Report to the Congress on Risk Retention

Sections of this Page

- Executive Summary

- Introduction

- General Description of Asset Classes

- Issuance Activity

- Mechanisms to Align Incentives and Mitigate Risk

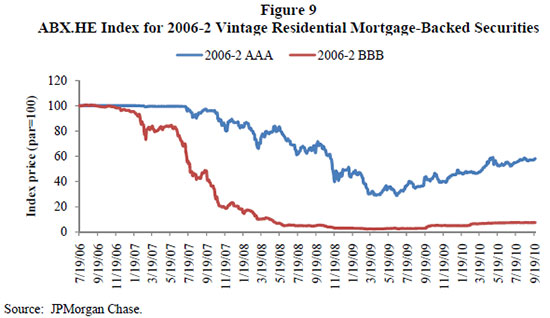

- Relative Performance during the Crisis

- Interaction of Risk Retention and Accounting Standards

- Summary of Current Sale Accounting and Consolidation Requirements

- Current Consolidation Practices by Asset Class

- Potential Interaction between Risk Retention and Accounting Treatment

- Accounting Treatment of Vertical versus Horizontal Risk Retention

- Discussion of Regulatory Capital Treatment

- Identifying Potential for Effect on Current Market Practice

- Potential Regulatory Effects on Mandated Risk Retention

- Increasing the Market for Federally Subsidized Loans

- Recommendations

- Appendix

October 2010

Submitted to the Congress pursuant to section 941 of the Dodd–Frank Wall Street Reform and Consumer Protection Act of 2010

Executive Summary

Section 941(c) of the Dodd–Frank Wall Street Reform and Consumer Protection Act (the Act, or Dodd–Frank Act) requires that the Board of Governors of the Federal Reserve System (the Board) conduct a study and issue a report not later than 90 days after the date of enactment on the effect of the new risk retention requirements to be developed and implemented by the federal agencies, and of Statements of Financial Accounting Standards Nos. 166 and 167 (FAS 166 and 167).1, 2

The federal agencies have an additional 180 days from the date of this report to adopt rules to implement the risk retention requirements of section 941. The agencies are continuing to develop these regulations, and thus the effects of a final set of risk retention requirements cannot be analyzed at this time. This report provides information and analysis on the impact of various risk retention and incentive alignment practices for individual classes of asset-backed securities both before and after the recent financial crisis.

The study defines and focuses on eight loan categories and on asset-backed commercial paper (ABCP). ABCP can be backed by a variety of collateral types but represents a sufficiently distinct structure that it warrants separate consideration. These nine categories, which together account for a significant amount of securitization activity, are

- Nonconforming residential mortgages (RMBS)3

- Commercial mortgages (CMBS)

- Credit cards

- Auto loans and leases

- Student loans (both federally guaranteed and privately issued)

- Commercial and industrial bank loans (collateralized loan obligations, or CLOs)

- Equipment loans and leases

- Dealer floorplan loans

- ABCP

For each asset class, the study provides background information, including: a discussion of the economics of securitization, a summary of the underlying collateral, and differences in the securitization "chain" linking originators to investors.

Further, the study examines issuance activity both before and after the crisis. RMBS and CMBS issuance has dropped dramatically since the onset of the financial crisis. In contrast, issuance of most types of consumer and business finance securitizations has rebounded somewhat. However, issuance has recently shifted from the public market to the Rule 144A/private placement market.

The study defines and examines by asset class a number of mechanisms that may improve the alignment of incentives, mitigate credit risk, or both. These mechanisms include retention of securities or underlying loans, overcollateralization, subordination, third-party credit enhancement, representations and warranties, and conditional cash flows. All of these mechanisms involve the securitizer, the originator, or some other party to the securitization process retaining an economic exposure to a securitization. Rulemakers should consider whether these mechanisms are acceptable forms of credit risk retention.

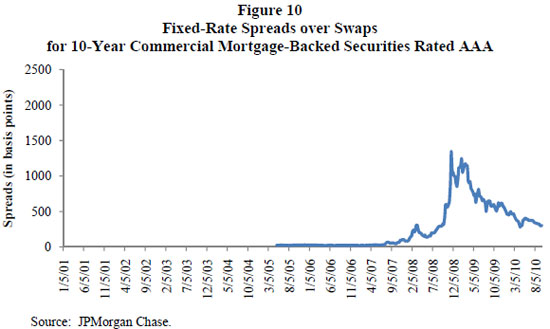

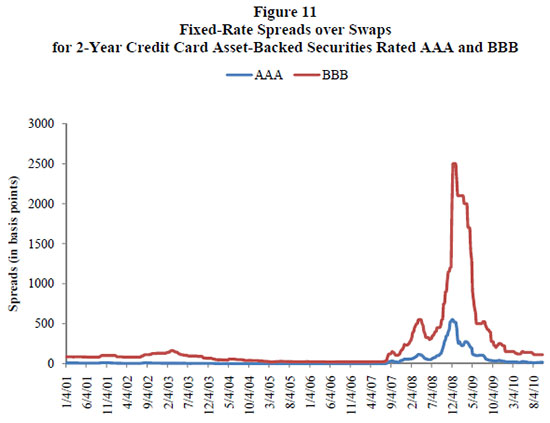

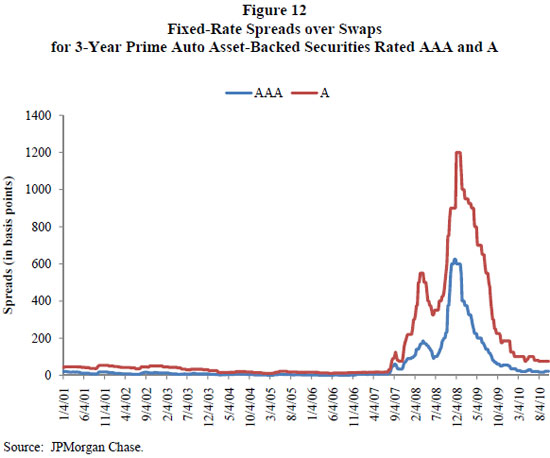

Performance during the crisis varied among asset classes, providing useful evidence on the relative impact of risk retention practices and incentive alignment mechanisms that were in place before the crisis. All asset classes suffered mark-tomarket losses during the crisis as investors, and thus liquidity, fled asset-backed securities (ABS). Widespread defaults, in which contractual payments were not made to bondholders, were largely concentrated in ABS backed by real estate. These losses appear to be driven primarily by the large drop in nominal house prices and its effect on loans made to borrowers with weak credit histories, unverified income, or with nontraditional amortization structures.4 In other cases, such as ABS backed by government student loans, losses were driven by certain problems with the prevalent structures--namely, their reliance on short-term funding markets that were disrupted during the crisis.

The study also addresses the interaction of credit risk retention and accounting standards, including FAS 166 and 167. Depending on the type and amount of risk retention required, a securitizer could become exposed to potentially significant losses of the issuance entity, which could require accounting consolidation when considered with the securitizer's decision making power over the issuance entity. Given the earnings and regulatory capital consequences of maintaining assets on–balance sheet, companies may be encouraged to structure securitization to again achieve off-balance-sheet treatment. For example, institutions may cede the power over ABS issuance entities by selling servicing rights or distancing themselves from their customers primarily to avoid consolidating the assets and liabilities of the issuance entities. Alternatively, the potential interaction of accounting treatment, regulatory capital requirements and new credit risk retention standards may make securitization a less attractive form of financing and may result in lower credit availability.

The extent to which risk retention rules might affect the volume of federally subsidized lending (for example, mortgage, student, and small business loans) varies by type of loan. Because no close private-market substitutes exist at this time for government-guaranteed mortgages or student loans, credit risk retention requirements are unlikely to materially increase the share of government subsidized loans. In contrast, many types of loans to small businesses are routinely securitized in the private market, so the Small Business Administration's (SBA) share of lending is likely to increase if risk retention significantly increases the cost of securitization.

Overall, the study documents considerable heterogeneity across asset classes in securitization chains, deal structure, and incentive alignment mechanisms in place before or after the financial crisis. Thus, this study concludes that simple credit risk retention rules, applied uniformly across assets of all types, are unlikely to achieve the stated objective of the Act--namely, to improve the asset-backed securitization process and protect investors from losses associated with poorly underwritten loans.

Thus, consistent with the flexibility provided in the statute, the Board recommends that rulemakers consider crafting credit risk retention requirements that are tailored to each major class of securitized assets. Such an approach could recognize differences in market practices and conventions, which in many instances exist for sound reasons related to the inherent nature of the type of asset being securitized. Asset class– specific requirements could also more directly address differences in the fundamental incentive problems characteristic of securitizations of each asset type, some of which became evident only during the crisis.

Moreover, the Board recommends that that the following considerations should be taken into account by the agencies responsible for implementing the credit risk retention requirements of the Act in order to help ensure that the regulations promote the purposes of the Act without unnecessarily reducing the supply of credit. Specifically, the rulemaking agencies should:

- Consider the specific incentive alignment problems to be addressed by each credit risk retention requirement established under the jointly prescribed rules.

- Consider the economics of asset classes and securitization structure in designing credit risk retention requirements.

- Consider the potential effect of credit risk retention requirements on the capacity of smaller market participants to comply and remain active in the securitization market.

- Consider the potential for other incentive alignment mechanisms to function as either an alternative or a complement to mandated credit risk retention.

- Consider the interaction of credit risk retention with both accounting treatment and regulatory capital requirements.

- Consider credit risk retention requirements in the context of all the rulemakings required under the Dodd–Frank Act, some of which might magnify the effect of, or influence, the optimal form of credit risk retention requirements.

- Consider that investors may appropriately demand that originators and securitizers hold alternate forms of risk retention beyond that required by the credit risk retention regulations.

- Consider that capital markets are, and should remain, dynamic, and thus periodic adjustments to any credit risk retention requirement may be necessary to ensure that the requirements remain effective over the longer term, and do not provide undue incentives to move intermediation into other venues where such requirements are less stringent or may not apply.

Introduction

Section 941(b) of the Dodd–Frank Wall Street Reform and Consumer Protection Act (the Act, or Dodd–Frank Act) imposes certain credit risk retention obligations on securitizers or originators of assets securitized through the issuance of asset-backed securities (ABS).5 Section 941 of the Act also requires a number of federal agencies, including the Board of Governors of the Federal Reserve System (the Board), to jointly prescribe regulations implementing the credit risk retention requirements of section 941 of the Act. The implementing regulations must be jointly prescribed by the federal agencies within 270 days of the date of enactment of the Act (which was July 21, 2010). The Act requires that the regulations "establish asset classes with separate rules for securitizers of different classes of assets, including residential mortgages, commercial mortgages, commercial loans, auto loans, and any other asset classes that the Federal banking agencies and the [Securities and Exchange] Commission deem appropriate."6

Section 941(c) of the Act requires that the Board conduct a study and issue a report not later than 90 days after the date of enactment on the effect of the new risk retention requirements to be developed and implemented by the agencies, and of Financial Accounting Standards (FAS) 166 and 167. Specifically, section 941(c) provides as follows:

(c) Study on Risk Retention.--

- Study.--The Board of Governors of the Federal Reserve System, in coordination and consultation with the Comptroller of the Currency, the Director of the Office of Thrift Supervision, the Chairperson of the Federal Deposit Insurance Corporation, and the Securities and Exchange Commission shall conduct a study of the combined impact on each individual class of asset-backed security established under section 15G(c)(2) of the Securities Exchange Act of 1934, as added by subsection (b), of--

- the new credit risk retention requirements contained in the amendment made by subsection (b), including the effect credit risk retention requirements have on increasing the market for Federally subsidized loans; and

- the Financial Accounting Statements 166 and 167 issued by the Financial Accounting Standards Board.

- Report.--Not later than 90 days after the date of enactment of this Act, the Board of Governors of the Federal Reserve System shall submit to Congress a report on the study conducted under paragraph (1). Such report shall include statutory and regulatory recommendations for eliminating any negative impacts on the continued viability of the asset-backed securitization markets and on the availability of credit for new lending identified by the study conducted under paragraph (1).7

Section 941 is intended to help align the interests of key participants in the securitization process, notably securitizers and originators of the assets underlying an ABS transaction, with the interests of investors. The Act requires, as a general matter, that the securitizer or originator retain some of the credit risk of the assets being securitized. By retaining a portion of the credit risk, the securitizer and/or originator will have an incentive to exercise due care in making underwriting decisions, or in selecting assets for securitization purchased from the entities making such decisions. In circumstances where the underlying assets are otherwise underwritten in accordance with sound underwriting standards, the statute expressly provides or allows for exceptions from the risk retention requirement, recognizing that in these circumstances additional incentives to promote the quality of the assets being securitized may not be needed.

The federal agencies have an additional 180 days from the date of this report to adopt rules to implement the risk retention requirements of section 941. The agencies are continuing to develop these regulations, and thus the effects of a final set of risk retention requirements cannot be analyzed at this time. This report provides information and analysis on risk retention and incentive alignment practices for individual classes of asset-backed securities.

Definitions of Asset Categories

This report focuses on securities backed by eight loan categories and on asset-backed commercial paper (ABCP). ABCP can be backed by a variety of collateral types but represents a sufficiently distinct structure that it warrants separate consideration. These categories account for the bulk of the ABS market, excluding mortgage-backed securities guaranteed by the housing-related government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac. In terms of overall new debt issuance, mortgage-related and other asset-backed securities represent a significant proportion (16 percent) during the period between 2002 and 2010.8

The classes of collateral considered in the report are as follows:

- Nonconforming residential mortgages (RMBS)9

- Commercial mortgages (CMBS)

- Credit cards

- Auto loans and leases

- Student loans (both federally guaranteed and privately issued)

- Commercial and industrial bank loans (collateralized loan obligations, or CLOs)

- Equipment loans and leases

- Dealer floorplan loans

- ABCP

Asset classes are further grouped into three broad sectors: real estate (RMBS and CMBS), consumer finance (credit cards, auto loans and leases, and student loans), and business finance (CLOs, equipment loans and leases, and dealer floorplan loans). ABCP is considered separately.

The study does not explicitly address resecuritizations, such as collateralized debt obligations (CDOs) backed by ABS or re-REMICs (resecuritizations of real estate mortgage investment conduits). Given that the credit risk retention provisions of the Act are intended to influence the quality of assets being securitized, it is appropriate for the study to focus on primary securitizations though further analysis of re-securitizations in the context of final rulemaking would be worthwhile.

Because section 941 of the Act exempts RMBS that are backed by mortgages that are insured or guaranteed by a federal agency from the credit risk retention requirements, securitizations backed by the Department of Veterans Affairs (VA), the Federal Housing Administration (FHA), and other agency-guaranteed or agency-insured loans are not in the asset classes defined above. While the statute does not provide a similar exemption for RMBS guaranteed by the housing-related GSEs (Fannie Mae, Freddie Mac, and the Federal Home Loan Banks), these securitizations also are not included within the nonconforming RMBS category as defined for purposes of this report. These entities retained all of the credit risk for the mortgages they securitized; hence, their experience and practices likely offer limited insight regarding the effect of credit risk retention by securitizers when significant credit risk is transferred to ABS investors.

Many other financial assets have been routinely securitized, including utility fees, tax liens, insurance premium finance loans, and aircraft and railcar loans and leases.

Some of these smaller-volume types of securitizations share many features with the nine broad categories enumerated earlier; for example, securities backed by insurance premium finance loans are structured much like securities backed by credit card loans.10 Nevertheless, some asset categories may provide important sources of funding to particular markets but may not easily inserted into the framework considered here because of idiosyncratic features. In addition, new loan types may materialize over time and securitization markets will develop around them.

Overview of Securitization

This section describes the basic mechanics and economics of securitization, defines terms that will be used throughout the report, and briefly highlights the potential for misaligned incentives and information asymmetry in the securitization process.

The term "securitization" generally refers to two separate, though related, activities. First, a financial institution is said to have securitized a pool of financial assets (for example, loans) when it creates securities backed by the cash flows from those assets and sells some or all of these securities to investors. The financial institution may or may not retain responsibility for "servicing"--providing on an ongoing basis some or all of the services necessary to collect payments from borrowers, monitor performance of the loans and distribute the cash flows generated to investors. Second, securitization may also refer, more narrowly, to the process of creating multiple securities with different payment priorities from a pool of underlying loans. For example, a pool of loans may be transformed into a senior tranche that is first in line to receive cash flows and a junior tranche that is last in line to receive cash flows.11

Securitization provides economic benefits that may lower the cost of credit to households and businesses. These benefits come from a reduction in the cost of funding, which is accomplished through several different mechanisms. First, firms that specialize in originating new loans and that have more difficulty funding existing loans may use securitization to access more-liquid capital markets for funding. Second, securitization can also create opportunities for more efficient management of the asset–liability duration mismatch generally associated with the funding of long-term loans, for example, with short-term bank deposits. Third, securitization allows the structuring of securities with differing maturity and credit risk profiles from a single pool of assets that appeal to a broad range of investors. Fourth, securitization that involves the transfer of credit risk allows financial institutions that primarily originate loans to particular classes of borrowers, or in particular geographic areas, to limit concentrated exposure to these idiosyncratic risks on their balance sheets.

These benefits are not without cost, however. In particular, during the financial crisis securitization also displayed significant vulnerabilities to informational and incentive problems among various parties involved in the process. The ramifications of these problems have had and continue to have profound effects on many American households.

Mechanics of Asset Sales

Section 941 of the Act defines a "securitizer" to mean "(a) an issuer of an asset-backed security or (b) a person who organizes and initiates an asset-backed securities transaction by selling or transferring assets, either directly or indirectly, including through an affiliate, to the issuer." The bill defines an "originator" to mean a person who "(a) through extension of credit or otherwise, creates a financial asset that collateralizes an asset-backed security and (b) sells an asset directly or indirectly to a securitizer."

Throughout, this report uses these definitions of originator and securitizer. However, many others participate in the securitization process, and originators and securitizers can play additional roles in the securitization process. Later, participants are further delineated into aggregators, servicers and underwriters.

An originator makes the initial decision about whether, and on what terms, to extend credit to a household or business and provides initial short-term funding. Originators include banks, thrifts, subsidiaries of bank or thrift holding companies, independent finance companies, and finance companies affiliated with vehicle, equipment, or other types of manufacturers.

The originator may securitize the loans directly or sell them to an aggregator that may buy loans from many different originators. Aggregators are intermediaries between originators and securitizers, and loans may pass through several such parties' hands before being securitized. Certain periods have seen active wholesale markets for pools of loans suitable for securitization.

The securitizer oversees the creation and sale of the securities backed by loans purchased from originators and aggregators. This process has several components, which may sometimes be divided among separate firms, although this report will generally treat them as if carried out by a single entity.

The securitizer performs the legal and economic requirements for a securitization, including: reviewing loan documents and origination standards, handling any required registration of offer and the sale ABS with the Securities and Exchange Commission (SEC) if a public offering is contemplated, and selling the ABS to investors. The securitizer engages one or more credit rating agencies to analyze the transaction and assign ratings to securities that reflect the securities' likelihood of default and expected loss given default. Finally, the securitizer hires an investment bank as an underwriter to market the deal, to assist in preparation of the offering documents, to conduct due diligence, and to find investors to purchase the securities. For many ABS transactions, the underwriter and the securitizer are affiliated.

At many stages of the securitization process, originators and securitizers may use interim funding, including ABCP conduits and warehouse lines of credit. Warehouse lines of credit are short-term loans, usually collateralized by the assets being securitized. In some cases, the transaction may be structured in a manner similar to a repurchase agreement, a transaction that involves a sale and subsequent repurchase but has the economics of collateralized borrowing. Often the warehouse lender is also an affiliate of the underwriter in the securitization.

A critical part of the securitization process is structuring the transaction so that the bankruptcy, receivership, or insolvency of parties to the transaction, including the originator, any aggregators and the securitizer, will not affect the ability of the holders of the securities to be paid according to the terms of the securitization. Generally, the structuring involves the sale of the assets to a bankruptcy-remote entity that in turn transfers the assets to either a one-time special purpose vehicle (SPV) created specifically for an individual securitization, or to a master trust that issues new liabilities on an ongoing basis. This latter arrangement is more common for short-maturity, revolving loans such as credit cards or floorplan loans. The key aim of establishing such separation is that the assets transferred into the securitization cannot be seized by creditors upon the bankruptcy or failure of the transferors of such assets. Thus, investors may demand a lower risk premium to purchase the ABS relative to the corporate debt of the parties involved in the transaction, including the originator and securitizer.

Structure of Securities

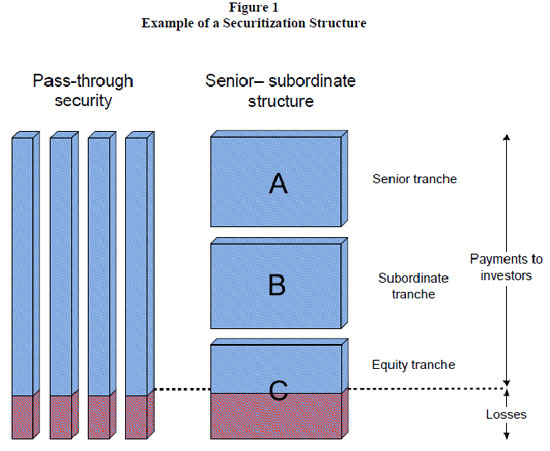

The simplest security that a financial institution can create from a pool of loans is a so-called pass-through security. Cash flows from the assets in the pool are distributed on a pro-rata basis to the holders of the securities, much as mutual fund investors receive a share in the gains and losses on a pool of assets. The bulk of these gains and losses are the principal and interest payments made by the underlying borrowers on their loans. If an underlying loan defaults, all investors in a pass-through structure share in the loss equally. Similarly, if a loan prepays, all investors share in the retired principal equally.

This structure is illustrated schematically in the left panel of figure 1. As an example, assume the pool consists of 400 loans. The four bars represent four equal shares in a pass-through security that has been created from the 400 loans. Each pass-through security represents an equal share in the cash flows of the underlying loans. As a result, if the total outstanding principal of the 400 loans is $400, the outstanding principal balance of each pass-through security is $100. As principal and interest payments are received on the 400 loans, one-fourth of these payments are directed to each pass-through security. Loan defaults are also shared proportionally among the securities. In the example, assume 67 of the 400 loans have defaulted. As a result, each pass-through security suffers a reduction in principal of $16.75, which is depicted in red at the bottom of each bar representing a pass-through security in figure 1. In addition to the reduction in principal, each pass-through security loses the interest payments that would otherwise have been made over the life of the loan.

While the pass-through structure just described is rather straightforward, it is neither the only nor the most common way that underlying cash flows are distributed to investors in a securitization. Many securitization structures distribute cash flows to investors through a process commonly referred to as tranching. In a tranched securitization, the underlying cash flows are allocated to different securities, or tranches, according to a pre-specified prioritization rule, or "waterfall."

A simple "senior subordinate" securitization made up of three distinct classes, or "tranches," is depicted in the right panel of figure 1. In this example, each tranche represents a distinct security with an initial principal balance of $133.33. The three securities, labeled A, B, and C, are referred to as the senior security (A), the subordinate security (B), and the equity security (C). In the senior-subordinate securitization, cash flows from the underlying loans are received by the holders of the senior security until the entire principal balance of the senior security is repaid. After all principal has been repaid to the senior security, loan cash flows are received by the holders of the subordinate security until the entire principal balance of the subordinate security is fully repaid. Once the entire principal balance of the subordinate security has been repaid, all remaining cash flows are received by the holders of the equity security.

Since cash flows are distributed to some securities before others, default losses on the underlying loans are not shared proportionally among the three securities. All losses are initially absorbed by the equity security. Only if losses exceed the principal balance of this equity security, $133.33 in this example, will the subordinate security absorb any losses. Finally, only if losses are larger than the combined principal balance of the equity and subordinate tranches, $266.67 in this example, will the senior security absorb any losses. In figure 1, the loan defaults of $66.67, depicted in red, are large enough to cause losses to the equity security but not large enough to cause losses to either the subordinate or senior security.

The precise size and number of tranches is a key design feature of any securitization. As an example, the securitization could be designed so that the equity security is large enough to absorb losses associated with a normal recession, and the equity and subordinate securities combined are large enough to absorb losses associated with a severe recession. The subordinate tranche could thus be marketed as robust to a normal recession and the senior tranche could be marketed as robust to a severe recession.12

Theoretically, if all investors are equally well informed about the outlook for loan losses in recessions and have a common appetite for risk, the pass-through and the senior-subordinate securities would, in the aggregate, trade at the same price in the market. In the earlier pass-through example, the sum of the prices of the pass-through securities would be equal to the sum of the prices of the securities in the senior-subordinate structure, reflecting the fact that both sets of securities are backed by the same underlying assets, which will generate the same cash flows. However, in practice, the sum of the prices of the senior-subordinate securities is likely to differ from the sum of the prices of the pass-through securities because investors differ in their risk appetites and expertise with respect to various loan markets. The pass-through security shown here is, of course, highly stylized and omits many important institutional details.

Creating different securities, via a senior-subordinate structure, that appeal to different types of investors can increase the proceeds from underwriting securities backed by a particular pool of assets or, equivalently, reduce the cost of funding the structure. Thus a pool of loans may, in total, be worth more when securitized using a senior-subordinate structure than when using a pass-through structure. Investors specializing in understanding the risk of the underlying loans may find the risk–return profile of the bottommost tranche of certain senior-subordinate securities attractive, because of the assets in the pool, the structure of the securities, or some combination of factors. In addition, some investors might want to acquire assets that pay a high rate of return in periods of economic growth as part of a broader investment strategy. Such investors would be interested in the lower two tranches of the security. Finally, some types of investors would be interested in the relatively safe top tranche, either because of restrictions on the types of securities that they can purchase or because of a low appetite for risk. The return on this senior tranche might be expected to be relatively insensitive to changes in the aggregate state of the economy, barring a historically severe recession.

The information necessary to design senior-subordinate structures far exceeds the requirements for simpler pass-through structures. To generate the desired performance, the amount of subordination protecting the top tranche has to be estimated based on data that, until recently, did not contain information on the performance of many types of loans during a severe recession. If these subordination levels prove inadequate to protect the senior tranches of securities in one asset class, investors might doubt the protection levels in other asset classes, eroding the funding advantage that typically results when loans are securitized. Indeed, the senior-subordinate structure adds economic value relative to simpler structures only to the extent that investors trust that the different subordination levels result in meaningful risk and return opportunities to accommodate a range of risk appetites. The subordination levels are generally set by the securitizer in order to obtain a desired rating from a credit rating agency. The potential incentive problems inherent in this arrangement are beyond the scope of this study and are addressed elsewhere in the Act.13

Loans with relatively short maturities or open-ended loans, such as credit cards, are usually securitized using a master trust structure. While similar in principle to the senior-subordinate structure shown in figure 1, master trusts are backed by a constantly changing pool of loans and periodically issue (and retire) senior tranches. The juniormost tranche of such securities, as well as a vertical slice of the portfolio in the master trust, is usually retained by the securitizer, in part to reassure investors about the continuing quality of assets placed in the pool.

Incentive and Information Issues in Securitization

Many parties in the securitization chain have access to information not easily made available to investors in the final securities. For example, originators may have nonpublic, hard-to-acquire or "soft" information about borrowers based on other transactions with them. In addition, participants in the securitization chain may be able to affect the value of the securities in opaque ways, both before and after the sale of the security. For example, securitizers may be able to buy just enough delinquent loans out of a trust so that the deal passes performance triggers, releasing cash reserves to the securitizer.

Over time, if an originator sells relatively bad loans to securitizers, or a securitizer markets poorly structured securities or securities backed by relatively bad loans to investors, its reputation will suffer and securities with which the entity is associated will fetch lower prices. In the short run, however, investors, credit rating agencies, and other market participants might find it hard to detect bad loans or bad behavior because differences in loan quality across securities may become apparent only in downturns and may require several years of data to detect. As a result, this reputation effect may not be sufficient to overcome the "adverse selection" problems associated with securitization. Such problems are characteristic of situations in which one party has better or more complete information than do other parties. One possible solution, of course, is increased or enhanced mandated disclosure of information. In the wake of the financial crisis and the poor performance of many ABS, significant initiatives are under way in this area.14

Another source of potential conflict occurs when the originator of the loan continues to service it even after selling it. A loan's servicer negotiates with the underlying borrower in the event of distress and decides, subject to standards set forth in the relevant pooling and servicing agreements, whether to offer the borrower a reduced payment or to pursue the borrower for full repayment. These different strategies benefit different securities holders: Senior tranches usually benefit from aggressive liquidation because principal is returned as quickly as possible, while junior tranches usually benefit from extensions which defer principal losses and extend the period during which payments are received before the principal is written down. If the originator holds a particular tranche and continues to service the underlying loans, it may have an incentive to adopt a particular servicing strategy that benefits the tranche it holds. Of course, by holding the junior most tranche, the originator's incentive to put bad loans into the security is reduced relative to the incentive if the originator holds an interest in a more senior part of the capital structure. This tension is illustrative of the difficulties in simultaneously solving the multiple incentive problems that arise in securitizations: retention of the lower tranche, which provides an incentive for the securitization of higher-quality assets, can also create incentives for the servicer to favor the interests of the holders of the lower tranche over more senior investors.

The fact that incentive problems and informational asymmetries can occur at multiple points in the securitization process does not necessarily mean that protecting investors requires an explicit incentive alignment mechanism for each participant in the chain. As long as at least one party to the chain has sufficient information to detect improper behavior by the other parties in the chain, an incentive alignment mechanism aimed at the informed party should, in turn, induce the informed party to enforce proper behavior by the other members of the chain.

The nature of the significant incentive problems, and the kind of information asymmetry, differs materially across asset classes. In closed-end securitizations, with a static pool of assets, loan quality and servicing may be the most important hidden factors driving the performance of securities. However, in actively managed structures (such as CLOs), where the portfolio composition is subject to ongoing adjustment, the investor faces the problem of properly managing the incentives of the managers delegated to assemble the asset pool.

In response to these varied incentive and information problems, investors have demanded a variety of protective mechanisms that are discussed later in the report in "Mechanisms to Align Incentives and Mitigate Risk." Some of these mechanisms clearly did not perform as investors expected during the strain of the financial crisis.

General Description of Asset Classes

This section provides an overview of the nine categories covered by this report. The section describes the types of assets securitized, any significant subcategories within the asset class, the composition of the securitization chain, and the structure of the resulting securities. Many asset classes contain significant variation even within the asset class; accordingly, this report focuses on the most common structures.

Nonconforming Residential Mortgages

Mortgages are originated to consumers to purchase a house or property or to refinance an existing mortgage. Nonconforming residential mortgages are loans that do not meet the underwriting criteria for securitization by housing-related GSEs. Nonconforming residential mortgages may be held in portfolio or securitized by private institutions.

Nonconforming loans typically fall into one of three major categories. The first is prime loans that exceed the conforming loan limit, known as "jumbo" loans. The second is near-prime loans that feature reduced documentation, non-traditional amortization schedules, or other risk factors. These loans were typically sold into securities marketed as "alt-A." The distinction between jumbo and alt-A deals reportedly became blurred late in the credit boom. The third is loans made to borrowers with weak credit histories, known as subprime loans.

Other types of loans securitized by non-agency institutions include second liens (often referred to as home equity loans, or HELs), and nonperforming or underperforming mortgages (referred to as scratch-and-dent loans) that are purchased at large discounts. These loans are not considered nonconforming residential mortgages for the purpose of this report.15

Financial institutions often originated a junior lien, such as a home equity line of credit (HELOC), at the same time that they originated the first mortgage. Relatively few of these junior liens were securitized; instead, institutions typically held them in portfolio.

Residential mortgages are originated by a wide variety of market participants including banks, nonbank financial institutions, thrifts, finance companies, investment banks and corporate issuers. Nonconforming mortgages, prior to the crisis, were then sold to intermediaries or directly to the securitizer. The typical securitizer was a large bank or investment bank. The resulting securities were purchased by a wide variety of investors, with different types of investors targeting securities with different ratings.

The average size of the typical nonprime securitization (subprime and alt-A securities) was approximately $750 million and included almost 4,000 loans each, although there was wide variation across security type and over time. The average subordination below the triple-A level in these nonprime securitizations ranged from 5 to 20 percent, with lower subordination for ostensibly less risky alt-A deals and higher subordination for subprime deals. In addition, more than 10 percent of nonprime deals had some form of insurance provided by a third party, typically a bond insurer.16

Commercial Mortgages

Commercial mortgages finance commercial properties such as office buildings, hotels, apartment buildings, and retail complexes. The loans included in CMBS tend to be backed by larger commercial properties with well-established rental streams and owners who desire long-term financing. The mortgages are typically 10-year, fixed-rate loans with a 30-year amortization schedule and a large balloon payment at maturity, although these mortgages may also have shorter maturities or may be partially or fully interest-only.

Originators of commercial mortgages include insurance companies, commercial banks, investment banks, and conduit lenders. Loans may be pooled in warehouse facilities maintained by large investment banks prior to securitization. Originators, aggregators, securitizers, and underwriters are typically affiliated with one another and may provide services outside the securitization to other participants involved in the securitization process. For example, the investment bank issuing the security may provide short-term financing to conduit lenders to facilitate the origination and warehousing of loans.

CMBS are broadly divided into three categories: conduit, large-loan deals, and fusion.17 Conduit transactions are composed of a large number, perhaps 150 to 300, of individual fixed-rate commercial loans. Large-loan CMBS are backed by only a few, perhaps 5 to 20, large floating-rate commercial mortgages. Fusion transactions are a hybrid of conduit transactions and large-loan securitizations in which the top 10 mortgage loans usually represent more than 50 percent of the total size of the deal.

Credit Cards

Consumers and small businesses use credit cards to finance purchases of a wide variety of services or merchandise. Credit cards can be classified into three types: general-purpose credit cards, which can be used for purchases of any type and whose balance may be carried over into the next month; general-purpose charge cards, whose balance must be paid in full each month; and retail credit cards, which can be used for purchases only at a specific retailer. Cards are issued almost exclusively by insured depositary institutions, including commercial banks, limited-purpose credit card banks, thrifts, or credit unions. Certain types of these depository institutions may be subsidiaries or affiliates of finance companies or retailers. In a typical credit card securitization, the originator, securitizer, and servicer are affiliated with the same parent entity.

Most credit card ABS use a revolving master trust as the primary securitization structure. Under this structure, one common pool of assets collateralizes all of the outstanding securities. The originator designates credit card accounts that meet certain eligibility criteria as eligible accounts and the outstanding balances on such accounts are sold to the trust, as well as new receivables (the interest payments, principal payments, and fees associated with such account) generated from such accounts. Additional accounts may be allocated to a particular securitization over time. Such new accounts must conform to strict parameters set forth in the securitization documents that are designed to maintain the credit rating of the securities.

The master trust receivables are split between the "investor's interest" and the "seller's interest." The receivables in the investor's interest collateralize the outstanding notes. The seller's interest component absorbs fluctuations in the monthly outstanding loan balances. The seller's interest is a vertical slice of all the receivables in the master trust and receives principal and interest payments in proportion to the share it represents of the master trust. Rating agencies typically require that the seller's interest component be around 4 to 12 percent of the receivables for the ABS to receive an AAA rating.

The credit card ABS issued by the master trust generally have maturities ranging from 1 to 10 years. Initially, investors in these securities receive only interest payments, and the securitizer uses the principal payments to purchase new receivables from the accounts designated to the master trust. Toward the end of the security's life, the principal payments accumulate in an account and are released to the investor in one "bullet" payment at the end.

Auto Loans and Leases

For the purposes of this report, auto loans are loans that are extended to consumers to purchase automobiles, motorcycles, and light trucks. Auto loan ABS are subcategorized into prime, nonprime, and subprime, corresponding to the credit quality of the underlying borrower. The loans are typically fixed rate with maturities up to 84 months.

Auto loans are originated by commercial banks, thrifts, credit unions, "captive" finance company subsidiaries of vehicle manufacturers, and independent finance companies. Finance companies are typically heavily dependent on securitization for funding. Although some banks and thrifts issue auto securitizations, depository institutions tend to hold a large share of their auto loans in portfolio.

Auto leases are an alternative mechanism to allow consumers to finance the acquisition of a vehicle for a fixed period of time, usually 48 months or less. At the end of the lease term, the consumer can either purchase or return the vehicle. The auto lease market is heavily dominated by the captive finance companies.

In both auto loan and auto lease ABS, the participants in the securitization chain--the originator, securitizer, and servicer--are usually affiliated with the same parent entity. On occasion, securitizers have purchased whole loans from unrelated originators, structured them, and sold them, although this practice has become less common in the wake of the financial crisis.

The most common securitization structure for auto loan and lease ABS is to have senior and subordinate tranches that pay sequentially. There are usually four triple-A tranches with different maturities, with the shortest tranche having an average life of around three months and the remaining tranches having average lives ranging from one to three years. Among the triple-A tranches, cash flows are directed first exclusively to the tranche with the shortest average life, then to other tranches in order of maturity. This practice is known as "time tranching."

Student Loans

Student loans come in two types--those guaranteed or originated by the federal government, and those without a government guarantee (so-called private loans). The terms and underwriting of government-guaranteed or government-originated loans are set by the federal government. Private loans are typically taken out by students whose educational expenses exceed the government-guaranteed loan limits.

Government-Guaranteed Loans

Historically, government-guaranteed loans were financed in one of two ways. Under the Federal Family Education Loan Program (FFELP), established in 1965, financial institutions originated the loans and the government guaranteed 97 to 100 percent of the principal and accrued interest in the event that the student defaulted on the loan and the loan was serviced in accordance with Department of Education guidelines.18 In 1994, the federal government began originating student loans directly through the William D. Ford Federal Direct Loan Program (FDLP). Each participating college or university could choose whether loans to its students were funded through the FFELP or the FDLP, but the underlying loans offered to students were essentially the same under both programs. On July 1, 2010, the FFELP was eliminated, and all government-guaranteed loans are now originated directly by the federal government.

Although the loans underlying FFELP securitizations are homogeneous, government-guaranteed, and underwritten to government-specified parameters, the securitizations of these loans have historically been surprisingly complex. The ABS can be issued out of discrete trusts or master trusts. Under a discrete trust structure, each security is collateralized by its own pool of assets. Both discrete and master trusts have issued floating-rate notes, auction-rate notes, rate-reset notes, and a variety of other types of securities. The complexity of the structures is due, in part, to uncertainty of the timing of cash flows of the loans, as students can defer payments on their loans while they are in school.

Before the financial crisis, FFELP loans were originated by a variety of commercial banks, thrifts, credit unions, independent finance companies, and nonprofit organizations. Although some of these institutions held the loans on portfolio or securitized the loans themselves, a large majority of the loans were sold to a handful of large banks, finance companies, state agencies, and nonprofit organizations that in turn securitized the loans.

Private Student Loans

Private student loans are a more recent product than FFELP loans. Private student loans are originated and securitized by a much smaller group of financial institutions than FFELP loans, and the secondary market for whole loan sales of private student loans is likewise much less active. For most private loan securitizations, the originator and securitizer are sponsored by the same institution, although at least one of the largest securitizers bought and securitized loans from other financial institutions and acted as an intermediary.

Private student loan securitizations, similar to FFELP securitizations, generally have a senior-subordinate structure with both time tranches and credit tranches, although the subordinate tranches are significantly larger for private student loan securitizations. These securitizations are almost exclusively issued out of a discrete trust, although some nonprofit securitizers co-mingled a small number of private loans with the FFELP loansin their revolving master trusts. Since the financial crisis, private student loan securitizations, like FFELP securitizations, have reduced the number and the maturity of the tranches, and have achieved this reduction by dramatically increasing the overcollateralization of the securities.

Collateralized Loan Obligations

CLOs involve the securitization of senior secured corporate loans that are typically made to non-investment-grade borrowers. CLOs can be divided into two subcategories: broadly syndicated CLOs and middle-market CLOs. Broadly syndicated CLOs are collateralized by syndicated loans to large borrowers. These loans may be purchased in the primary or secondary market. Consistent with the underlying loans being syndicated, a CLO typically owns a partial interest in a particular loan, while the remainder of the loan is held by other investors, including banks, institutional investors, and other CLOs. Middle-market CLOs are collateralized by loans to relatively smaller borrowers and tend to be securitized by the originator of the loans (for example, a finance company).

A CLO securitization typically begins with the manager engaging an investment bank to provide a warehouse facility to acquire and hold collateral until the acquisition of the portfolio of loans is complete. Collateral selection is primarily the job of the CLO manager. Most CLO managers are not affiliated with commercial or investment banks that arrange syndicate loans, but there are exceptions. For example, a CLO could be managed by the asset management affiliate of a large bank holding company.

CLOs differ from most other securitization vehicles backed by term loans in that the portfolio of loans is actively managed by the CLO manager. Even after the CLO closing, the CLO manager continues to make investment decisions over a specified reinvestment period during which proceeds from sold, maturing, or refinanced loans are reinvested. In most deals, the manager turns over a limited portion of the collateral, generally around 20 percent, each year. To protect investors' interests, the manager's ability to alter the composition of the portfolio is restricted and could be eliminated if the CLO fails to meet certain performance tests.

Prior to the crisis, a typical CLO securitized $400 million to $600 million of loans, utilizing multiple debt tranches ranging from AAA down to mezzanine as well as an equity tranche. Cash flows were allocated sequentially according to the waterfall specified in the CLO indenture. The typical contractual maturity of deals was 12 to 15 years, with the reinvestment period spanning the first 5 to 7 years.

Most recently, there have been few CLO securitizations and those that have been issued are smaller, ranging from $300 million to $400 million in loans. These deals have had a much simpler structure with fewer debt tranches and a relatively larger equity tranche, leading to lower leverage and more subordination to cushion losses for debt holders. Legal maturities of deals are now often below 10 years and reinvestment periods have been shortened to as low as 2 years.

Equipment Loans and Leases

Equipment loans and leases are extended to businesses to facilitate the purchase or lease of business, industrial, and farm equipment, including "large ticket" items such as bulldozers and backhoes and "small ticket" items such as computers and copiers. The businesses that take out these loans tend to be smaller firms. The underlying loans and leases are generally fixed-rate loans with relatively short maturities, similar to auto loans.

Loans and leases for large-ticket items are usually extended by "captive" finance companies affiliated with the equipment manufacturers, whereas loans and leases for small-ticket items are extended by specialty (or "independent") finance companies. These specialty finance companies may have relationships with multiple equipment vendors. Leases of aircraft, railcars, and container leases are also routinely securitized, but these securitizations are not usually considered "equipment" ABS.

As in auto ABS, the originator, securitizer, and servicer of an equipment loan or lease ABS are usually affiliated with the same parent entity. Likewise, the structure tends to be a discrete trust with senior and subordinate tranches that pay sequentially. There are usually a few triple-A tranches with different maturities, with the shortest tranche typically having an average life of around three months and the remaining tranches having average lives ranging from one to three years. The structure generally includes multiple subordinate tranches and the securitizer often retains the residual interest in the deal, and sometimes the subordinate tranches as well.

Dealer Floorplan Loans

Dealer floorplan financing is a revolving line of credit that allows merchandise dealers to finance their inventory. The dealer repays the debt as the inventory is sold and can borrow against the line of credit to add new inventory. Auto and non-auto floorplan are considered separate ABS categories. Auto floorplan includes floorplan loans to finance car, light truck, and motorcycle inventory. Non-auto floorplan loans finance other types of dealer inventory, including agricultural, construction, manufacturing, and electronic equipment, as well as appliances.

Auto floorplan loans typically are originated by captive finance companies affiliated with large auto manufacturers, although depository institutions also originate these loans. Non-auto floorplan lines of credit are originated by captive finance companies affiliated with large equipment manufacturers as well as by independent finance companies.

As with credit card receivables, the underlying floorplan receivables have very short lives, generally about 45 to 75 days. This short life corresponds to the average length of time that a vehicle, piece of equipment, or appliance is in the dealer's inventory before it is sold. Because of this short life, floorplan ABS, like credit card ABS, are issued out of master trusts. The structure is very similar to the credit card ABS structure in that there is the "investor's interest" and the "seller's interest," as described in above of this report.

Asset-Backed Commercial Paper

ABCP is an important source of short-term financing for a variety of underlying loan types. ABCP is a type of liability that is typically issued by a special purpose vehicle (or conduit) sponsored by a financial institution or other securitizer. The commercial paper issued by the conduit is collateralized by the pool of assets, which may change over the lifespan of the SPV. Like other types of commercial paper, the tenor of ABCP is typically short, and the liabilities are "rolled," or refinanced, at regular intervals. Thus, ABCP financed structures generally engage in some degree of maturity transformation, funding longer-term assets with shorter-term liabilities. ABCP is backed by a wide range of assets including auto loans, commercial loans, trade receivables, credit card receivables, student loans, and highly rated securities. Money market mutual funds are the main investors in the ABCP market.

Securitizers of ABCP conduits generally are large U.S. and foreign banks, although mortgage lenders, finance companies, and asset managers have also been active to some extent. The assets may be originated by the bank securitizer (for example, credit card receivables), or the securitizer may aggregate assets from various originators for securitization (for example, trade receivables from various clients of the bank). Securitizers may provide liquidity and credit support to the ABCP conduit, either directly if it is a financial institution or by obtaining lines from other entities.

ABCP can be classified according to the type of support provided by the securitizer or by the types of assets purchased by the SPV. In terms of the type of support, ABCP can either be fully or partially supported. Fully supported programs use an external support facility that provides ABCP investors 100 percent insurance against credit and liquidity risk. Liquidity risk refers to the possibility that funding cannot be rolled. By contrast, partially supported programs provide less than 100 percent insurance against credit and liquidity risk to ABCP investors. These programs use credit enhancements to reduce credit risk on the assets securitized, an outside facility that insures against liquidity risk, or both.

ABCP conduit programs are typically classified as multisellers, single sellers, securities arbitrage programs, structured investment vehicles (SIVs), or hybrid programs. ABCP conduits that mainly purchase receivables and loans from multiple originators (typically clients of the securitizing bank) are known as multiseller programs. Conduits that exclusively purchase receivables and loans from a single originator (typically the securitizer) are known as single-seller programs. Conduits that purchase highly rated securities and have liquidity facilities that cover 100 percent of the liabilities of the ABCP program are known as securities arbitrage programs. Conduits that purchase highly rated securities without liquidity facilities covering 100 percent of the liabilities of the program are known as SIVs; to compensate for incomplete liquidity support, SIVs typically finance securities that may be relatively easily liquidated and issue a combination of (1) debt with longer maturities than commercial paper and (2) subordinated notes that absorb any first losses incurred by the program. Finally, conduits that combine characteristics of multiseller programs with securities arbitrage programs are known as hybrids.

Issuance Activity

This section examines the issuance volume of different ABS classes over time and documents the proportion of issuance occurring in the private placement (or Rule 144A) markets. Private placements are of interest because this method of issuance has less stringent disclosure requirements than a public offering and generally offers less secondary-market liquidity than securities sold through public offerings.

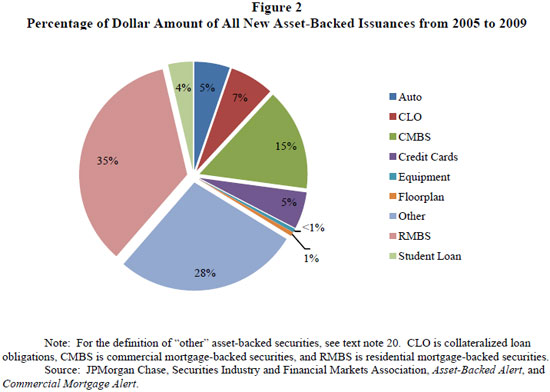

Figure 2 shows the percentage breakdown of total issuance from 2005 to 2009 for each asset class excluding ABCP.19 As shown, RMBS is the largest category, followed by "other" ABS that are not covered by this report, CMBS, CLOs, credit card ABS, and auto ABS. 20

The following subsections explore the variation in issuance among asset classes in more detail.

Real Estate Sector

The real estate sector, whose underlying collateral includes both residential and commercial mortgages, represents the largest component of asset-backed securities. Table 1 presents the dollar amount issued and the number of real estate deals from 2002 to September 2010. As indicated in the table, issuance of securitizations backed by nonconforming residential mortgages plummeted in 2008 and remains virtually nonexistent today.

Issuance of RMBS backed by nonconforming loans increased significantly in the period before the crisis because of the rapid growth in the volume of originations and the increased percentage of loans securitized. The fraction of subprime mortgages that were securitized increased from less than 50 percent in 2001 to 75 percent in 2006, while the fraction of alt-A mortgages that were securitized increased from less than 20 percent in 2001 to more than 90 percent in 2006.21

| Real Estate | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | To 9/2010 | Total |

|---|---|---|---|---|---|---|---|---|---|---|

| Prime mortgages | $213,993 | $296,617 | $329,219 | $543,064 | $569,217 | $439,458 | $24,760 | $47,875 | $38,986 | $2,503,188 |

| # of deals | 501 | 622 | 574 | 752 | 713 | 584 | 83 | 126 | 80 | 4,035 |

| Subprime mortgages | $73,923 | $99,672 | $174,692 | $181,051 | $154,041 | $202,349 | $3,853 | $207 | $844 | $890,632 |

| # of deals | 159 | 187 | 247 | 215 | 191 | 276 | 12 | 1 | 4 | 1,292 |

| RMBS Total | $287,916 | $396,288 | $503,911 | $724,115 | $723,257 | $641,808 | $28,612 | $48,082 | $39,830 | $3,393,819 |

| # of deals | 660 | 809 | 821 | 967 | 904 | 860 | 95 | 127 | 84 | 5,327 |

| CMBS | $89,900 | $107,354 | $136,986 | $245,883 | $305,714 | $319,863 | $33,583 | $38,750 | $27,297 | 1,305,329 |

| # of deals | 166 | 198 | 199 | 231 | 258 | 207 | 51 | 71 | 65 | 1,446 |

Note: Prime Mortgages, for the purposes of this chart, refer to securities backed by prime first-lien U.S. residential mortgages with weighted average credit score very close to 700 or above. Subprime Mortgages represent securities backed by primarily first-lien U.S. residential mortgages with weighted average credit score less than 700. Securities issued or insured by GSEs are not included herein. More information is available at www.abalert.com/about_abs.php#Data. Source: RMBS data are from Asset-Backed Alert; CMBS data are from Commercial Mortgage Alert.

Source: RMBS data are from Asset-Backed Alert; CMBS data are from Commercial Mortgage Alert.

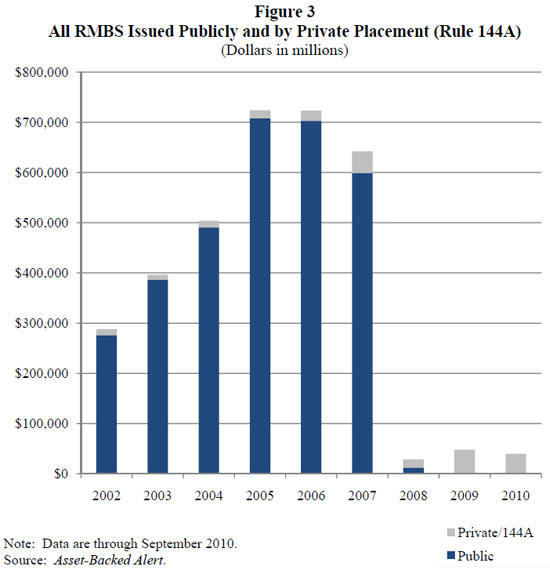

The overwhelming majority of RMBS deals issued before the crisis were public offers. Since the crisis, the few deals that have come to market (which are often backed by seasoned loans) have been issued in the private/144A market (figure 3).22

Consumer Finance

As shown in table 2, issuance in the consumer ABS market, which includes credit cards, auto loans and leases, and student loans, declined dramatically in both number of deals and dollar value after 2007. Unlike the real estate sector, however, consumer ABS has rebounded somewhat since the 2008 market trough.

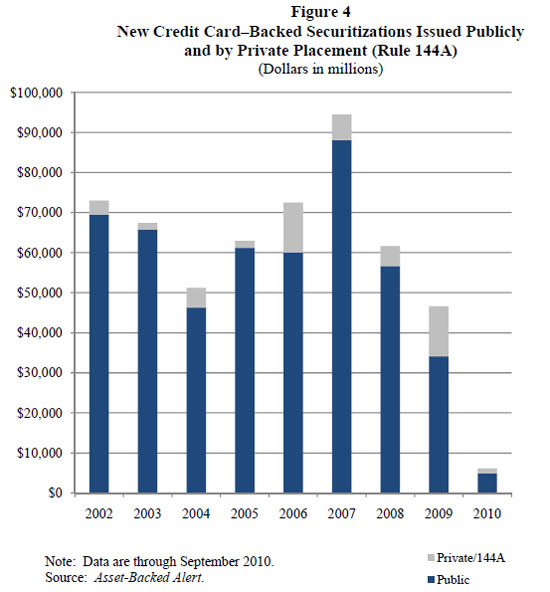

Credit card issuance came to a near-halt during the strained market conditions at the end of 2008, and then resumed in spring 2009. However, issuance has remained lackluster because of the sharp contraction in revolving credit outstanding. Due to weak consumer demand, reduced credit supply on the part of lenders, and elevated levels of charge-offs, revolving credit fell nearly 10 percent in 2009.23 In addition, the advent of the FAS 166/167 accounting standards, described in this report in the section "Interaction of Risk Retention and Accounting Standards," has required securitizers to hold almost all credit card deals on balance sheet. This switch makes securitization a less desirable form of funding, especially since most credit card securitizers are depository institutions, many of which currently enjoy ample access to other sources of funding. As shown in figure 4, private/144A deals are also more common in the period after the crisis.

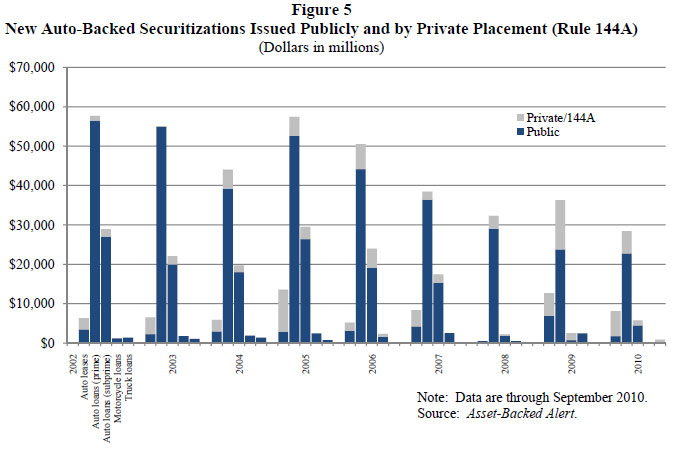

| Consumer Finance | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | To 9/2010 | Total |

|---|---|---|---|---|---|---|---|---|---|---|

| Credit cards | $73,004 | $67,385 | $51,188 | $62,916 | $72,518 | $94,470 | $61,628 | $46,581 | $6,149 | $535,839 |

| # of deals | 113 | 108 | 82 | 107 | 120 | 137 | 78 | 51 | 17 | 813 |

| Auto leases | $6,339 | $6,524 | $5,870 | 13,600 | $5,181 | $8,333 | $475 | $12,702 | $8,079 | $67,103 |

| # of deals | 10 | 12 | 7 | 13 | 6 | 9 | 1 | 13 | 12 | 83 |

| Auto loans (prime) | $57,660 | $54,994 | $44,053 | 57,423 | $50,506 | $38,462 | $32,301 | $36,301 | $28,397 | $400,097 |

| # of deals | 40 | 39 | 36 | 43 | 39 | 36 | 31 | 30 | 38 | 332 |

| Auto loans (subprime) | $28,949 | $22,033 | $19,732 | 29,467 | $23,984 | $17,446 | $2,207 | $2,518 | $5,747 | $152,084 |

| # of deals | 47 | 42 | 34 | 42 | 29 | 24 | 5 | 5 | 12 | 240 |

| Motorcycle loans | $1,186 | $1,750 | $1,876 | 2,480 | $2,330 | $2,532 | $486 | $2,423 | $0 | $15,063 |

| # of deals | 2 | 4 | 3 | 4 | 3 | 3 | 1 | 4 | 0 | 24 |

| Truck loans | $1,350 | $1,050 | $1,350 | $746 | $0 | $0 | $0 | $0 | $881 | $5,377 |

| # of deals | 2 | 2 | 2 | 1 | 0 | 0 | 0 | 0 | 1 | 8 |

| Auto Total | $95,484 | $86,350 | $72,881 | 103717 | $82,000 | $66,773 | $35,469 | $53,944 | $43,104 | $639,724 |

| # of deals | 101 | 99 | 82 | 103 | 77 | 72 | 38 | 52 | 63 | 687 |

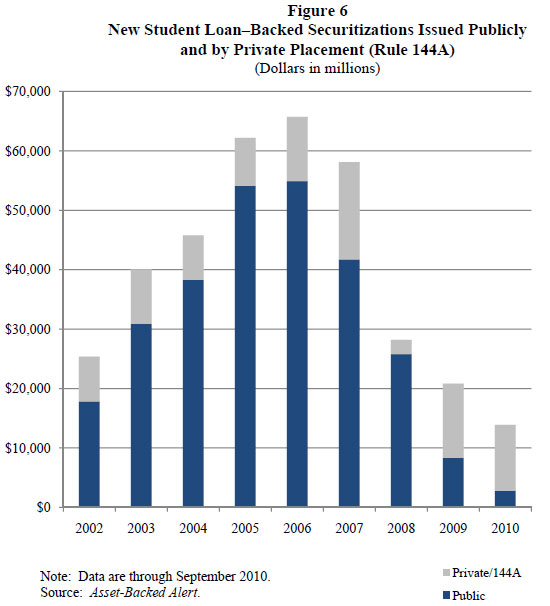

| Student loans | $25,367 | $40,067 | $45,759 | $62,212 | $65,745 | $58,122 | $28,199 | $20,839 | $13,899 | $360,210 |

| # of deals | 35 | 47 | 39 | 52 | 45 | 41 | 21 | 19 | 22 | 321 |

Source: Asset-Backed Alert.

Securitizations of auto loans and leases, like those of credit cards, dropped dramatically at the end of 2008. Unlike credit card ABS issuance, though, auto ABS issuance returned in 2009 to levels broadly comparable with 2007 issuance. The stronger rebound in the auto ABS category occurred because, among other things, auto lending did not contract nearly as sharply as credit card lending during the economic downturn. As with other consumer securitizations, auto ABS are more commonly issued in the private market following the crisis (figure 5).

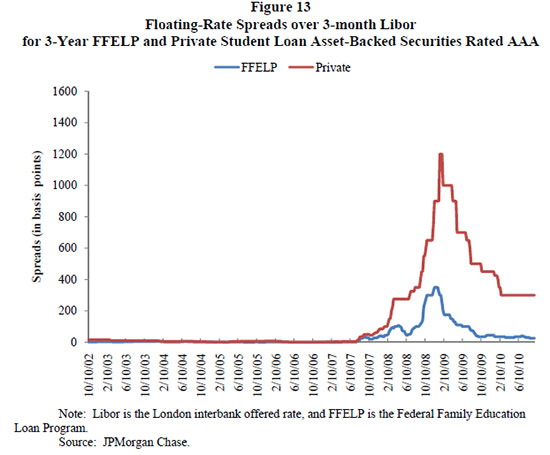

Issuance of student loan ABS dropped off in 2008, in line with other consumer sectors, and has not recovered. Securitizations of government-guaranteed loans have dropped dramatically because funding is offered on more desirable terms by special Department of Education liquidity programs put in place during the financial crisis. In addition, some securitizers continue to have difficulty accessing the capital markets because of problems associated with auction rate securities (ARS) issued prior to the crisis. Going forward, issuance is expected to remain low because government-guaranteed loans will be offered solely by the Federal government, which does not fund these loans via securitization. Further, securitizers of private student loans have had difficulty raising capital to fund these assets because of the long maturity of the loans and the recent rise in loan delinquencies.

In the post-crisis period, student loan ABS are among the most heavily reliant on the private markets for issuance, with almost all of the securitizations currently being conducted via the private/144A market (figure 6).

Business Finance

For CLOs, there has been little resurgence in issuance volume since 2008, consistent with the low volume of U.S. syndicated loan issuance relative to pre-crisis levels.24 Historically, CLOs accounted for roughly 60 percent of the investment in leveraged term loans between 2000 and 2006.25 CLOs invested in nearly $300 billion of corporate loans and today hold almost half of all outstanding non-investment-grade term loans. In 2009, new CLO issuance was only $2 billion, compared with $138 billion in 2007 (table 3). While few CLOs have been issued in 2010 most are smaller deals narrowly focused on specific collateral and investors.

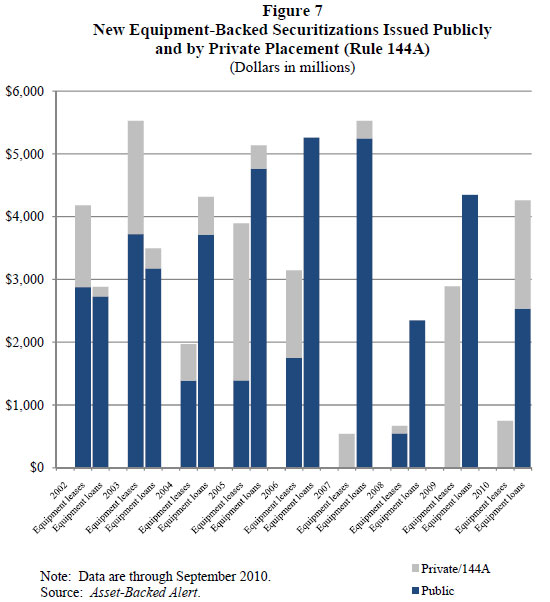

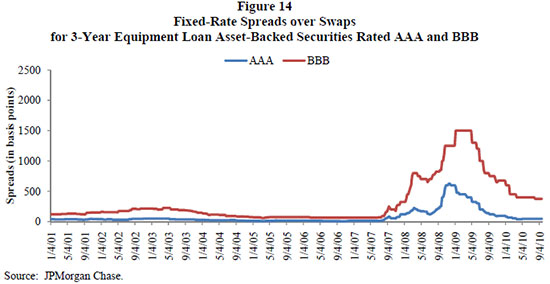

Equipment loan and lease ABS issuance has recovered almost fully since the crisis (table 3), and more of these deals now appear to be issued in the private market (figure 7). Captive finance companies of equipment manufacturers represented at least 75 percent of annual issuance in each of the past five years.

| Business Finance | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | To 9/2010 | Total |

|---|---|---|---|---|---|---|---|---|---|---|

| CLO | $30,388 | $22,584 | $32,192 | $69,441 | $171,906 | $138,827 | $27,489 | $2,033 | NA | $494,860 |

| Equipment leases | $4,180 | $5,528 | $1,971 | $3,893 | $3,144 | $540 | $665 | $2,892 | $748 | $23,561 |

| # of deals | 18 | 14 | 5 | 8 | 7 | 2 | 2 | 4 | 2 | 62 |

| Equipment loans | $2,882 | $3,493 | $4,318 | $5,137 | $5,260 | $5,526 | $2,349 | $4,348 | $4,262 | $37,576 |

| # of deals | 4 | 5 | 6 | 6 | 5 | 8 | 4 | 7 | 8 | 53 |

| Equipment Total | $7,062 | $9,022 | $6,288 | $9,030 | $8,404 | $6,066 | $3,014 | $7,240 | $5,010 | $61,137 |

| # of deals | 22 | 19 | 11 | 14 | 12 | 10 | 6 | 11 | 10 | 115 |

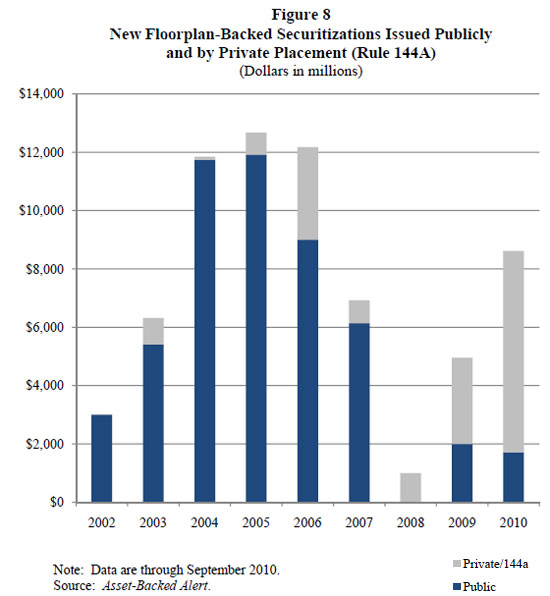

| Floorplan loans | $3,000 | $6,315 | $11,848 | $12,670 | $12,173 | $6,925 | $1,000 | $4,959 | $8,619 | $67,510 |

| # of deals | 2 | 11 | 10 | 11 | 13 | 8 | 1 | 9 | 12 | 77 |

| ABCP | NA | $8,633,591 | $7,746,457 | $9,300,331 | $12,811,588 | $17,546,734 | $16,183,104 | $8,474,867 | NA | $80,696,672 |

| # of deals | NA | 412,712 | 362,711 | 414,032 | 531,447 | 614,039 | 485,249 | 270,301 | NA | 3,090,491 |

Source: CLO data are from Securities Industry and Financial Markets Association; equipment and floorplan data are from Asset-Backed Alert; ABCP data are from Depository Trust and Clearing Corporation.

Dealer floorplan ABS had the largest decline in issuance in 2008 of any of the nine asset classes reviewed in this report outside of the real estate sector (table 3). In 2008, there was virtually no issuance of floorplan securitizations. Since that time, however, issuance has reverted to levels more comparable with the pre-crisis period. As with other asset classes, figure 8 indicates that there has been a movement away from the public market toward the private market for issuance.

Asset-Backed Commerical Paper

Issuance in the ABCP market has contracted significantly since reaching its peak in August 2007 (table 3).26 Total ABCP outstanding peaked at $1.2 trillion, representing 55 percent of the commercial paper market. Several programs faced liquidity challenges in 2007 and were unable to secure funding in the market. A number of subsequent changes to regulatory capital requirements, following the implementation of FAS 167 which brought some of these assets onto the securitizer's balance sheet, may have increased the cost of those facilities. As such, the amount of ABCP outstanding rapidly declined. Issuance in 2009 was $8 trillion, down from $17 trillion in 2007.

Mechanisms to Align Incentives and Mitigate Risk

Participants in securitization markets--originators, securitizers, rating agencies, and investors--have come to recognize that investors may have less information than other members of the securitization chain, particularly about the credit quality of the underlying assets. Furthermore, in some cases, the interests of some participants in the securitization may not be aligned with the interests of investors.

Over time, a series of mechanisms has developed to mitigate these incentive and information problems. All mechanisms share to a certain extent two features: They increase overall the odds that an investor is repaid, and they put at least one member of the securitization chain at risk of loss should the assets perform worse than expected. This latter feature is often referred to as "skin in the game."

The precise form of these mechanisms is influenced by the nature of the incentive or information problem, and by the historical development of each asset class. Mechanisms can differ across asset classes, in part because of the varying nature of the incentive problems and the differences in securitization structures and practices across asset classes.

In some cases, the mechanism applies only to the originator, while in others it applies only to the securitizer. The point in the chain where the mechanism acts is determined by the nature of the incentive or information problem. For example, the originator is likely to face some kind of incentive alignment mechanism, such as representations and warranties (R&W), if so-called soft information (known only to the originator) is crucial to loan performance.

During the financial crisis, some of these mechanisms failed to properly align incentives or to protect investors. Specific mechanisms, while effective in principle, may have failed in practice because they were too weak to overcome the incentive or information problems in a particular asset class.

Common mechanisms include overcollateralization, subordination, third-party credit enhancement, R&W, conditional cash flows, and retention of credit risk. Some of these mechanisms may lead the securitizer or the originator to retain part of the credit risk of a securitization. Each mechanism is described as follows:

- To implement overcollateralization the securitizer backs a deal with collateral that has a par value greater than the value of the liabilities sold to investors. For example, a deal with outstanding liabilities having a face value of $100 might be backed by loans with a combined principal of $110. In the event of default, the overcollateralization is available to support contractual payments to investors. In the event of no default, the overcollateralization may be returned to the securitizer.

- Subordination is related to overcollateralization. The securitizer structures the securitization so that the senior liabilities take losses only if the junior liabilities providing credit support have been completely exhausted by losses; the greater the amount of the credit support below the senior liabilities, the greater the subordination. The most junior liability in a structure is sometimes referred to as the equity piece. Having the originator or the securitizer retain the equity piece may act as an incentive alignment mechanism, because the party retaining the equity piece bears the first loss risk on the underlying assets.

- Third-party guarantees, or wraps, are insurance usually written on the seniormost tranche of a securitization. In theory, the insurers providing wraps for asset-backed securities had an incentive, through their exposure to default losses, to monitor the quality of loans backing the securities. It appears, however, that during the height of asset-backed issuance, some of these insurers did not perform adequate due diligence, suffering large losses as a result.

- Representations and warranties are factual statements that describe the underwriting standards and other matters with respect to the assets that are the subject of the securitization. R&W may not have begun as incentive alignment or credit enhancement mechanisms. However, the originator is, in principle, required to refund at par the value of the loan should it violate the originator's R&W about its features or should it default within a specified time from origination. During the crisis, some originators failed to repurchase loans that violated R&W.

- Conditional cash flows are provisions in securities that release cash from the pool to junior securities or the originator based on the deal's performance. Should delinquency rates fall below predefined trigger levels, for example, cash reserves trapped in the trust, either supplied in advance by the securitizer or created by accumulating excess spread, would be remitted back to the securitizer.27 These conditional cash flows serve the purpose of providing extra credit support to the senior tranche holders should the underlying loans perform worse than expected. They also should, in principle, give the originator and the securitizer the incentive to deliver lower-risk loans to the pool, in hopes of meeting the triggers and, thereby, receiving the conditional cash flows themselves. The conditions under which cash is released can be quite complex, with some securities applying a series of tests at a single point in time and others applying tests each month. Examples of conditional cash flows include releases from cash reserve accounts, shifting interest structure, and early amortization.

- Retention of credit risk is another key incentive alignment mechanism. Retention, in principle, gives securitizers or originators an explicit pecuniary stake in the performance of their assets. In addition to its incentive benefits, retention has the virtues of being observable by outside parties. The securitizer or originator may retain credit risk by holding some portion of the securities issued to investors. For example, if a securitizer or originator retains a piece of each tranche of securities sold to investors (a vertical slice), the securitizer or originator will retain exposure to the varying degrees of credit risk of the tranche holders. Likewise, an originator or securitizer can retain credit risk by retaining a portion of the subordinate piece of the security (a horizontal slice). Credit risk is concentrated in this security, so retaining even a small part of the subordinate piece exposes the seller to a relatively larger share of the deal's total credit risk.