September 30, 2020

Community Banks Rise to the Challenge

Governor Michelle W. Bowman

At "Community Banking in the 21st Century," Research Conference, the Federal Reserve Bank of St. Louis, St. Louis, Missouri (via webcast)

Thank you, it is a pleasure to join you virtually today and share a few thoughts on what I am hearing from community banks in the wake of the pandemic, and what the Federal Reserve is doing to assist in the recovery.

When I addressed this conference exactly a year ago, the world was a very different place. COVID-19 has brought hardship and disruption to nearly every aspect of our lives, and even as economic conditions improve, the pandemic continues to weigh on households, businesses, and the economy. Today, I would like to offer some of my observations on current conditions and share with you what I have learned in discussions with community bankers across the nation. This input has shaped my views of how supervision and regulation are affecting community banks in these challenging times—what is working, and what needs to improve. In addition to the Fed's usual consultation with community banks, I have separately embarked on an effort to meet directly with the CEOs of all 685 community banks supervised by the Fed, an undertaking that has already provided valuable insights that I will relate in these remarks.

What Community Banks Have Achieved

America has never experienced a health and economic crisis like the one we are facing. The measures taken to contain the virus and the ensuing sudden stop to the economy beginning in March were unprecedented, just as some aspects of the downturn. One of these is the extent to which small businesses have been affected. Small businesses tend to be service-oriented and clustered in retail and food services, with many less able than larger companies to maintain operations via remote work. Because community banks are a major source of credit and financial services for small businesses, this crisis has had a heavy impact on their customers, and in their communities.

Another unusual aspect of this event, which I have noted before, is the geographic variation in the timing and severity of the pandemic's effect.1 Given the widely varying rates of infection, and the distinct approaches of states and localities in dealing with the virus, we are seeing divergent experiences in economic performance in different areas of the country.

As a result, and to a greater extent than in the past, this slowdown is being felt differently from community to community, and is being responded to differently from community to community. So it is no surprise that community banks are standing shoulder to shoulder with their customers, on the front lines. You have done this before, of course, during past recessions, but for the reasons I've outlined, your role this time has never been more critical. That is why one of the government's first responses to the pandemic was the Paycheck Protection Program (PPP), geared to small business, and necessarily dependent on community banks. So let me start there, and review what has been accomplished through PPP and discuss the role of community banks in that program.

Based on preliminary results, it appears PPP was timely and effective in helping millions of businesses weather the lockdown period. It was also designed in a way that made community banks integral to its success. The first funds reached businesses roughly three weeks after the need for that relief was recognized. To provide perspective, $525 billion, or roughly 19 times the value of all Small Business Administration lending in fiscal year 2019, was distributed in the four months from April through August 8.2,3 Community banks with $10 billion or less in assets made about 40 percent of the overall number and value of PPP loans.4 Community banks were absolutely essential to the success of this program.

This outcome is probably not surprising to this audience, because when it comes to lending to small businesses, community banks have always been an outsized source of credit, relative to their size in the banking system. Before the pandemic, community banks accounted for over 40 percent of all small business lending, while they only accounted for roughly 15 percent of total assets in the banking system.

Community banks know their individual and small business customers, and they know their communities. In my conversations with community bank CEOs, several reported to me that early in the pandemic they directly contacted every single one of their business and consumer loan customers, taking the time to check in with each one to see how they were doing, and what they needed. They encouraged customers to keep in touch with the bank, and they noted the available opportunities for payment deferrals that customers might not have been aware of. They asked, "Do you need us and how can we help?" In this pandemic, it means going further, than other banks could or would. According to the 2020 national survey conducted by the Conference of State Bank Supervisors, more than one-third of community banks reduced or eliminated penalties or fees on credit cards, loans, or deposits.5 One banker in Colorado told me that his bank called 3,700 individual borrowers offering deferrals—and that 2,000 of them accepted.

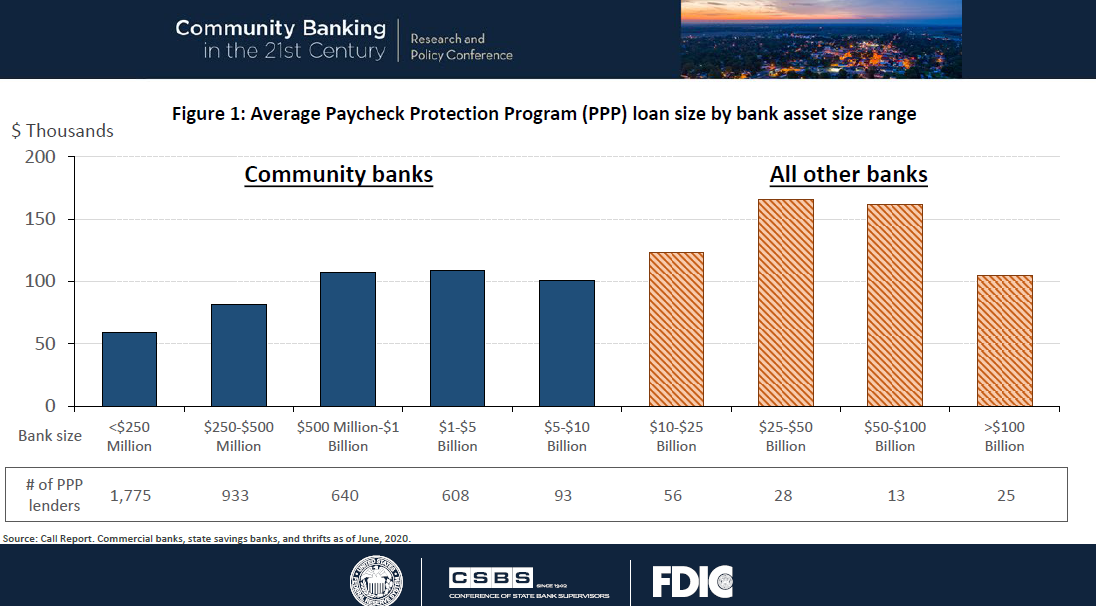

Let me highlight the role of smaller community banks in the PPP, because they demonstrate the agility and close relationships with customers that was so important in connecting with the businesses most threatened by the lockdowns. Banks with less than $1 billion in assets have made a million loans under the PPP, about one-fifth the total, delivering $85 billion in relief to their customers.6 Additionally, as shown in figure 1, the smallest banks made the smallest PPP loans on average, illustrating that these banks play a key role in serving businesses that may be outside the focus of larger banks. The average PPP loan size at banks with total assets under $500 million was just $72,000, about half the size of the average loan at banks with total assets between $10 billion and $100 billion.

{kind=link}

Additionally, preliminary data based on an Independent Community Bankers of America report indicates that community banks have been the main source of lending for minority-owned small businesses during the pandemic, accounting for 73 percent of all PPP loans made to small businesses owned by non-whites. Early estimates also suggest that community banks provided 64 percent of PPP loans to majority veteran-owned businesses.7 Within the broader community banking sector, there are banks that have the mission to serve low-income and minority communities. Specifically, I am referring to minority depository institutions (MDIs) and community development financial institutions (CDFIs). These institutions had previously established relationships with minority and low-income small business owners and were quickly able to provide them access to PPP loans. Additionally, as trusted institutions in their communities, new businesses sought them out as lenders who understood their unique, and sometimes challenging, business needs. The Cleveland Fed recently published an article entitled "I can't believe I got a real person," which describes one minority-owned small business's experience successfully getting a PPP loan from an MDI in Los Angeles.8 The title alone captures why community banks were so important for small businesses seeking PPP loans—small banks offer a personalized level of customer service that big banks do not. It is also striking that smaller community banks were the predominant lenders despite having a smaller staff and while facing lobby closures and other workforce challenges due to COVID-19. Several of the bankers I spoke with worked from home, when they couldn't open their banks. They worked overtime in drive-through facilities. They worked, in one case, inside a makeshift "disaster recovery site." Through all the ups and downs and closures and reopenings, they persevered. "We closed lobbies," a banker from Nebraska told me, "but we never closed the bank."

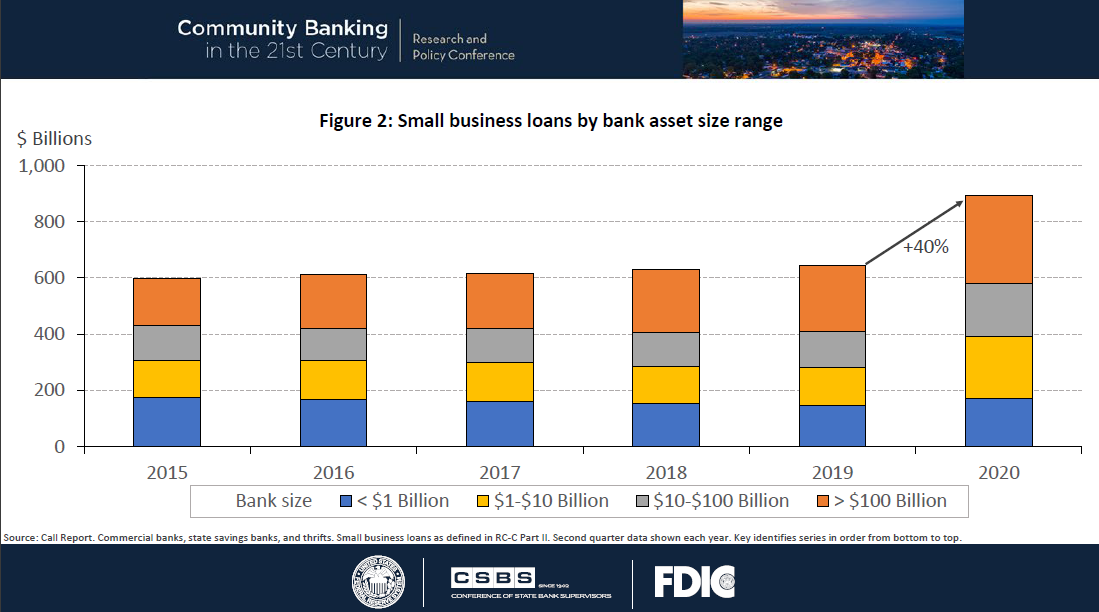

Actions like these highlight the importance and value of relationship banking, which is so central to the mission of community banks. According to the Call Report data, community banks held roughly $400 billion in small business loans in June 2020, as shown in figure 2. Loans made under the PPP totaled $197 billion—an amount representing about 40 percent of all funding provided under this program. A banker from Virginia told me, "It was a great opportunity for the community banks to show their strength."

{kind=link}

The Federal Reserve's Small Business Credit Survey shows that over one-third of small businesses turn to small banks for their lending needs.9 The survey data indicate that these borrowers are far more satisfied with their banks than the businesses who borrowed from other sources, and three out of five small businesses cite an existing relationship as a key reason they continue to do business with their bank. The PPP program strengthened many preexisting relationships between community banks and their borrowers, but community banks also met the needs of new customers facing stress from COVID-19. One bank reported 3,000 new customers from a total of 15,000 PPP loan originations. Over time, the establishment of these new relationships is likely to benefit both the community bank and the small businesses they serve.

Community Bank Supervision during the Pandemic

Now let me turn to the question of how the Federal Reserve is approaching community bank supervision during the pandemic, and how that aligns with my philosophy about how the Fed should always conduct supervision.

As you well know, community banks form a critical part of a strong and stable financial system, and they are vital to their surrounding communities. Supervising community banks requires us to strike a delicate balance between ensuring their safety and soundness and ensuring that they are able to continue serving those vital functions. This is especially true now, when community banks are supporting the businesses bearing the brunt of the economic effects of the pandemic. This situation strongly argues for flexibility in supervision.

In each of my conversations with community bank CEOs, I ask what they are experiencing and what they need, while sharing a very clear message about the Fed's flexibility: Given the challenging environment, the Fed will take into account good faith efforts by banks affected by COVID-19. In this pandemic, our common goal is to support individuals, businesses, and communities. This approach is reflected in an April 2020 statement issued by the Fed and other bank supervisors.10 In that statement, we instructed bank examiners not to criticize bank management for taking prudent steps to support their communities, and we underscored that we would not expect to take a consumer compliance public enforcement action against an institution that has made good faith efforts to comply.

This message has been getting through to examiners. One community banker in Texas that I spoke to recently said he had been feeling the justifiable concern that granting the kind of forbearances that everyone recognizes are essential to keep businesses open will eventually come back to haunt him in an examination. When he aired this concern to the Fed, he said he felt "incredible support" when the message he received back was, "Bank your customers." This assistance is helping homeowners. A recent Federal Reserve survey found that 5 percent of homeowners with a mortgage had received a payment deferral from their lender.11

So let me extend the same message to others who might be worried: "Bank your customers."

Now let me tell you how these actions fit into my overall view of how to conduct effective bank supervision. Our goal as regulators is to ensure that each institution under our supervision is successful in managing the risks present within its operations and product offerings. Effective supervisory practices are not static. They evolve over time as lessons are learned.

That includes learning by supervisors. As one example, the volume of PPP lending has driven meaningful asset growth, especially for smaller banks. We recognize that for some institutions, this asset growth has caused many banks to exceed or nearly exceed certain asset-based thresholds contained in statutes, regulations, and reporting requirements. We are currently exploring how to address regulatory and supervisory challenges caused by this temporary asset growth.

Supervisors encourage banks to adopt best practices, and I believe that we should also seek to achieve the highest supervisory standards. First, we should clearly communicate our expectations. It is wasteful, costly, and unnecessary when compliance activity occurs because expectations have not been clearly articulated or understood. Examiners should always be able and available to explain written guidance. A second consideration is that communication must also be timely. Supervisors should promptly communicate the findings of off- and on-site analyses, which will further improve the process of answering questions and addressing issues thereby improving compliance. A third principle is transparency. The key goal here is to promote a clear and transparent supervisory process so bankers know and understand how we form our expectations and judgments, and that they will receive this information in a timely manner.

Overall, I think it is entirely appropriate to regularly ask whether our approaches to supervision are consistent with the stated policy objectives of efficiency, safety and soundness, and financial stability. One of those objectives is a healthy community banking sector that can continue to serve its customers. The pandemic has emphasized just how important that is.

The Leading Challenge for Community Banks

Another theme I have heard repeatedly from CEOs is the strong message that they are struggling with the cost and burdens of regulatory compliance. Many bankers have said they consider this the most significant threat to their existence. According to the CSBS National Survey, relative compliance costs actually decreased modestly in 2019, which may be a sign that some of the steps we are taking are helping. This is consistent with what I heard from one Oklahoma banker, who said the biggest threat to his long-term survival was regulatory burden—but "not so much in the last few years."

We know examinations are top of mind for every community banker, and we are aware some bankers are also concerned with the length of time associated with the examination process. Community bank exams generally consist of phases—pre-exam contact, scoping, conducting the exam, and, finally, the drafting and delivery of the report. From a banker's perspective, the exam begins with the first day letter or perhaps the first contact of an examiner with the bank, and ends with receipt of the report of exam. From a banker's perspective, exams can seem as though they last for many months, which can strain resources for community banks that are unable to dedicate staff exclusively to managing the examination process. This is a valid concern, and achieving an appropriate timeframe for the length of exams, whether that be safety and soundness or consumer compliance, is very important to me. We are committed to evaluating our policies, practices, and implementation processes to understand and identify opportunities to address these concerns.

There are other significant concerns for community bankers, but these only compound the challenge posed by regulatory burden. Bankers worry about competition from larger banks with economies of scale that are sufficient to drive consolidation. One of the biggest advantages from scale comes in regulatory compliance. As one banker in Wyoming told me: "Consolidation is a huge threat as larger banks can deliver at a far lower cost." One of the biggest costs, of course, is regulatory compliance. Researchers from the St. Louis Fed found that compliance expenses averaged nearly 10 percent of total non-interest expenses for banks with less than $100 million in total assets. For banks with between $1 billion and $10 billion in total assets, compliance expenses averaged 5.3 percent of total non-interest expense. This suggests that the regulatory cost burden for the smallest community banks is nearly double that of the largest community banks.

In a speech about community banking regulation, it is entirely appropriate to point out our work on tailoring efforts. However, on its own, tailoring does not ensure that existing regulations are not unduly burdensome for smaller banks. These banks may benefit from further regulatory relief, without undermining the goals of safety and soundness, consumer protection, and financial stability. Regulatory burden can be manifested in multiple ways, including the attitude that examiners have in their interactions with banks. That is why the supervision principles I outlined earlier are so important. Supervisors need to communicate intentions clearly, in a timely manner, and in a transparent way. Doing so consistently can significantly lighten the regulatory burden that is such a challenge for banks.

Current Economic and Financial Conditions for Banks

I will conclude with a few comments about economic and financial conditions as they affect community banks. Our nation has suffered the sharpest drop in economic activity in U.S. history, and while unemployment remains quite high, the recent economic data have been encouraging and suggest that our national economy has been recovering at a rapid pace. The substantial and timely fiscal stimulus provided by Congress and the Administration has made a meaningful contribution to this recovery. Looking ahead, continued monetary and targeted fiscal policy support will likely be needed. Even with this support, however, I anticipate that the path toward full recovery will be bumpy, and that our progress will likely be uneven. Asset prices in particular, remain vulnerable to significant price declines should the pandemic seriously worsen. Some hotels and other businesses are in arrears on rent and debt service payments, and we are watching the commercial real estate market closely for signs of further stress. I also expect the pace of the recovery will continue to vary from area to area, and will be heavily influenced by not only the course of the virus, but also the public policy decisions made across all levels of government.

Before the COVID-19 pandemic began, all of the data told us that community banks began this year in excellent shape—by some measures the strongest in decades. Ninety-six percent of community banks were profitable; nonperforming assets neared historical lows, and capital ratios were strong. More than 95 percent of small banks were rated as 1 or 2 under the CAMELS rating system. These banks built strong capital positions and substantially improved asset quality metrics in the years following the last crisis. They also entered the pandemic with high levels of liquidity that have been augmented by deposit inflows associated with the pandemic-related stimulus programs. Finally, credit concentrations were generally much lower, especially in construction and commercial real estate, and broadly speaking, concentration risk management practices significantly improved since the financial crisis.

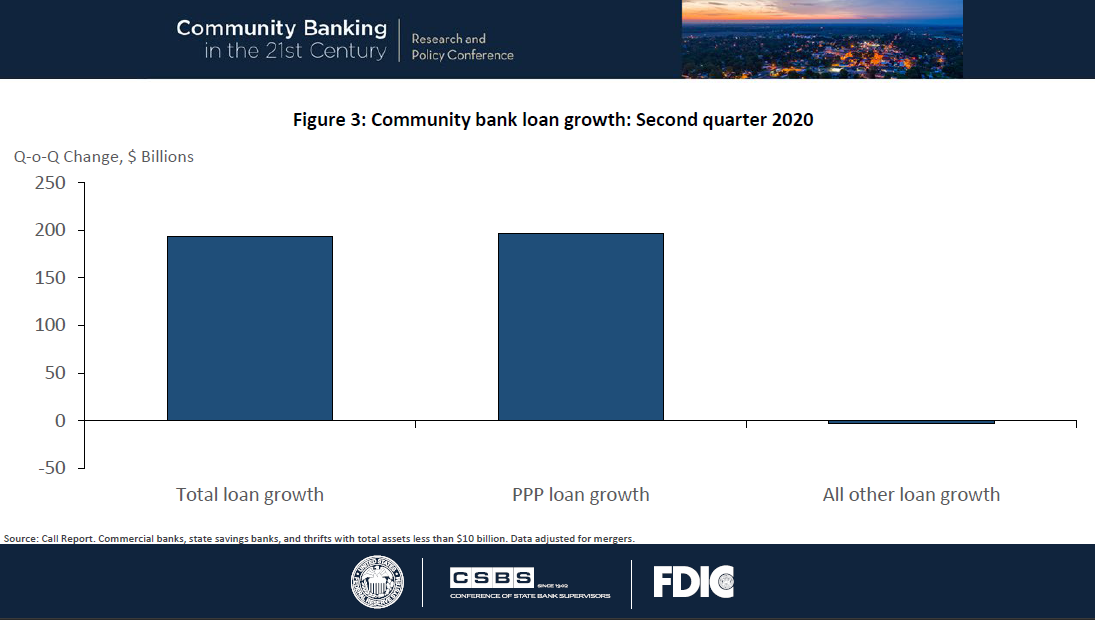

Following a weak first quarter that included higher credit loss provisions, second-quarter earnings showed improvement. Aggregate return on assets recovered more than two-thirds of the decline reported during the first quarter, driven by higher noninterest income and lower operating expenses. Origination fees and interest income from PPP lending fueled some of this improvement, with many community banks reporting substantial loan growth as a result of the program, and a few actually doubling their balance sheets. As seen in figure 3, the quarter-over-quarter loan growth would have been negative, absent the PPP loans. As origination fees and interest income are generally recognized over the life of these loans or when they are forgiven, PPP loans will continue to push up bank earnings in the next several quarters. The origination fees earned by community banks this year will mitigate the impact of provisions for credit losses, and in turn, may support further lending by these banks.

{kind=link}

Despite improvement in these areas, the operating environment remains challenging. The average net interest margin at community banks tightened during the second quarter, and it is likely that margins will remain under pressure given the low interest rate environment. But community banks have historically performed well even when interest margins were under pressure, and they entered into the pandemic in sound financial condition.

So what do we take away from this review of bank numbers and performance? In all, I expect community banks will face challenges during what could be a slow return to a full economic recovery, but I also expect that this sector is well prepared to deal with these challenges and will continue to perform the vital role it has played during the response to the pandemic. My hope is that at next year's conference we will have additional data and research that paint a fuller picture of the role community banks played in our nation's response to and recovery from COVID-19, and that we have gained further insights into the role of all community banks, including MDIs and CDFIs, in ensuring access by all to credit and financial services.

1. Michelle W. Bowman, "The Pandemic's Effect on the Economy and Banking" (speech at Kansas Bankers Association CEO and Senior Management Forum/Annual Meeting, Topeka, Kansas (via webcast), August 26, 2020). Return to text

2. Small Business Administration, Paycheck Protection Program (PPP) Report (PDF) (Washington: Small Business Administration, August 8, 2020). Return to text

3. Small Business Administration, Agency Financial Report: Fiscal Year 2019 (PDF) (Washington: Small Business Administration, November 15, 2019). Return to text

4. Call Report for commercial banks, state savings banks, and thrifts as of June 2020. Return to text

5. Conference of State Bank Supervisors, "National Survey of Community Banks" Return to text

6. Small Business Administration, Paycheck Protection Program (PPP) Report. Return to text

7. Independent Community Bankers of America, "Data Show Community Banks Lead Economic Recovery," news release, August 19, 2020. Return to text

8. Michelle Park Lazette, "'I Can't Believe I Got a Real Person': Small Bank Answers Businesses' Cries for Help," Medium, September 3, 2020, https://medium.com/new-york-fed/i-cant-believe-i-got-a-real-person-small-bank-answers-businesses-cries-for-help-844b482ab5ba. Return to text

9. Federal Reserve, "Small Business Credit Survey (PDF)," (2020). Return to text

10. See Board of Governors of the Federal Reserve System, Federal Deposit Insurance Corporation, National Credit Union Administration, Office of the Comptroller of the Currency, and Consumer Financial Protection Bureau, "Interagency Statement on Loan Modifications and Reporting for Financial Institutions Working with Customers Affected by the Coronavirus (Revised) (PDF)," news release, April 7, 2020. Return to text

11. Board of Governors of the Federal Reserve System, "Update on the Economic Well-Being of U.S. Households: July 2020 Appendixes (PDF)," (September 2020). Return to text