January 08, 2011

The Federal Reserve's Asset Purchase Program

Vice Chair Janet L. Yellen

At the The Brimmer Policy Forum, Allied Social Science Associations Annual Meeting, Denver, Colorado

I am delighted to participate in this Brimmer Policy Forum, not least because this year marks the 45th anniversary of Andrew's appointment by President Johnson as a Governor of the Federal Reserve Board. Andrew's ongoing work in organizing this annual forum reflects his long-standing commitment to fostering economic analysis and public discourse on key policy issues.

In my remarks today, I will discuss the rationale for the decision by the Federal Open Market Committee (FOMC) in November to initiate a new program of asset purchases, and I will address some frequently asked questions (FAQs) regarding the program's economic and financial effects both here and abroad.1 The purpose of the new asset purchase program, like all of the monetary policy actions taken by the FOMC since the onset of the global financial crisis, is to fulfill our congressionally mandated objectives of promoting maximum employment and price stability. In pursuit of these goals, the FOMC brought the target federal funds rate down close to zero by late 2008; conducted large-scale purchases of longer-term securities during 2009 and early 2010; and, last summer, modified its reinvestment policy to keep the Federal Reserve's balance sheet from shrinking as mortgage-related securities matured or were redeemed. In early November, the Committee announced that it intends to purchase an additional $600 billion in longer-term Treasury securities by the middle of this year.

The Rationale for the Asset Purchase Program

Macroeconomic Conditions

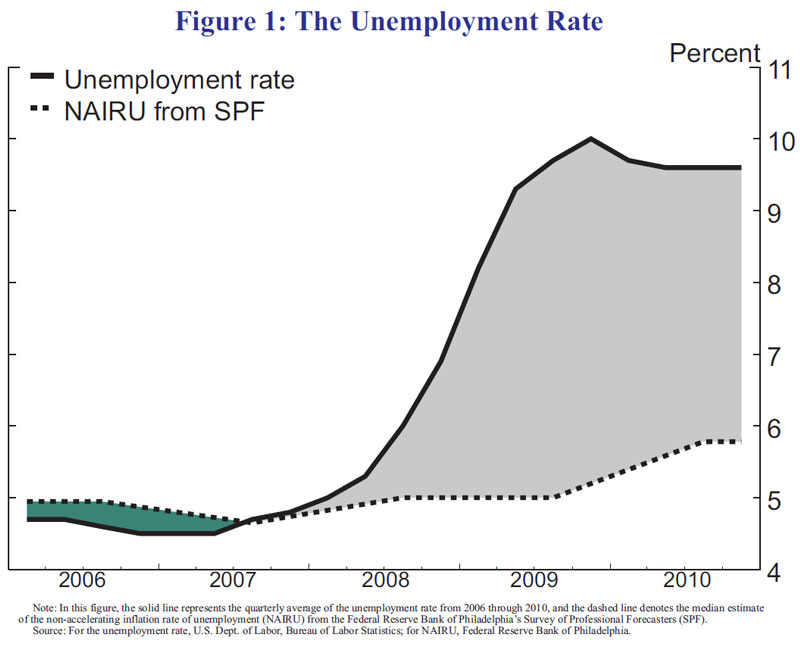

To understand the rationale for our asset purchase program, it is helpful to review the evolution of macroeconomic conditions over the past several years. The National Bureau of Economic Research has dated the recession as having begun in December 2007, but the pace of economic contraction accelerated in the wake of the Lehman Brothers collapse in September 2008 and the ensuing disruption to global financial markets. As shown in figure 1, the unemployment rate rose from around 5 percent in the spring of 2008 to about 10 percent by the autumn of 2009 and has stayed well above 9 percent since then. Most observers, including myself, judge this level of unemployment to be much higher than levels consistent with full employment and stable inflation. For example, in a recent Survey of Professional Forecasters conducted by the Federal Reserve Bank of Philadelphia, the median estimate of the current level of structural unemployment--often referred to as the non-accelerating inflation rate of unemployment (NAIRU)--stood at about 5-3/4 percent, implying that the unemployment gap is nearly 4 percentage points.

{kind=link}

In addition, a historically large fraction of the unemployed have been out of a job for a very long time. For example, roughly 4 percentage points of today's unemployment rate reflects individuals who have been unemployed for half a year or more. Those who experience an extended period of unemployment face a risk of losing their ability to participate successfully in the workforce, lending additional urgency to the task of reviving the demand for labor.

Such low rates of resource utilization are typically accompanied by falling inflation. And, indeed, as shown in figure 2, measures of inflation for personal consumption expenditures (PCE) have declined significantly since 2008. For the total PCE inflation rate, the underlying trend is obscured to some extent by large swings in energy prices. However, the downward trend is clearly evident from the evolution of core PCE inflation, which excludes the volatile prices of food and energy. The 12-month change in core PCE prices dropped from about 2-1/2 percent in mid-2008 to around 1‑1/2 percent in 2009 and declined further to less than 1 percent by late 2010.2

{kind=link}

As inflation has trended downward, measures of underlying inflation have fallen somewhat below the levels of about 2 percent or a bit less that most Committee participants judge to be consistent, over the longer run, with the FOMC's dual mandate. In particular, a modest positive rate of inflation over time allows for a slightly higher average level of nominal interest rates, thereby creating more scope for the FOMC to respond to adverse shocks. A modest positive inflation rate also reduces the risk that such shocks could result in deflation, which can be associated with poor macroeconomic performance.

Of course, if incoming information last autumn had been pointing to greater momentum in the prospects for economic growth or to a rapid escalation in inflation, then the case for further monetary policy easing might have seemed less pressing. However, such was not the case. The Federal Reserve publishes a Summary of Economic Projections (SEP) four times a year in conjunction with the FOMC minutes. As shown in the November SEP, most Committee participants anticipated that the economy would recover only gradually and projected that the unemployment rate would still be at around 8 percent at the end of 2012--an outlook that is shared by most outside forecasters. Similarly, Committee participants generally expected inflation to rise very gradually toward levels consistent with the Federal Reserve's mandate. Moreover, continuing downside risks to the outlook for economic activity and inflation strengthened the case for providing additional monetary policy accommodation, thereby reducing the risk of another downturn in economic activity or a further decline in inflation.

The Design of the Asset Purchase Program

In weighing its policy options last autumn, the Committee gave careful consideration to the question of whether further purchases of longer-term Treasury securities were likely to be effective in fostering economic recovery and bringing inflation back up to levels judged to be consistent with the dual mandate.3 In my judgment, both theoretical analysis and empirical evidence suggested that such purchases could provide effective stimulus by keeping longer-term interest rates lower than they would otherwise be.

The underlying theory, in which asset prices are directly linked to the outstanding quantity of assets, dates back to the early 1950s.4 For example, in preferred-habitat models, short- and long-term assets are imperfect substitutes in investors' portfolios, and the effect of arbitrageurs is limited by their risk aversion or by market frictions such as capital constraints. Consequently, the term structure of interest rates can be influenced by exogenous shocks in supply and demand at specific maturities. Purchases of longer-term securities by the central bank can be viewed as a shift in supply that tends to push up the prices and drive down the yields on those securities.

In the context of such an analytical framework, the effect of an asset purchase program also depends on investors' perceptions of the future path of short-term interest rates as well as their perceptions of the timing and pace of the central bank's eventual unwinding of its asset purchases. Thus, central bank communication may play a key role in influencing the financial market response to such a program.

Recent empirical work provides a rough gauge of the quantitative effects of longer-term securities purchases.5 For example, event studies have investigated the short-term response of asset prices to announcements by the Federal Reserve and the Bank of England regarding their respective asset purchase programs. And regression analysis has been used to estimate statistical models that embed predictions from a specific theoretical framework.

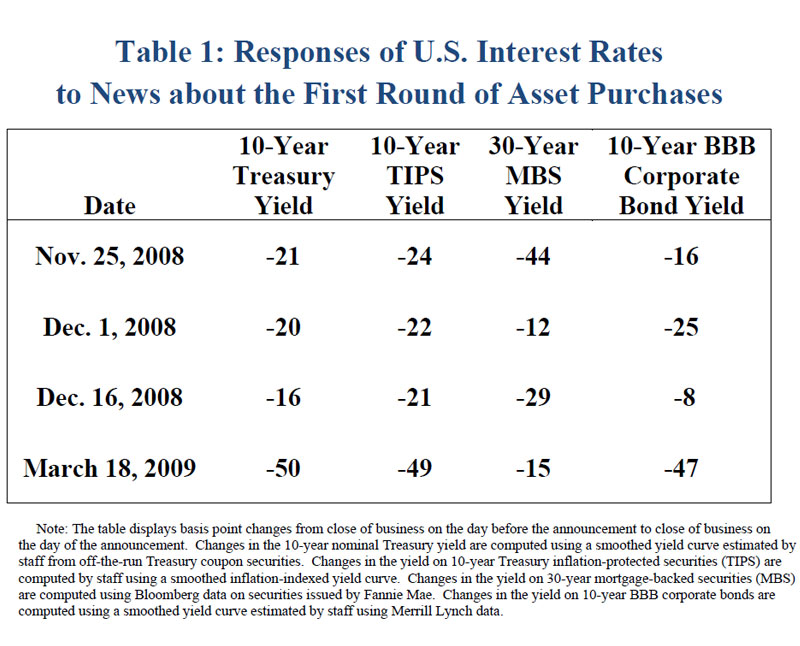

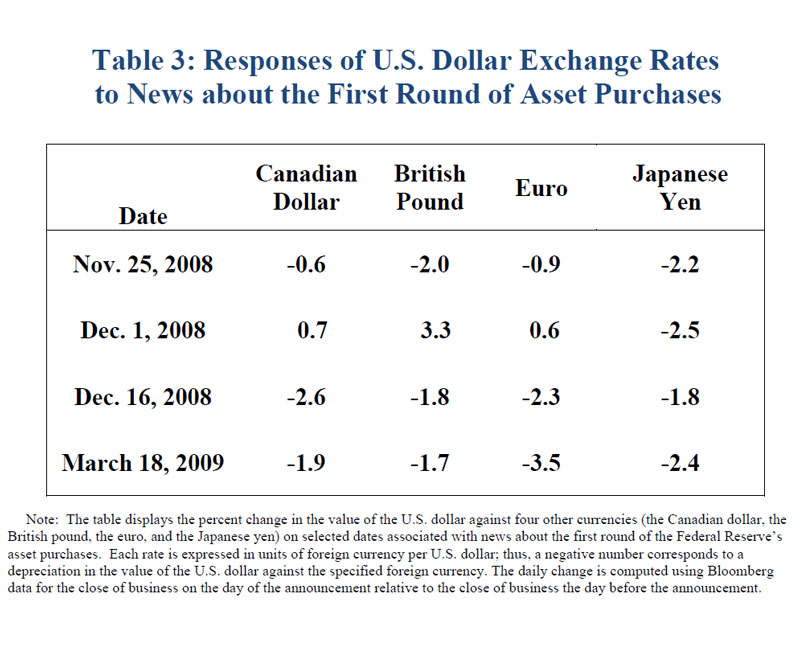

Table 1 summarizes the response of selected financial variables on four dates associated with the Federal Reserve's first round of asset purchases. On November 25, 2008, the Federal Reserve announced that it would purchase up to $600 billion in agency mortgage-backed securities (MBS) and agency debt. On December 1, Chairman Bernanke provided further details in a speech.6 On December 16, the program was formally launched by the FOMC.7 On March 18, 2009, the FOMC announced that the program would be expanded by an additional $850 billion in purchases of agency MBS and agency debt and $300 billion in purchases of Treasury securities. As is evident from the table, these announcements were generally associated with a substantial decline in the 10-year Treasury yield and the yield on 10-year Treasury inflation-protected securities (TIPS) as well as in rates on agency MBS and corporate debt.

{kind=link}

Turning now to the macroeconomic effects of the Federal Reserve's securities purchases, there are several distinct channels through which these purchases tend to influence aggregate demand, including a reduced cost of credit to consumers and businesses, a rise in asset prices that boosts household wealth and spending, and a moderate change in the foreign exchange value of the dollar that provides support to net exports. The quantitative magnitude of these effects can be gauged using a macroeconometric model such as FRB/US--one of the models developed and maintained by Board staff and used routinely in simulations of alternative economic scenarios.

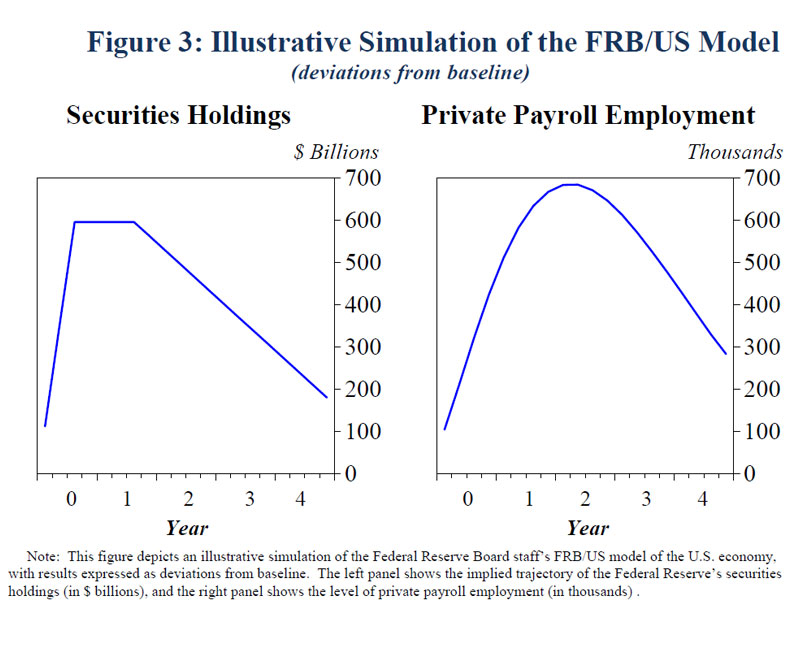

Figure 3 depicts the results of such a simulation exercise, as reported in a recent research paper by four Federal Reserve System economists.8 For illustrative purposes, the simulation imposes the assumption that the purchases of $600 billion in longer-term Treasury securities are completed within about a year, that the elevated level of securities holdings is then maintained for about two years, and that the asset position is then unwound linearly over the following five years.9

{kind=link}

This trajectory of securities holdings causes the 10-year Treasury yield to decline initially about 1/4 percentage point and then gradually return toward baseline over subsequent years. That path of longer-term Treasury yields leads to a significant pickup in real gross domestic product (GDP) growth relative to baseline and generates an increase in nonfarm payroll employment that amounts to roughly 700,000 jobs.10 It should also be noted that this exercise is performed as a deterministic simulation and hence does not capture the potential benefits of the asset purchase program in mitigating downside risks to economic activity and inflation.

I would also like to note that the same research paper analyzed the macroeconomic effects of the FOMC's full program of securities purchases, including the first round of purchases that was initiated in late 2008 and early 2009, the modification of the reinvestment policy that was announced last August, and the second round of purchases that was initiated in November. Those simulation results indicate that by 2012, the full program of securities purchases will have raised private payroll employment by about 3 million jobs. Moreover, the simulations suggest that inflation is currently a percentage point higher than would have been the case if the FOMC had never initiated a securities purchases, implying that, in the absence of such purchases, the economy would now be close to deflation.11

Addressing Some FAQs about the Asset Purchase Program

Has the Program Been Effective in Promoting the Economic Recovery?

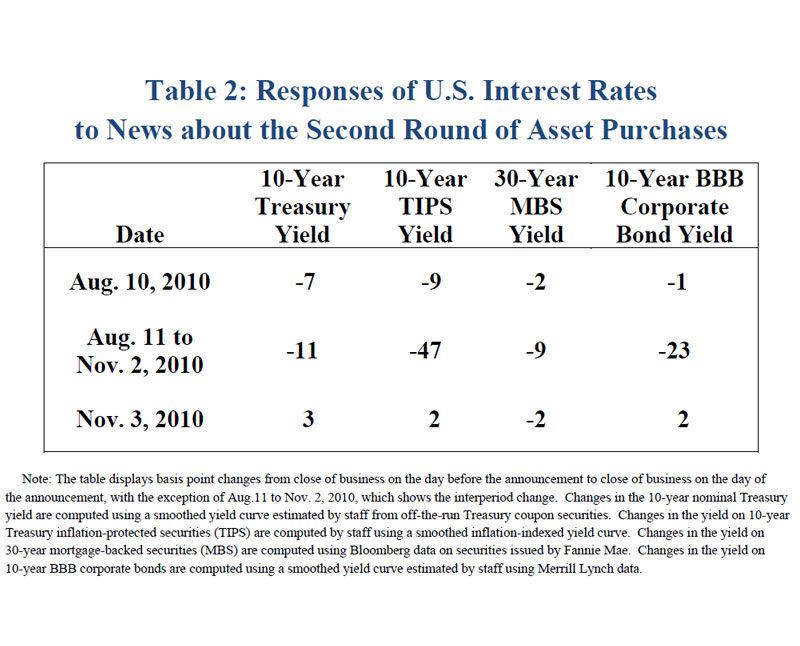

Is the program actually proving effective? My short answer is yes. Table 2 depicts financial market responses during three key phases in the rollout of the program: (1) August 10, 2010, when the FOMC announced that the Federal Reserve would begin reinvesting principal payments on agency MBS and agency debt by purchasing Treasury securities; (2) the period between August 11 and November 2; and (3) November 3, the date on which the FOMC meeting statement announced the commencement of the program.

{kind=link}

As shown in the table, the initiation of the securities purchase program at the November FOMC meeting occasioned only minimal market response. The reason is that it was largely anticipated by investors, having been the subject of extensive public discussions by Federal Reserve officials during late summer and early autumn. Importantly, as expectations of the program gradually became embedded in asset prices during late summer and early autumn, the 10-year TIPS yield dropped nearly 1/2 percentage point over the period between the August and November FOMC meetings; moreover, equity prices rose and corporate bond spreads narrowed. Over that period, of course, asset prices were also responding to economic news and some favorable corporate earnings reports, but the overall pattern of the financial market data bolstered my confidence in the effectiveness of the Federal Reserve's securities purchases in providing additional monetary policy accommodation. Indeed, market rates might well have backed up significantly following the November FOMC meeting if the Committee had decided not to move ahead with the program.12

As shown in figure 4, longer-term Treasury yields have risen substantially over the past couple of months since the FOMC initiated this round of asset purchases. I believe that this increase in Treasury yields likely reflects a number of significant factors, including incoming information suggesting a somewhat stronger economic outlook and the fiscal package that was announced by President Obama in early December and approved by the Congress about two weeks later; that package will not only support economic growth next year but will also increase the amount of federal debt issuance. Also, investors appear to have scaled back their expectations about the extent to which the FOMC will engage in further purchases beyond those already announced; however, the effect of that reassessment on market rates tends to bolster the view that the Federal Reserve's securities purchases do indeed affect yields in the direction indicated by analytical and empirical studies.13

{kind=link}

Will the Asset Purchase Program Lead to Excessive Inflation?

A concern voiced by some observers is that the asset purchase program will lead to excessive inflation. One rationale for this view is that the economy is currently operating with little slack--that is, an unemployment rate that is not far from the NAIRU. A second rationale is that asset purchases have ballooned the Fed's balance sheet and the supply of bank reserves. I will consider each argument in turn.

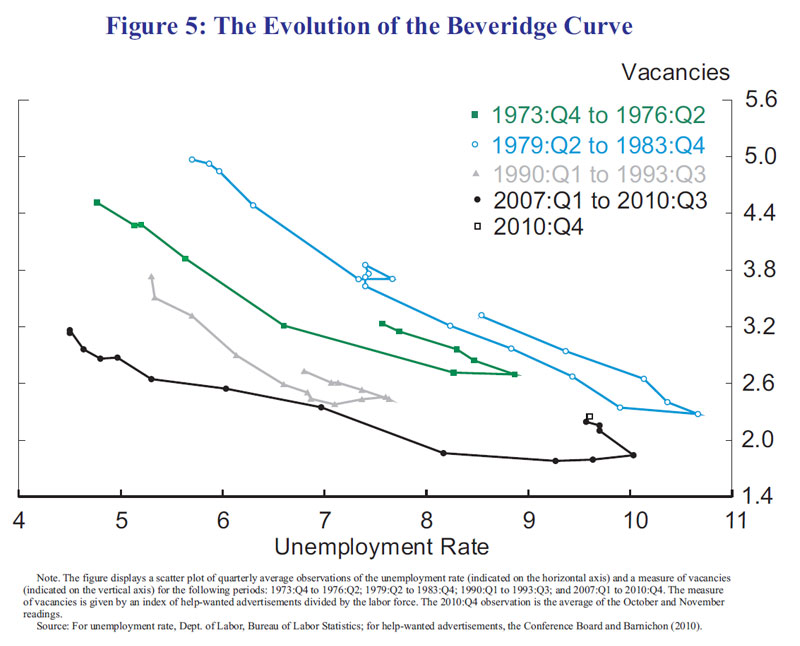

Extent of slack in the economy. Some proponents of the view that the U.S. economy is operating close to the NAIRU point to an apparent outward shift in the Beveridge curve--the relationship between job vacancies and unemployment--as indicating an increase in the structural level of unemployment. In the simplest framework, movements along a downward sloping Beveridge curve are typically characterized as cyclical movements in labor market conditions, while persistent inward and outward shifts in the curve are frequently attributed to structural forces.

As shown in figure 5, the Beveridge curve appears to have shifted out in recent years. However, the Beveridge curve can shift out for a variety of reasons, including some that are essentially cyclical in nature, so it is important to understand the sources of a shift to assess whether it represents persistent structural forces.

{kind=link}

There is some evidence suggesting that structural factors account for a portion of the Beveridge curve's outward shift. In particular, the shift may partly reflect a decline in the efficiency with which unemployed workers are matched to vacant jobs.14 However, given that the apparent decline in matching efficiency coincided with a large reduction in job vacancies, the two developments may be related. In particular, weak labor demand may be causing the labor market to operate less efficiently than would typically be the case, and matching efficiency may return to normal as demand for workers improves. Indeed, historically, matching efficiency does appear to move back toward its long-run average over time.15 That said, a persistently high level of long-term unemployment could lead to a significant increase in structural unemployment over time as individuals who are out of work for long periods face the erosion of their skills. However, such effects would take time to materialize and, in any event, would argue for aggressive policies to reduce unemployment promptly.

Another portion of the recent outward shift in the Beveridge curve is likely due to increases in the maximum duration of unemployment benefits, which may have induced some unemployed workers to be more selective in the job offers they accept. However, recent research suggests that the increase in unemployment due to extended benefits is probably small relative to the overall increase in unemployment, and, regardless of its magnitude, the influence of extended unemployment benefits will disappear as the economy improves and extended benefits expire.16

Moreover, at least some of the recent outward shift in the Beveridge curve appears to reflect cyclical rather than structural influences. For example, vacancies typically adjust more quickly than unemployment to changes in labor demand, causing counterclockwise movements in vacancy-unemployment space that can look like shifts in the Beveridge curve. Indeed, as is evident from the figure, such counterclockwise movements have occurred in most previous recessions.

Finally, it is worth emphasizing that most of the co-movement between unemployment and vacancies in recent years does not appear especially unusual. In particular, low vacancies and elevated layoffs--likely driven by weak labor demand--can account for much of the increase in unemployment that has occurred since mid-2008.17 This observation is in accord with the recent behavior of inflation, which, as noted above, has trended down over the past three years, consistent with a decline in rates of resource utilization. Likewise, nominal wage growth has fallen noticeably over the past several years and remains quite low.

In sum, while deficient labor demand may not be the only factor boosting unemployment currently, and while disentangling the various influences on unemployment is not straightforward, weak labor demand appears to be the predominant factor keeping the unemployment rate elevated. This weakness, in turn, implies that current resource utilization is likely well below normal levels, mitigating the risk that the policy stimulus from our asset purchase program will lead to excessive inflation.

Inflation and bank reserves. A second reason that some observers worry that the Fed's asset purchase programs could raise inflation is that these programs have increased the quantity of bank reserves far above pre-crisis levels. I strongly agree with one aspect of this argument--the notion that an accommodative monetary policy left in place too long can cause inflation to rise to undesirable levels. This notion would be true regardless of the level of bank reserves and pertains as well in situations in which monetary policy is unconstrained by the zero bound on interest rates. Indeed, it is one reason why the Committee stated that it will review its asset purchase program regularly in light of incoming information and adjust the program as needed to meet its objectives. We recognize that the FOMC must withdraw monetary stimulus once the recovery has taken hold and the economy is improving at a healthy pace. Importantly, the Committee remains unwaveringly committed to price stability and does not seek inflation above the level of 2 percent or a bit less than that, which most FOMC participants see as consistent with the Federal Reserve's mandate.

In contrast, I disagree with the notion that the large quantity of reserves resulting from our asset purchases poses some special barrier to removing policy stimulus when the right time comes. The FOMC will be able to increase short-term rates by raising the interest rate that we pay on excess reserves--currently 1/4 percent. That ability will allow us to manage short-term interest rates effectively and thus to tighten policy when needed, even if bank reserves remain high.

Given the very high level of reserve balances, changes in the interest rate on reserves might not be fully reflected in the federal funds rate and other short-term market rates. In that event, the Federal Reserve can use tools it has developed and tested to drain or immobilize bank reserves, thereby enhancing our control over the federal funds rate. To build the capability to drain large quantities of reserves, the Federal Reserve has expanded the range of its counterparties for reverse repurchase operations beyond the primary dealers and has developed the infrastructure necessary to use agency MBS as collateral in such transactions. The Federal Reserve has also put in place a Term Deposit Facility through which it can offer deposits to member institutions that are roughly analogous to the certificates of deposit that these institutions offer to their customers. We have tested both of these tools by conducting several small-scale operations and have the ability to initiate them quickly if needed. The use of reverse repurchase operations and the Term Deposit Facility would allow the Federal Reserve to drain hundreds of billions of dollars of reserves from the banking system should conditions necessitate. We don't think that draining such large amounts of reserves will be necessary for a smooth exit, but it makes sense to be prepared, and hence we have followed this "belt and suspenders" approach.

Finally, we can sell portions of our holdings of MBS, agency debt, and Treasury securities if we determine that doing so is an appropriate way of tightening financial conditions when the time comes. The redemption or sale of securities would have the effect of reducing the size of the Federal Reserve's balance sheet as well as further reducing the quantity of reserves in the banking system. Restoring the size and composition of the balance sheet to a more normal configuration is a longer-term objective of our policies. Any such sales would be at a gradual pace, would be clearly communicated to market participants, and would entail appropriate consideration of economic conditions.

In short, the range of tools we have developed will permit us to raise short-term interest rates and drain large volumes of reserves when it becomes necessary to achieve the policy stance that fosters our macroeconomic objectives--including the objective of maintaining price stability.

Will the Asset Purchase Program Result in Adverse Financial Imbalances?

The Committee's intention in implementing asset purchases is to hold down the level of longer-term interest rates to make credit more affordable for businesses and households. A reasonable fear is that this process could go too far, encouraging potential borrowers to employ excessive leverage to take advantage of low financing costs and leading investors to accept less compensation for bearing risks as they seek to enhance their rates of return in an environment of very low yields.

This concern deserves to be taken seriously, and the Federal Reserve is carefully monitoring financial indicators for signs of potential threats to financial stability. While there is no single metric we can use to assess these threats, standard financial market indicators do not currently signal significant excesses or imbalances in the United States. In the stock market, for example, price-to-earnings ratios, by some measures, remain below their averages over the past several decades, and other valuation measures also indicate that equity prices are not significantly out of alignment with past norms. In the real estate market, price-to-rent ratios for both residential and commercial real estate are now within a reasonable range of their long-run averages, in contrast to the severe misalignment that occurred prior to the crisis. Again, there is little sign here of imbalances relative to fundamentals, at least if history is used as a guide. In fixed-income markets, narrow risk spreads and risk premiums could be signs of excessive risk-taking by investors, and indeed spreads on corporate bonds have dropped dramatically since the financial crisis, as the economic outlook has improved and investor sentiment has picked up. Risk premiums on nonfinancial corporate bonds, as measured by forward spreads far in the future, are relatively low compared with historical norms, although other indicators for this market do not point to overvaluation.

An alternative way to identify imbalances is to focus more directly on measuring credit flows and exposures to credit risk. Extraordinarily rapid credit growth may be a sign that financial institutions are taking greater risks onto their balance sheets. In recent months, nonfinancial corporations have issued large amounts of bonds and syndicated leveraged loans, and banks' provision of consumer credit has shown some signs of reviving. Nonetheless, a portion of the recent corporate issuance has been used to refinance existing debt, including leveraged loans; small business lending remains especially weak; and commercial and residential mortgage originations continue to shrink. Thus, there is little evidence that financial institutions are significantly expanding the level of credit and liquidity provided to households and businesses on net. Indeed, given the current very low level of interest rates and the continuation of the economic recovery, credit flows remain stubbornly sluggish.

Of course, such aggregate measures provide only an imperfect picture of overall credit conditions. Another type of evidence comes from surveying market participants about their practices. For bank lending, we have the Federal Reserve's Senior Loan Officer Opinion Survey on Bank Lending Practices, which provides information about changes in supply and demand for bank loans to businesses and households. Recent surveys have indicated that banks have only just begun to reverse the historically large tightening in standards and terms that they implemented in the aftermath of the crisis. In fact, considerably more easing of terms and standards will probably be required before lending conditions return to normal.

To monitor leverage provided by dealers to financial market participants, last June the Federal Reserve launched the Senior Credit Officer Opinion Survey on Dealer Financing Terms. This survey provides information on credit terms and availability of various forms of dealer-intermediated financing, including funding for securities positions and over-the-counter derivatives. The survey results suggest that over the past several months there has been some easing of terms applicable to financing for a range of counterparty types and many types of collateral, as well as an increase in demand from clients to fund most types of securities. These results indicate that the availability and use of leverage by nonbank financial institutions increased somewhat last year. Overall, a variety of indicators suggest that leverage generally remains well below the levels reached prior to the financial crisis, but these measures are worth watching closely, and the new survey reflects our strong commitment to developing additional tools for this purpose.

The Federal Reserve is closely monitoring many indicators of financial conditions to better understand the implications of financial market developments for the economy as well as risks to the financial system itself. We are working with other regulators to make the financial system more robust and are attentive in our supervision to developments that may affect systemic risk. If evidence of financial imbalances were to develop, I believe that supervision and regulation should provide the first line of defense so that monetary policy can concentrate on its longstanding goals of price stability and maximum employment. That said, we cannot categorically rule out using monetary policy to address financial imbalances, given the damage that they can cause.

Will the Asset Purchase Program Have Adverse Effects on Foreign Economies?

My final FAQ relates to the concerns that some observers have expressed over the potential for the Federal Reserve's asset purchase program to have adverse effects on foreign economies. One specific concern is that these securities purchases might drive down the value of the U.S. dollar, thereby diverting demand from our trading partners. Although purchases of longer-term securities are a less conventional means of conducting monetary policy than the more familiar approach of managing short-term interest rates, the goals and transmission mechanisms are actually very similar, and there is nothing special about these asset purchases that would make them especially likely to weigh on the dollar.

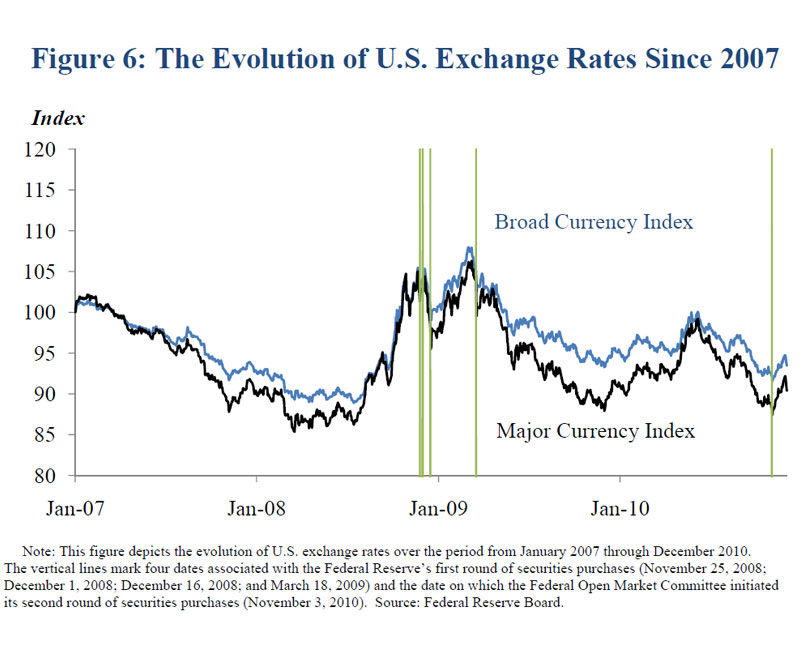

In fact, the evidence available to date suggests that the asset purchases have had only moderate effects on the foreign exchange value of the dollar. This point is illustrated in table 3, which reports the change in U.S. dollar exchange rates against four other currencies (the Canadian dollar, pound sterling, euro, and yen) on each of the four dates referred to in table 1. These movements in exchange rates are not particularly large when compared with the fluctuations that can occur in any given week or month. Indeed, as shown in figure 6, these exchange rate movements are very modest in the broader context of developments over the past several years.

{kind=link}

{kind=link}

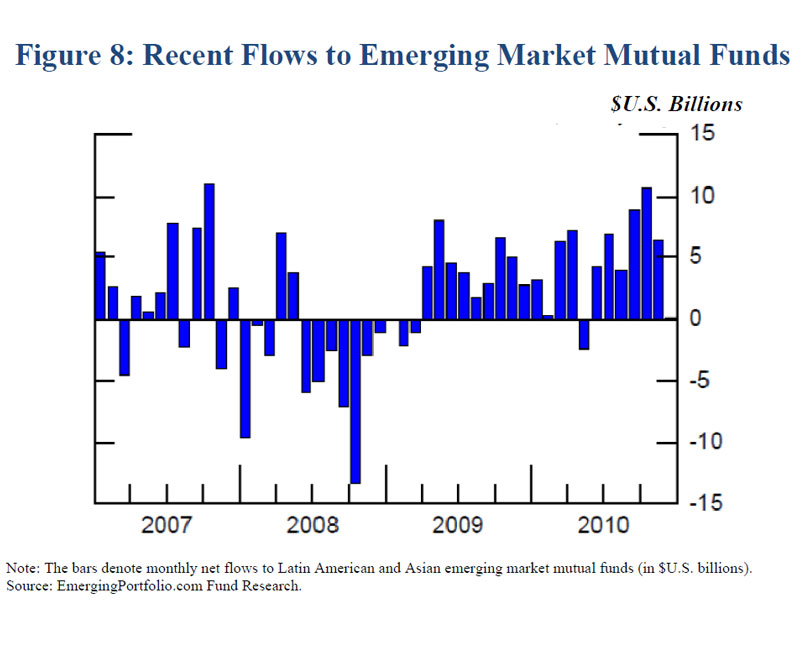

A related concern raised by some observers is that the Federal Reserve's asset purchases may induce excessive capital inflows to emerging market economies (EMEs)--inflows that in turn could put unwelcome upward pressure on the currencies of those EMEs and perhaps even contribute to asset price bubbles. As shown in figure 7, net private capital flows to Latin American and Asian EMEs (reported as a share of the aggregate GDP of those EMEs) were substantial in the second half of 2009 and the first half of 2010 but were not obviously outsized compared with levels prior to the crisis.18 A similar pattern is evident in figure 8, which depicts the net inflows since 2007 into mutual funds investing in EME bonds and equities. In each case, the strong inflows over the past year or so reflect a recovery in the wake of the large outflows that occurred during the crisis. In fact, the stock of claims on EMEs has only returned to its pre-crisis trend.

{kind=link}

{kind=link}

Accommodative monetary policies in the advanced economies, including the Federal Reserve's asset purchases, have likely played some role in widening interest rate differentials and encouraging capital flows to EMEs. But this role should not be exaggerated. Other factors--including a reversal of the capital outflows from EMEs during the financial crisis and the EMEs' longer-term favorable growth prospects--likely have also been important. Moreover, it would be a mistake to portray these capital flows as an unmitigated negative for the EMEs. A rebalanced global economy in which EMEs depend more on domestic demand for their growth will likely involve ultimately stronger and more sustained capital flows to these economies.

Finally, I would like to comment on the critique that our asset purchase program is meant to promote U.S. growth at the expense of other nations by depreciating the dollar and enhancing U.S. competitiveness. That argument ignores the fact that stimulating growth in the United States is also likely to boost our demand for foreign goods and promote growth abroad. This effect will provide an important offset to the other implication of U.S. monetary stimulus that I discussed earlier--that it may lead to moderate movements in the foreign exchange value of the dollar that tend to lower U.S. demand for foreign goods. Whether foreign demand is ultimately boosted or diminished by U.S. monetary policy depends on the relative sizes of these two effects and is ultimately an empirical question.19 However, given the moderate exchange rate effects that we believe the Federal Reserve's asset purchases have had, it seems likely to me that, as seems to be the case with conventional monetary easing achieved by lowering interest rates, our decision to purchase assets will not hinder foreign growth. In particular, given the importance of the United States in the global economy, it is hard to believe that any foreign country would gain if our economy were to fall back into another recession. Over the longer term, the health and vitality of the global economy will depend importantly on the sustained, vigorous recovery in the United States that our asset purchase program is intended to support.

Conclusion

In closing, let me reiterate that the program of asset purchases initiated by the Federal Open Market Committee in November is intended to support economic recovery from an exceptionally deep recession and to restore inflation to, but not above, levels that FOMC participants consider consistent with price stability. It will not be a panacea, but

I believe it will be effective in fostering maximum employment and price stability.

References

Barnichon, Regis, and Andrew Figura (2010). "What Drives Movements in the Unemployment Rate? A Decomposition of the Beveridge Curve (399 KB PDF)," Finance and Economics Discussion Series 2010-148. Washington: Board of Governors of the Federal Reserve System, September.

Canova, Fabio (2005). "The Transmission of U.S. Shocks to Latin America ," Journal of Applied Econometrics, vol. 20 (2), pp. 229-51.

Chung, Hess, Jean-Philippe Laforte, David Reifschneider, and John C. Williams (2011). "Have We Underestimated the Probability of Hitting the Zero Lower Bound? (568 KB PDF) " Working Paper 2011-01. San Francisco: Federal Reserve Bank of San Francisco, January.

Culbertson, John M. (1957). "The Term Structure of Interest Rates," Quarterly Journal of Economics, vol. 71 (November), pp. 485-517.

D'Amico, Stefania, and Thomas B. King (2010). "Flow and Stock Effects of Large-Scale Treasury Purchases," Finance and Economics Discussion Series 2010-52, Washington: Board of Governors of the Federal Reserve System, September.

Davis, Steven J., R. Jason Faberman, and John C. Haltiwanger (2010). "The Establishment-Level Behavior of Vacancies and Hiring ," NBER Working Paper Series 16265. Cambridge, Mass.: National Bureau of Economic Research, August.

Gagnon, Joseph, Matthew Raskin, Julie Remache, and Brian Sack (2010). "Large-Scale Asset Purchases by the Federal Reserve: Did They Work? " Staff Report No.441. New York: Federal Reserve Bank of New York, March.

Hamilton, James D., and Jing (Cynthia) Wu (2010). "The Effectiveness of Alternative Monetary Policy Tools in a Zero Lower Bound Environment (467 KB PDF) ," working paper. San Diego: University of California, San Diego, August (revised October).

Joyce, Michael, Ana Lasaosa, Ibrahim Stevens, and Matthew Tong (2010). "The Financial Market Impact of Quantitative Easing (748 KB PDF) ," Working Paper 393. London: Bank of England, July (revised August).

Kaplan, Greg, and Sam Schulhofer-Wohl (2010). "Interstate Migration Has Fallen Less than You Think: Consequences of Hot Deck Imputation in the Current Population Survey ," NBER Working Paper Series 16536. Cambridge, Mass.: National Bureau of Economic Research, November.

Kim, Soyoung (2001). "International Transmission of U.S. Monetary Policy Shocks: Evidence from VAR's," Journal of Monetary Economics, vol. 48 (October), pp. 339-72.

Kuang, Katherine, and Rob Valleta (2010). "Extended Unemployment and UI Benefits ," Federal Reserve Bank of San Francisco, FRBSF Economic Letter, 2010-10, April 19.

Modigliani, Franco, and Richard Sutch (1966). "Innovations in Interest Rate Policy," American Economic Review, vol. 56 (March), pp. 178-97.

Tobin, James (1958). "Liquidity Preference as Behavior towards Risk," Review of Economic Studies, vol. 25 (February), pp. 65-86.

Uribe, Martin, and Vivian Z. Yue (2006). "Country Spreads and Emerging Countries: Who Drives Whom? " Journal of International Economics, vol. 69 (June), pp.6‑36.

Vayanos, Dimitri, and Jean-Luc Vila (2009). "A Preferred-Habitat Model of the Term Structure of Interest Rates ," NBER Working Paper Series 15487. Cambridge, Mass.: National Bureau of Economic Research, November.

1. These remarks solely reflect my own views and not necessarily those of any other member of the FOMC. I appreciate assistance from members of the Board staff--David Bowman, James Clouse, William English, Andrew Figura, Steven Kamin, Yuriy Kitsul, Andrew Levin, Fabio Natalucci, David Reifschneider, Clara Vega, William Wascher, and David Wilcox--who contributed to the preparation of these remarks. Return to text

2. This downward trend in inflation has not been confined to any specific sectors of the economy, such as housing. For example, the Federal Reserve Bank of Dallas constructs a trimmed-mean rate of PCE inflation by removing the tails of the distribution of monthly price changes for disaggregated spending categories. That measure of underlying inflation has also declined fairly steadily since mid-2008 and dipped slightly below 1 percent last autumn. Moreover, diffusion indexes of price changes--which subtract the percentage of items in the consumption basket with price increases from the percentage of items with price decreases--also fell noticeably over this period, providing further evidence that the decline in inflation has been widespread across many categories of consumer spending. Return to text

3. As indicated in the minutes of the November FOMC meeting, the Committee has also considered the potential costs and benefits of setting a peg for a term interest rate. While targeting the yield on a term security could be an effective way to reduce longer-term interest rates, such an approach might require the Federal Reserve to make an open-ended commitment to purchasing longer-term securities. Return to text

4. Examples include Culbertson (1957), Tobin (1958), and Modigliani and Sutch (1966); see also Vayanos and Vila (2009). Return to text

5. A burgeoning literature focuses on the experience of asset purchase programs of the Federal Reserve and other central banks; for example, see D'Amico and King (2010); Gagnon, Raskin, Remache, and Sack (2010); Hamilton and Wu (2010); and Joyce, Lasaosa, Stevens, and Tong (2010). Return to text

6. See Ben S. Bernanke (2008), "Monetary Policy and Asset Prices Revisited," speech delivered at the Greater Austin Chamber of Commerce, Austin, Tex., December 1. Return to text

7. The December 2008 FOMC announcement also reported the Committee's decision to reduce the target for the federal funds rate to a range of 0 to 1/4 percent. Return to text

8. See Chung and others (2011). Return to text

9. In addition, the federal funds rate is assumed to remain unchanged from baseline for several years and then to follow the prescriptions of a simple estimated policy rule; for further details, see Chung and others (2011). Return to text

10. The simulation results are reported as deviations from baseline and hence eventually return to zero. In effect, under circumstances in which the baseline path involves a large and relatively persistent unemployment gap, these results can be interpreted as gauging the extent to which the policy stimulus accelerates the pace at which the economy returns to its balanced-growth path with maximum sustainable employment and low, stable inflation. Return to text

11. See Chung and others (2011) for further details. Return to text

12. Consistent with the conjecture that bond yields are affected by expected purchase size, the 30-year Treasury yield increased markedly in the days following the November FOMC meeting, as market participants reportedly revised downward their expectations of the amount of purchases by the Federal Reserve in this maturity sector. Return to text

13. The backup in rates may have been amplified by technical factors such as mortgage-related hedging flows and year-end positioning by leveraged investors. Return to text

14. On changes in matching efficiency, see Barnichon and Figura (2010) and Davis, Faberman, and Haltiwanger (2010). Possible reasons for a decline in matching efficiency include decreased mobility of workers due to the drop in house prices and a mismatch between the skills demanded by businesses and the skills offered by unemployed workers. On the issue of migration rates and mobility, see Kaplan and Schulhofer-Wohl (2010). Return to text

15. See Barnichon and Figura (2010). Return to text

16. On the effect of extended unemployment benefits on the unemployment rate, see Kuang and Valleta (2010). Return to text

17. Declining demand leads businesses with positive trend growth in employment to reduce vacancies--a movement down the Beveridge curve--and businesses with flat or downwardly trending employment to increase layoffs--an outward shift in the Beveridge curve. For the response of vacancies and layoffs to changes in firm-level employment, see Davis, Faberman, and Haltiwanger (2010). Return to text

18. For the purposes of this discussion, the EMEs comprise Argentina, Brazil, Chile, China, Colombia, Hong Kong, India, Indonesia, Malaysia, Mexico, the Philippines, Singapore, South Korea, Taiwan, Thailand, and Venezuela. Return to text

19. Kim (2001), Canova (2005), and Uribe and Yue (2006), among others, find that U.S. monetary stimulus affects aggregate output in emerging market and advanced foreign economies positively. Return to text