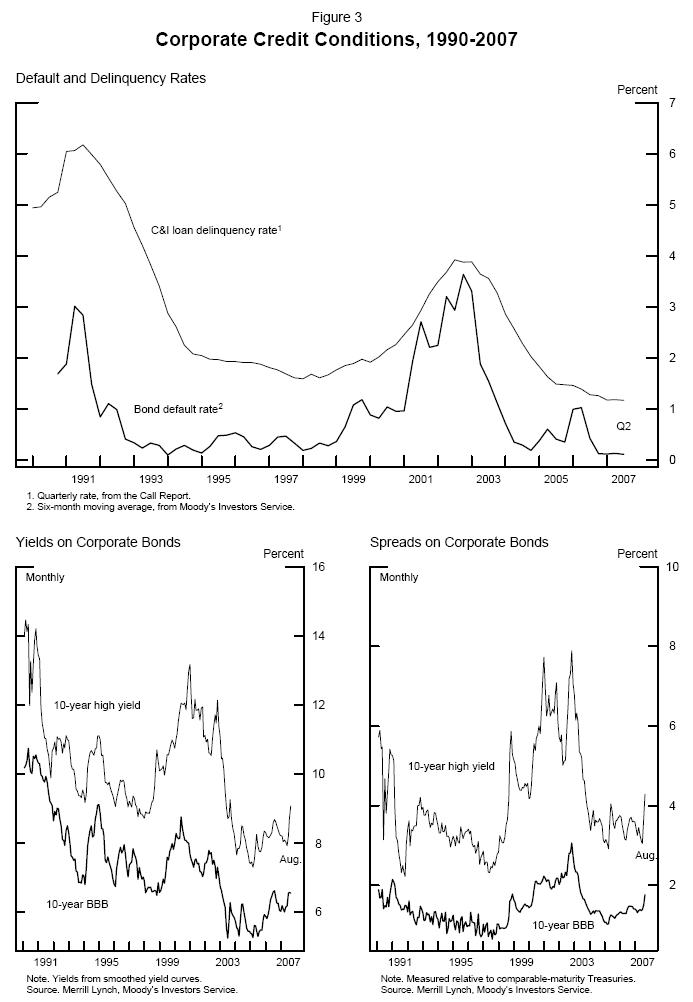

Improving financing conditions for firms in public capital markets and at banks may also have contributed to the increases in corporate debt growth since 2002. Default rates on corporate bonds and on commercial and industrial loans fell substantially to near-historic lows (figure 3). Yields on BBB-rated and high-yield corporate bonds also declined, and their spreads to yields on comparable-maturity Treasury securities remained at the low end of their historical ranges through the first half of 2007. Bond spreads have risen noticeably in recent months but are still far below their peaks in 2002. Relatively narrow yield spreads are consistent with strong overall corporate balance sheets.

Financing by Small Business

Comprehensive data that directly measure the financing activities of small businesses are nonexistent. However, various sources of information can serve as proxies for small business activity and can be used to identify patterns of small business financing. These sources suggest that financing flows to small firms weakened a bit in 2003 but have generally been robust since then.

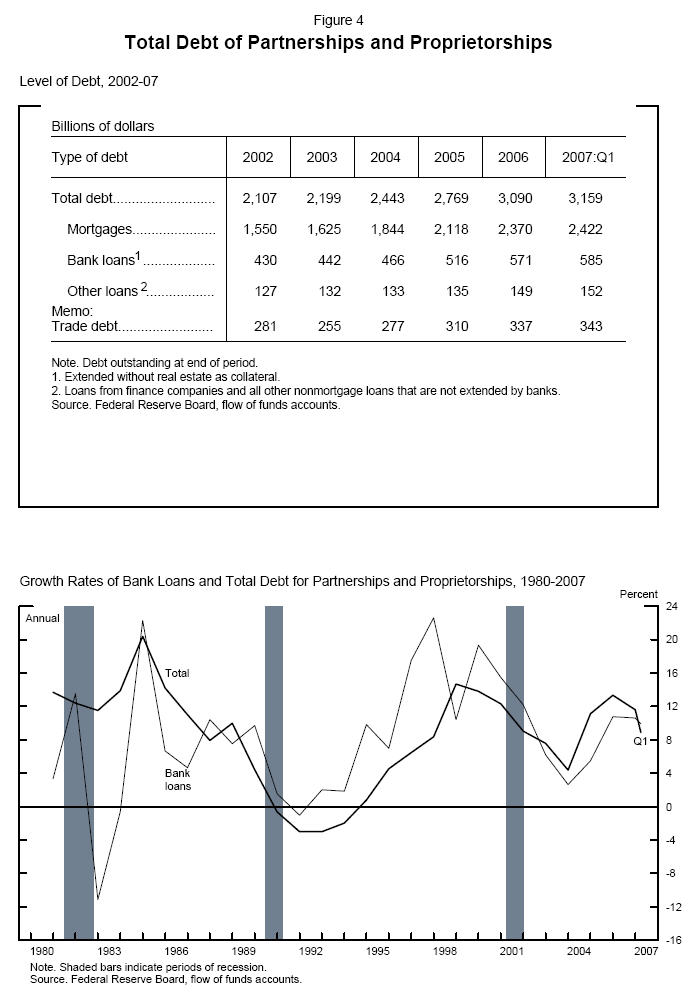

Total small business debt, estimated as the total debt of partnerships and proprietorships, reached $3.1 trillion in the first quarter of 2007 (figure 4).8 Growth in small business debt declined to about 4 percent in 2003, but it rose to about 12 percent in 2005 before moderating a touch over the next two years. Growth in two of the three components of total small business debt--mortgage debt and bank loans extended without real estate as collateral--followed a roughly similar pattern. Commercial bank loans (both with and without real estate as collateral) with principal less than or equal to $1 million, often extended to small firms, have shown modest but steady growth since 2003 (table 1).

| Size of loan and year | All | Commercial and industrial | Nonfarm nonresidential real estate | |

|---|---|---|---|---|

| Amount outstanding, June 30 (billions of dollars) | ||||

| Small business loans ($1 million or less) | ||||

| 2002 | 471.6 | 239.0 | 232.6 | |

| 2003 | 482.5 | 234.7 | 247.8 | |

| 2004 | 504.2 | 239.4 | 264.8 | |

| 2005 | 523.6 | 244.1 | 279.6 | |

| 2006 | 549.8 | 250.8 | 299.0 | |

| Change1 (percent) | ||||

| 2003 | 2.3 | -1.8 | 6.5 | |

| 2004 | 4.5 | 2.0 | 6.9 | |

| 2005 | 3.8 | 2.0 | 5.6 | |

| 2006 | 5.0 | 2.7 | 6.9 | |

| Amount outstanding, June 30 (billions of dollars) | ||||

| Microloans ($100,000 or less) | ||||

| 2002 | 120.0 | 89.2 | 30.9 | |

| 2003 | 115.9 | 86.5 | 29.4 | |

| 2004 | 113.1 | 85.2 | 27.9 | |

| 2005 | 112.7 | 85.2 | 27.5 | |

| 2006 | 115.2 | 89.2 | 26.0 | |

| Change1 (percent) | ||||

| 2003 | -3.4 | -3.0 | -4.9 | |

| 2004 | -2.4 | -1.5 | -5.1 | |

| 2005 | -.4 | .0 | -1.4 | |

| 2006 | 2.2 | 4.7 | -5.5 | |

Note. Small business loans are business loans of $1 million or less; microloans, a subset of small business loans, are for $100,000 or less. U.S. commercial banking organizations are insured U.S. domestically chartered banks excluding credit card institutions and U.S. branches and agencies of foreign banks. Details may not sum to totals because of rounding.

1. Change is from June of preceding year to June of year indicated. Return to table

Source. Call Reports (June 30), various years.

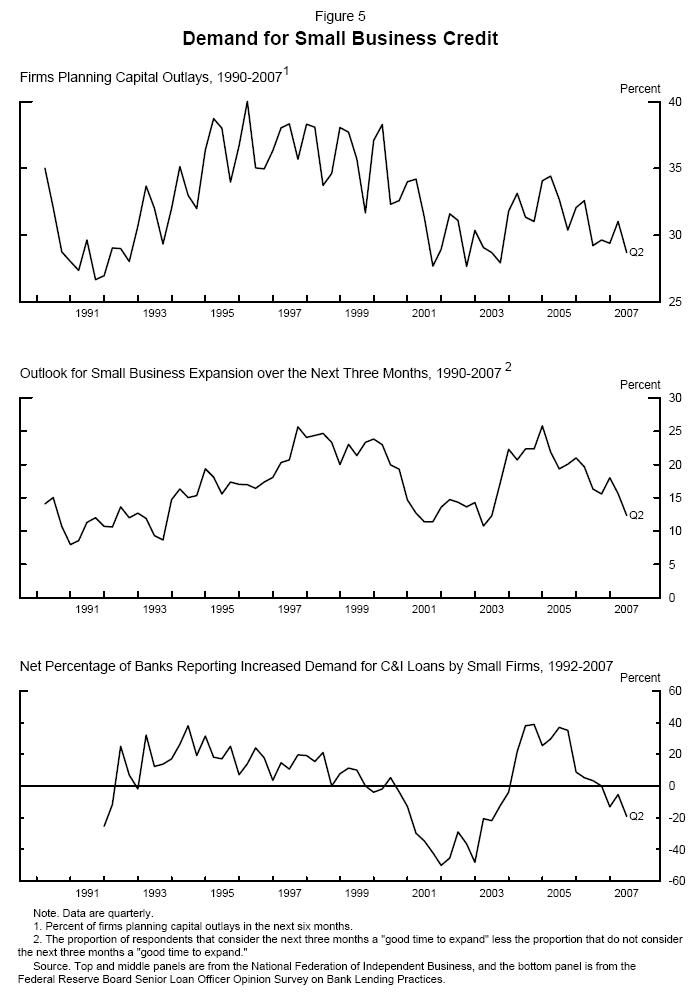

Indicators of small business financing needs suggest that demand picked up in 2004 from low levels but moderated in 2006 and 2007. The demand for small business financing can be inferred from small business investment plans, as reported in surveys conducted by the National Federation of Independent Business (NFIB).9 According to the surveys, the net percentage of firms that planned capital outlays and the net percentage that anticipated business expansions were low by historical standards in 2002 and 2003, rose to above-average levels in 2004 and 2005, but then reverted to low levels in 2006 and 2007 (figure 5). Data on demand for commercial and industrial loans, as reported in the Federal Reserve's Senior Loan Officer Opinion Survey on Bank Lending Practices, show a similar up-and-down pattern over the period.

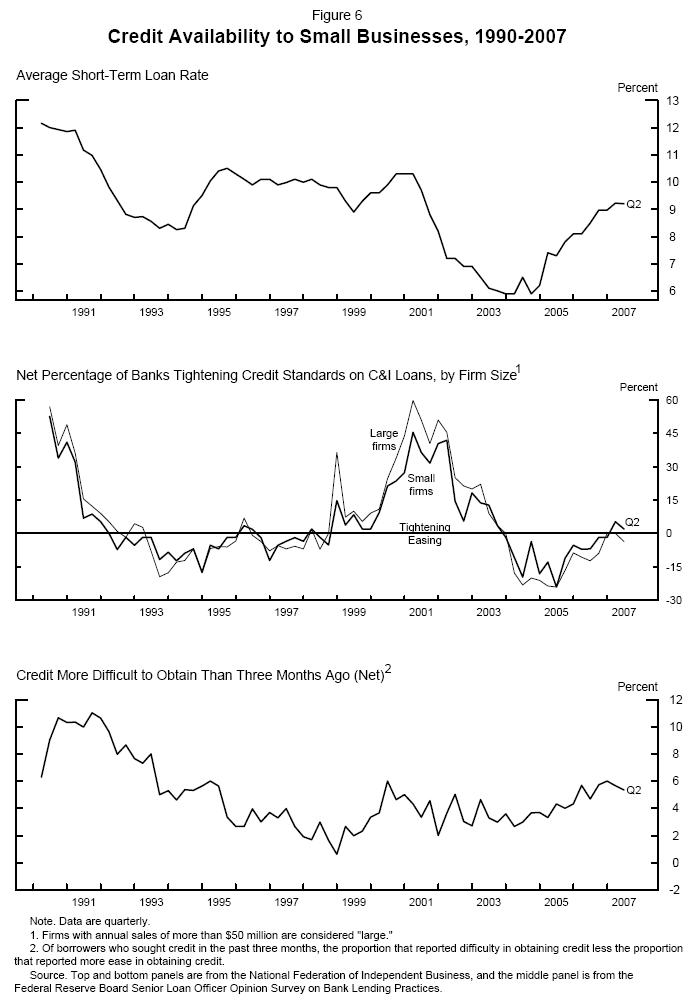

Credit conditions at banks for small businesses have been favorable, for the most part, since 2002. Results from the Senior Loan Officer Opinion Survey indicate that lending standards for small borrowers were tightened a bit in 2002 and 2003, were loosened substantially in each of the subsequent three years, and were about unchanged in the first part of 2007 (figure 6). Responses to other questions in the survey suggest that the general easing of standards since 2004 is due mainly to the favorable economic outlook and the increased competition among banks and other nonbank lenders. Since 2002, the net percentage of NFIB respondents reporting that credit had become more difficult to obtain remained low through the first half of 2007 by historical standards, even as the average short-term interest rate paid by NFIB respondents increased from a low of 6 percent in 2004 to about 9 percent in the first half of 2007.10

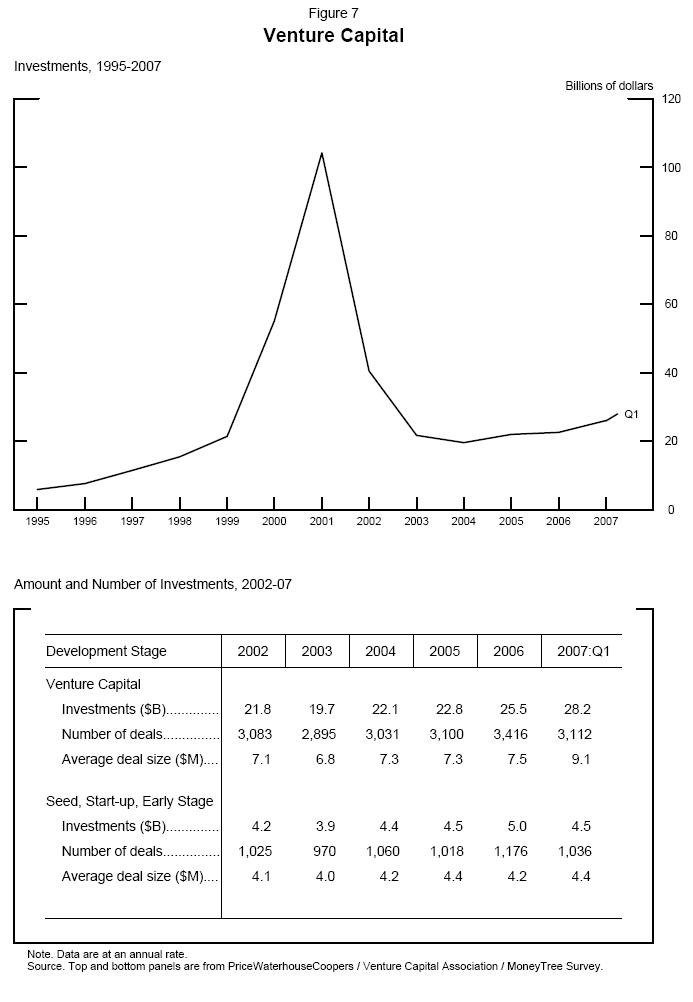

Although well below its record pace of the late 1990s, financing to small business with the potential for significant growth has been solid since 2002. Venture capital investments edged down a bit from $22 billion in 2002 to $20 billion in 2003, have steadily increased since then, and are on pace to reach $28 billion in 2007 (figure 7). Financing of firms at very early stages of development followed a similar pattern.

Credit Use by Small Businesses

This section examines the composition and borrowing behavior of small firms to identify characteristics that are associated with important patterns of credit use. It also discusses the special role that small business plays in the U.S. economy and the unique challenges they face in obtaining credit.

Small Business: Definition and Background

Defining what is meant by "small business" is the first step in conducting a policy-relevant analysis of the financing needs of small business; it is also difficult. The financing needs are very different for a "mom and pop" grocery store, a microenterprise in the inner city, a start-up high-tech firm, a business that is ready to expand from early-stage growth to the next higher level, or a business that has neared the point of issuing public debt or equity. Yet the term "small business" encompasses all of these. According to a broad guideline used by the U.S. Small Business Administration (SBA), a small business is a firm or enterprise with fewer than 500 employees. This definition encompasses more than 99 percent of all businesses in the United States.

The vast majority of small businesses are modest in size. The 2003 Survey of Small Business Finances (SSBF), which is representative of more than 6.3 million nonfarm, nonfinancial businesses with fewer than 500 workers, estimates that more than 91 percent of these businesses have fewer than twenty employees (including working owners) and that three-fifths have fewer than five (table A.1).

Just more than half of the small businesses were organized as proprietorships (44.5 percent) or partnerships (8.7 percent) in 2003. The remainder were organized as either S corporations (31 percent) or C corporations (15.7 percent). The primary difference between the two types of corporations is that C corporations are subject to corporate income tax. However, S corporations are legally constrained to have no more than seventy-five shareholders, are restricted to one class of stock, and to avoid income tax liability, must pass all income to the owners at the end of each fiscal year. In recent years, the S corporation organizational form has become more popular. Between 1998 and 2003, the share of firms organized as S corporations increased from 24 percent to 31 percent, while the share organized as C corporations and that organized as proprietorships declined, respectively, from 20 percent to 15.7 percent and from 49 percent to 44.5 percent.

Two other organizational forms gained legal status in several states during the latter 1990s: the limited liability corporation (LLC) and the limited liability partnership (LLP). LLCs share many characteristics of partnerships but also have the limited liability of a corporation. LLPs are partnerships in which an investor's liability is limited to his or her initial investment. In this report, LLCs and LLPs are classified as partnerships, corporations, or proprietorships according to the way they file their taxes. LLCs may file taxes as partnerships, sole proprietorships, or corporations, and LLPs may file as either partnerships or corporations.

Small businesses operate in every major segment of the U.S. economy. The most common industry for small businesses in 2003 was business services, which accounted for one-fourth of small firms (table A.1). Another fourth of small businesses were in the retail (18.4 percent) and wholesale (5.9 percent) trade sectors. The remaining half of small businesses were involved in professional services (20.6 percent), construction and mining (11.8 percent), insurance and real estate (7.2 percent), transportation (3.8 percent), and manufacturing (7.1 percent).

In 2003, 94 percent of the small businesses in the United States had owners who actively participated in the firm's management, 85.9 percent had a single office, and 79.4 percent were located in urban areas. Geographically, small businesses were widely dispersed throughout the nation, with 19.8 percent in the Northeast, 21.1 percent in the Midwest, 24.4 percent in the West, and the remaining 34.7 percent in the South. A demographic breakdown of the universe of nonfarm, nonfinancial small businesses in the United States according to the 2003 SSBF appears in table A.1.

Small businesses contribute significantly to the strength and vigor of the U.S. economy. According to the SBA, firms with fewer than 500 employees employ more than one-half of private-sector workers and produce more than one-half of the private-sector output. They account for 99.9 percent of all firms. Large and successful companies often begin as smaller firms that prosper and grow. In 2005, the latest year for which data are available, the estimated number of employer firm births, at 671,800, was higher than the number of deaths, at 544,800, for a net change of 127,000 new employer businesses (a net annual growth rate of 2.2 percent). Firms with fewer than 500 employees accounted for 99.9 percent of all firm births and deaths (U.S. Small Business Administration, 2006, p. 10).

The concerns of the Congress and other policymaking bodies about small business financing stem from the perception that small firms have more difficulty gaining access to credit sources than do large businesses or other types of borrowers. The source of this difficulty may be the greater riskiness of small firms and the associated high costs of evaluating and monitoring credit risks, or it may be inefficiencies in markets that hinder pricing of risk or impede the effective pooling of risks. To the extent that private-market impediments or inefficiencies are the source of any difficulties for small business financing, policymakers may focus on changes that reduce these constraints. In this case, no one policy prescription would likely work for all, and no one definition of small business would be appropriate. As discussed in this report, credit needs and borrowing sources differ widely among small businesses.

Risks of Lending to Small Businesses

Lending to small businesses is generally considered riskier and more costly than lending to larger firms. Small businesses tend to be much more affected by swings in the economy and have a much higher failure rate than larger operations.11 In addition, lenders historically have had difficulty determining the creditworthiness of applicants for some small business loans. The heterogeneity across small firms, together with widely varying uses of borrowed funds, has impeded the development of general standards for assessing applications for small business loans and has made evaluating such loans relatively expensive.

Lending to small businesses is further complicated by the "informational opacity" of many such firms. Obtaining reliable information on the creditworthiness of a small business is often difficult because little, if any, public information exists about the performance of most small businesses. Small businesses rarely have publicly traded equity or debt securities, and public information on such firms is typically sparse. Many small businesses also lack detailed balance sheets and other financial information often used by lenders in making underwriting decisions.

The cost to the lender does not end with the decision to grant a loan. Small business lenders typically have had to monitor the credit arrangement with individual borrowers. For very small firms, a close association between the finances of the business and those of the owner may increase loan-monitoring costs.

Historically, the relatively elevated costs of evaluating small business applications and the ongoing costs of monitoring firm performance have made loans to small businesses less attractive for some lenders, especially because, when expressed as a percentage of the (small) dollar amount of the proposed loan, these non-interest costs are often quite high relative to loans to middle-market or large corporate borrowers. Financial institutions, especially commercial banks, are believed to have an advantage in dealing with information problems. Through interactions with a firm that uses its financial services, the lending institution can obtain additional information about the firm's activities, ownership, financial characteristics, and prospects that is important in deciding whether to extend credit.12 Lenders can use information gathered over time through long-term relationships with business owners and other members of the local community to monitor the health of the business and to build appropriate incentives into loan agreements.13 The role of relationship lending will likely continue to be significant, even as developments such as automated banking, credit scoring, and bank consolidation influence the competitive structure of the banking industry.14

Credit Use

Up-to-date and comprehensive information about the universe of small businesses is sparse, and most evidence about financing needs and sources is derived largely from surveys. Researchers have learned a great deal about the financing of small businesses from various data sources and studies, particularly from the SSBF. This survey, which was conducted most recently for year-end 2003, provides the most comprehensive and up-to-date information available on small business use of financial services and providers.15

The 2003 SSBF gathered data from interviews with 4,240 small businesses between June 2004 and January 2005. The firms were selected to be representative of for-profit, nonfarm, nonfinancial small businesses operating in the United States in December 2003. The survey gathered details on the characteristics of each business and its top three owners, the firm's income statement and balance sheet, and the use and sources of financial services. It also obtained information about the firm's recent experiences in borrowing and applying for credit, the use of trade credit, and capital infusions. The previous survey had been conducted for fiscal year 1998 using a sample of 3,561 firms.

Data from the 2003 SSBF describe patterns of credit use by small businesses. Although this information is influenced by both demand and supply factors, it is nonetheless very useful in developing a picture of the demand for credit by small businesses. The data reveal patterns at both the aggregate and the firm levels.16

Although recent economic developments may have altered small business behavior from that reported in the 2003 SSBF, past surveys suggest that the 2003 results should still provide a good picture of current small business behavior because patterns in the use of credit by small businesses change slowly. When significant differences exist between the 1998 and the 2003 data, these differences are discussed to highlight potentially important trends in the use of credit by small businesses.

Types of Traditional Credit Used

Most small businesses use traditional types of credit, including loans taken down under lines of credit, mortgages used for business purposes, equipment loans, motor vehicle loans, capital leases, and "other loans." In 2003, 60.4 percent of small businesses used one of these traditional forms of credit (table A.2). This incidence is slightly higher than the 55 percent that reported using traditional forms of credit in 1998.

Among all small businesses in 2003, several patterns in credit use are apparent from the figures in table A.2. Larger firms were more likely than smaller firms to use at least one of the traditional forms of credit. A large majority (94 percent) of firms with between 100 and 499 employees used credit, whereas about two-fifths of firms with fewer than two employees did. Among firms that used a traditional credit product, use increased with firm size. The median credit-using firm with between 100 and 499 employees had four credit lines, loans, or leases with a total outstanding balance of more than $870,000 (table 2). These figures are substantially higher than those for the median credit-using firm with fewer than two employees, which had one credit line, loan, or lease with a combined balance of $17,000.

| Category of firm | Any | Credit line | Mortgage loan | Vehicle loan | Equipment loan | Capital lease | Other credit | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Number | Balance | Number | Balance | Number | Balance | Number | Balance | Number | Balance | Number | Balance | Number | Balance | |

| All firms | 2 | 38,983 | 1 | 15,030 | 1 | 108,487 | 1 | 20,000 | 1 | 20,663 | 1 | 8,080 | 1 | 40,400 |

| Number of employees1 | ||||||||||||||

| 0-1 | 1 | 17,000 | 1 | 5,000 | 1 | 83,000 | 1 | 17,500 | 1 | 15,600 | 1 | 3,600 | 1 | 17,000 |

| 2-4 | 1 | 24,000 | 1 | 12,000 | 1 | 79,200 | 1 | 16,000 | 1 | 6,200 | 1 | 5,560 | 1 | 18,712 |

| 5-9 | 2 | 41,600 | 1 | 19,840 | 1 | 96,000 | 1 | 20,000 | 1 | 21,000 | 1 | 6,800 | 1 | 38,800 |

| 10-19 | 3 | 102,300 | 1 | 33,000 | 1 | 215,000 | 2 | 28,000 | 1 | 36,000 | 1 | 14,800 | 1 | 100,000 |

| 20-49 | 3 | 190,900 | 1 | 36,560 | 1 | 283,200 | 2 | 33,960 | 1 | 62,000 | 1 | 20,000 | 1 | 140,800 |

| 50-99 | 3 | 464,728 | 1 | 90,200 | 1 | 600,000 | 3 | 51,200 | 1 | 156,728 | 2 | 65,000 | 1 | 310,000 |

| 100-499 | 4 | 873,000 | 1 | 130,000 | 2 | 937,643 | 2 | 78,896 | 2 | 506,546 | 2 | 69,000 | 2 | 900,000 |

| Standard Industrial Classification | ||||||||||||||

| Construction and mining (10-19) | 2 | 40,000 | 1 | 10,400 | 1 | 78,000 | 1 | 25,000 | 2 | 43,000 | 1 | 20,000 | 1 | 39,000 |

| Manufacturing (20-39) | 2 | 60,000 | 1 | 20,000 | 1 | 181,000 | 1 | 20,000 | 1 | 39,000 | 1 | 15,000 | 1 | 80,000 |

| Transportation (40-49) | 2 | 70,000 | 1 | 18,120 | 1 | 65,000 | 2 | 30,000 | 1 | 69,000 | 2 | 38,000 | 1 | 42,000 |

| Wholesale trade (50-51) | 2 | 70,000 | 1 | 26,000 | 1 | 105,000 | 1 | 20,441 | 1 | 16,000 | 2 | 14,839 | 1 | 84,000 |

| Retail trade (52-59) | 2 | 50,000 | 1 | 20,073 | 1 | 133,600 | 1 | 20,000 | 1 | 12,331 | 1 | 5,940 | 1 | 50,000 |

| Insurance and real estate (60-69) | 2 | 75,120 | 1 | 20,000 | 1 | 164,838 | 1 | 15,200 | 1 | 15,000 | 1 | 5,000 | 1 | 91,146 |

| Business services (70-79) | 2 | 27,759 | 1 | 10,600 | 1 | 100,000 | 1 | 17,188 | 1 | 16,582 | 1 | 10,374 | 1 | 20,078 |

| Professional services (80-89) | 2 | 28,680 | 1 | 15,793 | 1 | 121,529 | 1 | 18,000 | 1 | 12,228 | 1 | 6,000 | 1 | 30,000 |

Note. Data are weighted to adjust for differences in sampling and response rates and reflect population rather than sample measures.

1. Number of owners working in the business plus number of full- and part-time workers. Return to table

Source. 2003 Survey of Small Business Finances.

Although these data reveal a strong association between firm size and the extent of borrowing, they cannot measure how much of the association may be due to relatively greater capital needs of larger firms and how much may be due to the greater difficulty that smaller firms have in obtaining credit. The relative demand for credit likely increases with firm size because credit needs tend to expand with the scope of operations and inventories that a firm needs to hold. Size also tends to be associated with various characteristics of the firm that could affect its ability to gain access to credit from external sources. For example, larger firms tend to have more assets for collateral, are likely to be more diversified, and frequently have longer performance histories.

The share of small firms in each industry that used credit was highest for firms in transportation (79.1 percent), construction and mining (70.7 percent), and manufacturing (70 percent). It was noticeably lower in the service sectors (56.4 percent in business services and 54.1 percent in professional services), which rely less on inventories or machinery (table A.2).

Different patterns of credit use among various firms exist not just for all credit lines, loans, and leases but for the individual products in this group as well. Patterns for each product are discussed below. Much of the data illustrating differences come from the 2003 SSBF and are presented in the appendix. Specifically, table A.2 reports the percentage of each firm type that used each of the traditional credit products, and table A.8 reports the share of total outstanding balances in each of the traditional credit products by firm type.17 In addition, table 2 shows the median balances outstanding for each credit product. Figures from each of these three tables are cited in the discussion of specific credit products.

Credit Lines

As was true in 1998, credit lines were the most common traditional form of credit used by small businesses in 2003. Between 1998 and 2003, use of credit lines increased. In 1998, 28 percent of firms reported using credit lines; in 2003, more than one-third of all firms reported doing so. Credit lines accounted for 31.7 percent of the total dollar value of traditional credit outstanding. Among firms with lines of credit, the median firm had one line of credit with a credit limit of $50,000 and a balance of $15,030.

Substantial variation exists in the use of credit lines across industries. Credit lines were most important to firms involved in wholesale trade. In this industry, 49.4 percent of small firms used credit lines, which accounted for 55.3 percent of the value of all traditional credit outstanding at these firms. Firms in the manufacturing industry and the construction and mining industry were also frequent users of lines of credit. Figures for the share of firms that used lines of credit and their share of traditional credit outstanding were 47.8 percent and 44.2 percent in manufacturing, and 44.6 percent and 27.3 percent in construction and mining. Heavy use by firms in these industries may be explained by the need to maintain large inventories, which is expensive and generally requires financing. In contrast, among professional services firms, for which inventory may not be as important, only 29.4 percent of firms used lines of credit, a share that accounted for 21 percent of all outstanding traditional credit.

The use of credit lines was less common among younger firms than among older firms. Among firms with fewer than five years under current ownership, 30.2 percent used credit lines, compared with 39.3 percent of firms with twenty-five or more years under current ownership. At the same time, however, the share of traditional credit accounted for by firms with open lines did not vary much with firm age. Credit lines accounted for about 30 percent of outstanding credit at both the youngest firms (those in operation fewer than five years) and the oldest firms (those in operation twenty-five years or more). Comparing firms with credit lines, the credit limit of the average firm with fewer than five years under current ownership was less than half the credit limit of older firms. The balances on the credit lines of these younger firms were also noticeably lower than those at the older firms, though the difference was not as large as the difference between the credit limits.

Credit-line use increased with firm size: Smaller small firms used this type of credit less frequently than larger small firms. This difference may reflect the lower credit needs of smaller firms, a reduced ability of young and small firms to obtain credit due to the greater information opacity, or the higher risks and costs associated with lending to such firms.

The SSBF data on credit lines provide additional insight into the demand and availability of small business credit. Table 3 shows the ratio of credit-line balance to credit limit for each firm type--that is, the percentage of available credit that each firm used in 1998 and 2003. These percentages increased somewhat for most categories of small businesses between 1998 and 2003, perhaps because of an increased demand for credit in 2003. However, in 2003, most types of small businesses reported using less than half of their available credit lines. Thus, while credit lines were used somewhat more intensively in 1998 than in 2003, most firms with credit lines apparently had additional credit available from unused lines.

| Category of firm | 1998 | 2003 |

|---|---|---|

| All firms | 38.6 | 45.5 |

| Number of employees1 | ||

| 0-1 | 37.1 | 48.7 |

| 2-4 | 41.1 | 40.7 |

| 5-9 | 50.5 | 50.8 |

| 10-19 | 34.3 | 38.3 |

| 20-49 | 29.9 | 41.4 |

| 50-99 | 43.4 | 46.0 |

| 100-499 | 39.6 | 48.4 |

| Standard Industrial Classification | ||

| Construction and mining (10-19) | 29.7 | 33.2 |

| Manufacturing (20-39) | 40.1 | 45.2 |

| Transportation (40-49) | 39.7 | 47.0 |

| Wholesale trade (50-51) | 29.2 | 47.2 |

| Retail trade (52-59) | 58.2 | 56.0 |

| Insurance and real estate (60-69) | 38.9 | 39.9 |

| Business services (70-79) | 47.6 | 50.0 |

| Professional services (80-89) | 27.9 | 31.0 |

| Years under current ownership | ||

| 0-4 | 46.8 | 53.6 |

| 5-9 | 47.5 | 46.5 |

| 10-14 | 39.2 | 50.1 |

| 15-19 | 32.1 | 44.7 |

| 20-24 | 30.3 | 43.3 |

| 25 or more | 39.9 | 39.9 |

| Organizational form | ||

| Proprietorship | 33.7 | 40.5 |

| Partnership | 39.1 | 38.0 |

| S corporation | 41.9 | 46.1 |

| C corporation | 35.9 | 47.7 |

Note. Data are weighted to adjust for differences in sampling and response rates and reflect population rather than sample measures.

1. Number of owners working in the business plus number of full- and part-time workers. Return to table

Source. 2003 Survey of Small Business Finances.

Motor Vehicle Loans

Motor vehicle loans continue to be the second most commonly used type of traditional credit. In 1998, 20 percent of firms reported one or more motor vehicle loans. By 2003, more than one-fourth of all firms had reported outstanding motor vehicle loans. These loans, however, accounted for only 5.1 percent of the total amount of traditional credit outstanding because motor vehicle loans are small compared with the other types of credit. Of firms with motor vehicle loans, the median firm had one such loan with a balance of $20,000.

Motor vehicle loans were most frequently used in the construction and mining industry (43.9 percent) and in the transportation industry (42.9 percent), where these loans accounted for 14.4 and 11.5 percent of outstanding balances respectively. The median firm in the transportation industry that used this type of loan had two motor vehicle loans outstanding with a combined balance of $30,000, which was more than 50 percent larger than the median amount in any industry other than construction and mining.

Mortgage Loans

Approximately 13.3 percent of all firms had mortgage loans for business purposes, making this the third most commonly used type of credit. In terms of dollar amount, mortgage loans were the largest form of credit, accounting for 39 percent of traditional credit outstanding. These figures do not represent a significant change from the results of the 1998 survey, which showed that mortgages were used by 13.2 percent of small businesses and accounted for 35 percent of outstanding credit. Among the 13 percent of firms with mortgages, the median firm had one mortgage with a balance of $108,000.

The proportion of firms with mortgage loans used for business purposes increased with firm size. Only 5.6 percent of firms with fewer than two employees reported outstanding mortgages, whereas more than one-fourth of firms with 100 to 499 employees did so. In contrast, the proportion of traditional credit accounted for by mortgages fell with firm size. By organizational form, partnerships were the most likely to have outstanding mortgages, which accounted for nearly 68.3 percent of all outstanding credit.

Mortgage loans were the most important form of finance in the insurance and real estate industry. Mortgages were used by almost one-fourth of the small firms in the industry, and they accounted for 70.1 percent of the outstanding credit balances. Among firms in the industry that used mortgages, the median outstanding mortgage balance was $165,000, which was about $60,000 more than the median outstanding mortgage for all firms.

Capital Leases

Capital leases, which are leases on equipment that are often provided by the manufacturer of the equipment or a subsidiary, were used somewhat less frequently in 2003 than in 1998. Between 1998 and 2003, the share of small businesses that used leases fell from 10.3 percent to 8.7 percent. The lease share of total outstanding traditional credit also fell from 5.8 percent in 1998 to 3.2 percent in 2003. Among firms that used capital leases in 2003, the median firm had one capital lease with an outstanding balance of roughly $8,000.

Capital leases, which include automobile and equipment leases, were most heavily used in transportation industries. These leases were used by 9.3 percent of firms in transportation, a share that accounted for more than 20 percent of total outstanding credit. The median transportation firm had two leases, and the median outstanding balance of $69,000 was almost twice that for any other industry. Even though leases were somewhat more common for firms in the manufacturing (10.9 percent) and professional services (13.5 percent) industries, their share of traditional credit outstanding was only a modest 2.6 percent in manufacturing and 3.2 percent in professional services. Of the firms in these industries with a lease, the median firm had a single lease.

Equipment Loans and Other Types of Credit

Equipment loans were used by 10.3 percent of all firms and accounted for 7.2 percent of outstanding credit. Among firms that had at least one equipment loan, the median firm had one such loan with a balance of $21,000.

Not surprisingly, equipment loans were most significant in industries that rely heavily on equipment: construction and mining (12.6 percent of balances), manufacturing (15.2 percent), and transportation (18.4 percent). They were also somewhat important in wholesale trade, in which they accounted for 11.3 percent of outstanding loan balances, but in all other major industries, equipment loans accounted for less than 10 percent of outstanding balances.

Finally, unspecified other types of credit were used by 10.1 percent of small businesses and accounted for 13.7 percent of outstanding credit. The median firm with at least one "other" loan had one such loan outstanding with a balance of $40,000. Most of these loans were unsecured term loans. Approximately equal proportions of these loans were made by financial intermediaries or by family and friends.

Alternatives to Traditional Credit

Small business owners may turn to alternative forms of credit if they find themselves unable to obtain traditional forms or if they find the terms of these other products more favorable. Three such alternatives--credit cards, trade credit, and owner loans--can be examined using data from the 1998 and 2003 SSBFs. Widely used, these alternative forms of credit may be important both in financing small businesses and, as substitute products, in influencing the demand for traditional credit by small firms. According to the 2003 SSBF, 60.4 percent of small firms used a credit line, loan, or lease, but almost 89 percent used an alternative form of credit. Nearly 93 percent of small firms used either a traditional type of credit, a credit card, trade credit, or an owner loan.

Credit Cards

Credit cards can serve as a convenient alternative to paying expenses by cash or check if a business pays balances on time and in full each month. They can also substitute for traditional forms of credit when balances are carried month to month. Survey evidence suggests that credit cards are used primarily for convenience and that, despite a large increase in the use of credit cards between 1998 and 2003, small businesses have not substantially increased their use of credit cards as an alternative to traditional forms of credit.

Credit cards used for business purposes can be issued to the firm itself or to the owners of the firm, who may also use their personal credit cards for business expenses. Table 4 shows the percentage of small businesses that used personal credit cards, business credit cards, or either personal or business credit cards to pay for business expenses in 1998 and 2003. The use of credit cards by small businesses increased substantially between 1998 and 2003. In 2003, more than 77 percent of small businesses used either a business or a personal credit card to pay for business expenses--an increase of 9 percentage points over the 1998 percentage of firms using credit cards.

| Category of firm | 1998 | 2003 | ||||||

|---|---|---|---|---|---|---|---|---|

| Any1 | Personal | Business | Paid balance2 | Any1 | Personal | Business | Paid balance2 | |

| All firms | 68.0 | 46.0 | 34.1 | 76.3 | 77.3 | 46.7 | 48.1 | 70.7 |

| Number of employees3 | ||||||||

| 0-1 | 59.0 | 45.6 | 20.0 | 75.2 | 69.5 | 48.6 | 32.0 | 69.6 |

| 2-4 | 65.3 | 47.1 | 28.8 | 72.5 | 76.4 | 48.1 | 45.7 | 65.9 |

| 5-9 | 73.4 | 45.4 | 43.2 | 76.5 | 81.0 | 47.8 | 56.8 | 68.5 |

| 10-19 | 80.0 | 51.5 | 50.8 | 78.5 | 85.0 | 45.6 | 59.7 | 79.4 |

| 20-49 | 81.9 | 41.7 | 56.9 | 88.5 | 81.5 | 34.4 | 61.7 | 85.2 |

| 50-99 | 75.2 | 31.3 | 58.6 | 94.1 | 81.9 | 34.6 | 63.5 | 93.9 |

| 100-499 | 76.8 | 23.7 | 62.5 | 97.5 | 82.9 | 32.2 | 71.4 | 92.4 |

| Standard Industrial Classification | ||||||||

| Construction and mining (10-19) | 65.3 | 40.8 | 33.4 | 80.5 | 76.9 | 44.7 | 52.1 | 75.1 |

| Manufacturing (20-39) | 73.8 | 48.7 | 39.3 | 73.2 | 81.7 | 47.1 | 54.8 | 71.6 |

| Transportation (40-49) | 72.2 | 44.1 | 45.5 | 79.9 | 74.6 | 41.4 | 51.8 | 70.8 |

| Wholesale trade (50-51) | 75.1 | 45.8 | 46.3 | 80.8 | 81.3 | 46.7 | 54.4 | 76.2 |

| Retail trade (52-59) | 59.4 | 41.0 | 29.9 | 70.6 | 75.1 | 47.9 | 45.0 | 64.8 |

| Insurance and real estate (60-69) | 68.7 | 41.5 | 36.3 | 88.3 | 72.6 | 47.4 | 43.0 | 85.2 |

| Business services (70-79) | 64.4 | 47.0 | 28.3 | 70.2 | 76.3 | 45.2 | 47.0 | 66.4 |

| Professional services (80-89) | 76.8 | 53.9 | 36.2 | 80.5 | 80.0 | 48.8 | 47.1 | 71.7 |

| Years under current ownership | ||||||||

| 0-4 | 66.4 | 46.0 | 28.7 | 68.9 | 73.7 | 45.2 | 46.6 | 67.5 |

| 5-9 | 72.5 | 48.7 | 38.2 | 74.0 | 77.3 | 44.6 | 49.7 | 63.4 |

| 10-14 | 68.2 | 46.6 | 34.3 | 79.1 | 80.9 | 49.8 | 48.7 | 72.2 |

| 15-19 | 67.7 | 43.7 | 37.5 | 78.7 | 79.5 | 48.5 | 52.3 | 71.9 |

| 20-24 | 66.5 | 46.2 | 34.2 | 84.1 | 79.6 | 46.9 | 50.7 | 74.9 |

| 25 or more | 64.6 | 42.8 | 32.5 | 80.9 | 75.2 | 46.6 | 43.1 | 78.6 |

| Organizational form | ||||||||

| Proprietorship | 62.3 | 49.6 | 21.9 | 71.7 | 73.0 | 52.3 | 35.1 | 66.6 |

| Partnership | 59.6 | 37.0 | 30.4 | 71.9 | 73.0 | 41.7 | 46.9 | 70.9 |

| S corporation | 77.4 | 44.2 | 47.3 | 80.0 | 83.4 | 43.5 | 61.6 | 70.4 |

| C corporation | 73.9 | 42.3 | 49.7 | 82.3 | 79.7 | 39.6 | 58.9 | 81.9 |

Note. Data are weighted to adjust for differences in sampling and response rates and reflect population rather than sample measures.

1. Percentage of firms that used either a personal or business credit card. Return to table

2. Percentage of firms using either a personal or business credit card that paid off their credit card balances each month. Return to table

3. Number of owners working in the business plus number of full- and part-time workers. Return to table

Source. 2003 Survey of Small Business Finances.

In the past five years, the use of business credit cards has grown faster than the use of personal credit cards, probably because of aggressive marketing by credit card companies. In 1998, 34.1 percent of small businesses used business credit cards; by 2003, this figure had increased to 48.1 percent. During the same period, the use of personal credit cards increased less than 1 percentage point. Business use was on par with personal use by 2003: 48.1 percent of surveyed firms reported using business credit cards, and 46.7 percent reported using personal credit cards. The use of each of these credit card types differs by size of firm. Business use of personal credit cards decreased as firm size increased, whereas the use of business credit cards increased with firm size. In 2003, only the smallest businesses, those with fewer than five employees, used personal credit cards more than business credit cards. This difference may indicate that small firms have more difficulty than larger firms in obtaining business credit cards and therefore use personal cards as a substitute.

In 2003, businesses that used either personal or business credit cards on average charged $3,100 of new business expenses each month. On personal cards, monthly charges averaged $1,200, whereas on business cards monthly charges averaged $1,900. In 1998, new charges to personal or business credit cards averaged $2,200, with $1,000 charged to personal credit cards and $1,200 charged to business credit cards. Hence, most of the growth in the average charges to credit cards is due to increased use of business credit cards. Despite this increased use, the majority (70.7 percent) of these firms reported that they paid their credit card balance in full each month. Such behavior suggests that most firms used credit cards for convenience and not as a substitute for traditional credit products. Smaller and younger firms, which are most likely to have difficulty obtaining traditional forms of credit, were more likely to carry balances on their credit cards. For example, roughly 70 percent of firms with fewer than ten employees paid their balances in full each month, compared with more than 90 percent of firms with fifty or more employees.

Trade Credit

Trade credit arises when a business purchases goods or services for which payment is delayed. Like credit cards, firms can use trade credit either as a form of credit or as a convenient alternative to paying cash each time a purchase is made. In 2003, 60.1 percent of small businesses used trade credit, about the same proportion that used credit lines, loans, or capital leases but much smaller than the proportion of firms that used credit cards (table A.10). The use of trade credit was virtually unchanged between 1998 and 2003.

Trade credit is generally extended for an intermediate period (30-60 days), at which point payment is due. When payment is not made by the due date, financing charges are applied, and trade credit becomes an alternative method of financing business expenses. Trade credit can be a very costly form of credit for firms that do not make timely payment. According to the 2003 SSBF, 41 percent of firms that used trade credit paid after the due date. Frequently, suppliers will offer cash discounts (typically 1 percent to 2 percent of the purchase price) for early payment, normally five, ten, or fifteen days after delivery. According to the same data from the SSBF, 53 percent of firms that used trade credit were offered such cash discounts by one or more of their suppliers. Of these firms that were offered cash discounts, 80.2 percent took advantage of the discounts by making quick payment.

As shown in table A.10, trade credit was used more extensively by larger firms (more than 85 percent of small businesses with between 100 and 499 employees used trade credit in 2003) and by corporations (more than 70 percent of S and C corporations used trade credit, compared with less than 50 percent of proprietorships).

The substitution of trade credit for traditional types of credit shows a different pattern than the overall use of trade credit. Larger small businesses paid off trade credit after the due date more frequently than smaller firms. This behavior indicates that larger small businesses used trade credit more frequently than smaller firms as a form of credit and not just as a convenient way to pay for transactions. Younger firms were also less likely to take advantage of cash discounts for early payment when discounts were offered by suppliers.

Loans from Owners

Members of partnerships and owners of corporations may rely on themselves as an alternative source of credit by making personal loans to their businesses.18 Though perhaps not feasible for all small businesses, as some business owners may have insufficient wealth, this form of finance represents another alternative to the traditional forms of credit.

In some instances, owner loans may serve different functions than traditional credit loans. For example, an owner may form a corporation and pay herself a salary. At the end of the year, the owner forgoes the salary in lieu of a loan to the firm. Such behavior generally occurs in firms with cash-flow problems or in the initial stages of a firm's existence, before the venture becomes profitable. Loans from owners are different from the other types of credit in that owner loans have elements of both credit and equity. Specifically, in cases of firm liquidation, creditors have senior claims to equity holders, so owners with loans to the firm are more likely to receive money from the liquidation of the firm than owners without such loans.

Small business owners made loans to 30.3 percent of small businesses organized as either partnerships or corporations in 2003. As shown in the last column of table A.10, these loans were used more often by small corporations (more than 30 percent of S and C corporations had owner loans in 2003) than by partnerships (25.2 percent). Among firms that used owner loans, both the number of loans per firm and the size of the principal of those loans increased with firm size, possibly as a result of the greater capital needs of larger firms.

Owner loans were somewhat more likely to be used by younger firms than by older firms, a possible indication of another instance in which younger firms tend to rely on alternatives to traditional credit products. The use of owner loans was almost unchanged between 1998 (28 percent of small firms had one or more owner loans) and 2003 (30 percent).

Summary of Credit Use

The use of credit products exhibited several clear patterns. Among small businesses, larger firms were more likely than smaller firms to use each of the traditional credit types. However, whether this pattern reflects a greater need for credit at larger firms or whether lenders are simply more willing to extend credit to larger firms is unclear.

The relationship between firm age and credit use is similar to the relationship between size and use in that younger firms use fewer credit products. At the same time, however, the use of some traditional credit products declines with firm age. Specifically, leases and other loans were more likely to be used by younger firms, whereas lines of credit, vehicle loans, and equipment loans were more likely to be used by older firms. Several factors may explain the similarities and differences in the relationship between size and credit use and between firm age and credit use. The similarities are likely due to a correlation between firm size and age. The differences are likely related to the greater informational opacity of younger and smaller firms. This characteristic might make evaluating creditworthiness more difficult for lenders, which could reduce the supply of some types of credit available to small and young firms.

Patterns of credit use by small businesses observed in data from the 1998 and 2003 SSBFs were similar. The most significant differences in the use of traditional credit products involved the increased use of lines of credit, which could be due to in part to some institutions relying more heavily on credit scoring to evaluate certain loan applications (discussed in a later chapter). Among the alternatives to traditional credit products, only credit cards, specifically business credit cards, showed notable increases, although the percentage of firms carrying balances month to month on their cards was low and approximately constant over the two surveys.

Credit Application Experience

In some cases, small businesses may have wanted to use more credit than was reflected on the survey but were unable to obtain it. The analysis in this section looks at the experience of firms that sought to obtain credit but had their applications denied.

As shown in table A.9, 21.4 percent of small firms applied for new credit between 2000 and 2003.19 Larger firms applied for new credit with greater frequency than smaller or older firms. More than 41 percent of firms with between 100 and 499 employees applied for new credit over this period, more than three times the 13.5 percent of firms with fewer than two employees.

Success also varied with firm size. Larger firms were more likely than smaller firms to have their loans approved. More than 90 percent of firms with 100 to 499 employees that applied once for credit had their application approved, and 90.6 percent of such firms that applied more than once had all their applications approved. These approval rates are higher than those for firms with fewer than two employees: 89.4 percent of such firms that applied once for credit, and 67 percent of those that applied multiple times, had all their loans approved.

Although application rates did not vary much with firm age, younger firms were less likely to have one or more of their applications for credit approved. Of the firms with fewer than five years under current ownership, 84.5 percent of those that applied once for credit had their application approved, and 48 percent of such firms that applied more than once had all of their applications approved. Firms with twenty-five years or more under current ownership were more successful at applying for credit, with 86.8 percent of the single-application firms being approved and 80.1 percent of the multiple-application firms having all applications approved.

In addition to self-reported application experiences, the SSBF obtained business credit scores for surveyed businesses from Dun and Bradstreet.20 The credit-score data support the hypothesis that smaller and younger firms may be riskier than other firms. Younger and smaller firms have lower (that is, more risky) credit scores than older and larger firms. For example, firms with fewer than five years under current ownership had an average credit score of 44; those with more than twenty-five years under current ownership had an average score of 61. And firms with fewer than four employees had an average score of 48, while those with more than fifty employees had an average score of 58. Moreover, firms that applied for credit and had at least one application denied had an average credit score of 32, much lower than the average score--56--for those firms that applied for credit and had all of their applications approved.

Thus, the evidence regarding loan application experiences of small businesses and the finding that smaller and younger firms have their loan applications approved less frequently are consistent with the conventional wisdom that these firms are riskier, have shorter credit histories or less collateral to pledge as security, and are more informationally opaque.

Unfortunately, one cannot tell from the survey data whether the firms that had credit applications denied were able to obtain financing from other sources. Even so, unless all denied credit applications were approved elsewhere, the data on the application experience of firms indicate that the demand for credit by some small businesses may have been higher than suggested by the credit-utilization data. Because smaller and younger firms have their applications denied more frequently than their larger and older peers, the difference between credit demand and ultimate use should be greater at smaller firms.

Besides the firms that were denied credit, some firms that may have wanted additional credit may not have applied because they expected that their applications would be denied. The 2003 SSBF asked respondents whether they had forgone applying for needed credit because of the expectation of denial. According to those results, in 2003, only 18 percent of small businesses responded affirmatively to this question, down from the 23 percent that did so in 1998. These data indicate a pattern similar to that observed in the data on application denial rates; younger and smaller firms were more likely to forgo applying for credit.21 The expectation of denial was particularly strong among the youngest firms, those with fewer than five years under current ownership: More than 26 percent did not apply for credit because they expected to be denied. These data suggest that the demand for credit at smaller and younger small businesses may have been higher than the data on credit use suggest. However, firms that expected denial may not have been shut out of the market. Firms that reported not having applied for needed credit at some point in the previous three years actually applied for credit nearly twice as often as firms that did not expect their applications to be turned down.

Providers of Credit Lines, Loans, and Leases to Small Businesses

In this section, the providers of small business credit are examined. These providers include commercial banks, savings institutions, credit unions, finance companies, nonfinancial firms, and individuals such as a family member or a friend. Because commercial banks are the leading source of credit to small businesses, this analysis focuses largely on their activity. The section examines the relationship between bank size and small business lending, and it discusses the industrywide structure of small business lending activity. These issues provide insight into the availability of credit to small businesses. The section also presents a more modest analysis of small business lending by savings institutions, which account for substantially less small business credit than commercial banks.

Overview

According to the 2003 SSBF, more than 60 percent of small businesses had outstanding credit lines, loans, or leases, an increase from the 55 percent of such businesses reporting outstanding credit in 1998. Commercial banks provided credit lines, loans, or leases to 41.1 percent of small firms, a proportion that corresponds to about 68 percent of the small firms that obtained a traditional form of credit from any source (table A.4). In addition, 5.5 percent of small businesses obtained traditional credit from a savings bank or a savings and loan association, and 3.9 percent obtained it from a credit union. In total, depository institutions supplied credit to more than three-fourths of the businesses that reported outstanding credit.

Nondepository sources, which include nondepository financial suppliers and nonfinancial suppliers, provided credit to about one-third of small businesses in 2003, an increase from the nearly 27 percent of firms that used nondepositories in 1998. The key sources among nondepository financial suppliers were finance companies (22.2 percent of firms) and leasing companies (4.3 percent). Family and individuals (6.5 percent) were the most important nonfinancial source of credit.

Commercial banks were, by a wide margin, the most common source of virtually every credit product included in the survey. They supplied more small businesses with lines of credit, mortgage loans, and equipment loans than any other type of provider. They were also the second most common supplier of motor vehicle loans and "other" loans.22

Finance companies were the most important sources of motor vehicle loans and leases, whereas family and friends were the most important sources of other loans.

In terms of the aggregate dollars outstanding, commercial banks provided 56.8 percent of the outstanding amount of lines of credit, loans, and leases used by small businesses (table A.5). Banks accounted for the largest dollar share of credit lines, mortgages, equipment loans, and other loans. Finance companies, the largest nonbank suppliers, accounted for 16.2 percent of aggregate dollars outstanding. Although most of these loans were for motor vehicles, motor vehicle loans extended by finance companies accounted for only 2.5 percent of aggregate dollars, whereas mortgages and lines of credit extended by such companies each accounted for about 4 percent of aggregate dollars. Thrifts and credit unions accounted for 6.9 percent of aggregate dollars outstanding, and most of the outstanding dollars were associated with mortgage loans. Altogether, depository institutions provided nearly two-thirds of the outstanding balances of loans, lines, and leases used by small businesses.

Lending by Depository Institutions

Beyond survey data, an important source of information on the small business lending activities of commercial banks and savings institutions is the small business loan data collected by the Federal Reserve and other regulatory agencies on the midyear Reports of Condition and Income (Call Reports) and midyear Thrift Financial Reports (TFRs).23 These data, which have been collected as of June 30 since 1993, include information on outstanding small commercial and industrial loans and loans secured by nonfarm, nonresidential properties.24 The number of loans and amount outstanding are collected for loans with original amounts of $100,000 or less, more than $100,000 through $250,000, and more than $250,000 through $1 million.25

These data are used to estimate the amount of credit extended to small firms because loan size is often used as a proxy for the size of the firm receiving credit. However, this approach to measuring small business lending introduces two sources of inaccuracy in the measurement of the number and dollar amount of loans to small businesses. First, the data likely include loans equal to or less than $1 million extended to large firms, and second, the data exclude loans of more than $1 million made to small firms.26

The latter source of inaccuracy probably has a greater net effect and results in an undercounting of small business lending. According to the 2003 SSBF, only about 3.5 percent of credit-line extensions to small businesses were associated with commitments greater than $1 million. However, these relatively few loan extensions accounted for roughly 66 percent of the dollar value of credit-line commitments to small businesses. Although a large share of the value of small business loans may be excluded from Call Report and TFR data, these loans are not typical of the credit obtained by the majority of small firms.27

Commercial Banks

Commercial banks are the leading providers of credit to small firms.28 Lending to small businesses involves unique challenges that banks are particularly well suited to meet. Of particular significance, information on the financial condition, performance, and prospects of small firms is not readily available, so lending is often based heavily on information gathered through established relationships, which banks and their staff frequently have with small firms and their owners.

Bank Size

The relationship between bank size and the extent to which banks engage in small business lending may have implications for the availability of credit to small firms. Substantial consolidation in the banking industry over the past twenty years has dramatically reduced the number of banks, increasing the importance of large banks and the concentration of industry assets.29 For example, more than 4,200 bank mergers involving acquired assets in excess of $4.2 trillion were completed between 1994 and 2006.30 Even though more than 1,700 new banks were granted charters over this period, the total number of bank organizations fell nearly one-fourth, to 6,229 (table 5).

| Year (as of June 30) |

Number | Total assets held by insured U.S. commercial banks (billions of dollars) | Share of domestic commercial banking assets held by the largest organizations (percent) | ||||

|---|---|---|---|---|---|---|---|

| Commercial banking organizations1 | Insured U.S. commercial banks | Top 10 | Top 25 | Top 50 | Top 100 | ||

| 1994 | 8,102 | 10,552 | 3,311 | 27.5 | 45.7 | 60.2 | 71.2 |

| 1998 | 6,930 | 8,810 | 4,286 | 35.1 | 54.2 | 67.6 | 75.6 |

| 2002 | 6,455 | 7,800 | 5,590 | 45.2 | 61.0 | 71.1 | 77.5 |

| 2006 | 6,229 | 7,327 | 7,920 | 49.7 | 64.3 | 73.7 | 79.1 |

Note. Includes insured U.S. domestically chartered banks excluding credit card institutions.

1. Commercial banking organizations include bank holding companies and independent banks. Return to table

Source. Call Reports (June 30), various years, and the National Information Center database.