May 28, 2024

The Federal Reserve's Balance Sheet as a Monetary Policy Tool: Past Lessons and Future Considerations

Governor Michelle W. Bowman

At the 2024 BOJ-IMES Conference, hosted by the Institute for Monetary and Economic Studies, Bank of Japan, Tokyo, Japan

I would like to thank the Bank of Japan and Governor Ueda for organizing this year's conference and for the invitation to participate in this afternoon's panel.1 The topic of "the effects of conventional and unconventional policy instruments" is an important one given central banks' expanded use of unconventional monetary policy tools to pursue their mandates over the past decade and a half.

My remarks focus on the use of the central bank balance sheet as a monetary policy tool. I will first offer some observations regarding the benefits and costs of large-scale asset purchases (LSAPs) by reflecting on the two episodes of the Federal Reserve's active use of the balance sheet in U.S. monetary policy following the 2008 financial crisis and during the COVID-19 pandemic. I will then discuss some considerations regarding future balance sheet policy as the Federal Open Market Committee (FOMC) seeks to bring inflation back down to its 2 percent target following the post-pandemic inflation surge, and as the FOMC continues to reduce the size of the Federal Reserve's balance sheet.

Lessons Learned from Past Uses of the Federal Reserve's Balance Sheet as a Monetary Policy Tool

Post-2008 financial crisis balance sheet policy

A key challenge for the FOMC following the 2008 financial crisis was how to provide additional support to an economy that was experiencing high unemployment and subdued inflation after the FOMC lowered its primary and conventional monetary policy tool—the target range for the federal funds rate—to near zero. Given the importance of longer-term interest rates for broader asset prices and for investment and consumption decisions, the FOMC used both forward guidance and LSAPs to help lower longer-term rates, which had not yet moved to zero. The intent of forward guidance was to lower longer-term interest rates by shifting expectations of "low-for-long" short-term interest rates in line with a low-for-long federal funds rate. LSAPs, or quantitative easing (QE), were intended to reduce longer-term interest rates further by lowering the yields of specific longer-dated securities being purchased and by reducing more generally the term premia, the compensation that investors must earn to incentivize investment in a longer-term bond relative to a short-term bond. LSAPs could also reinforce the FOMC's forward guidance of low-for-long short-term interest rates. Such reinforcement of low-for-long forward guidance could be especially powerful if the FOMC communicated that it would not consider raising the target range for the federal funds rate until it stopped actively engaging in asset purchases for the purposes of QE.

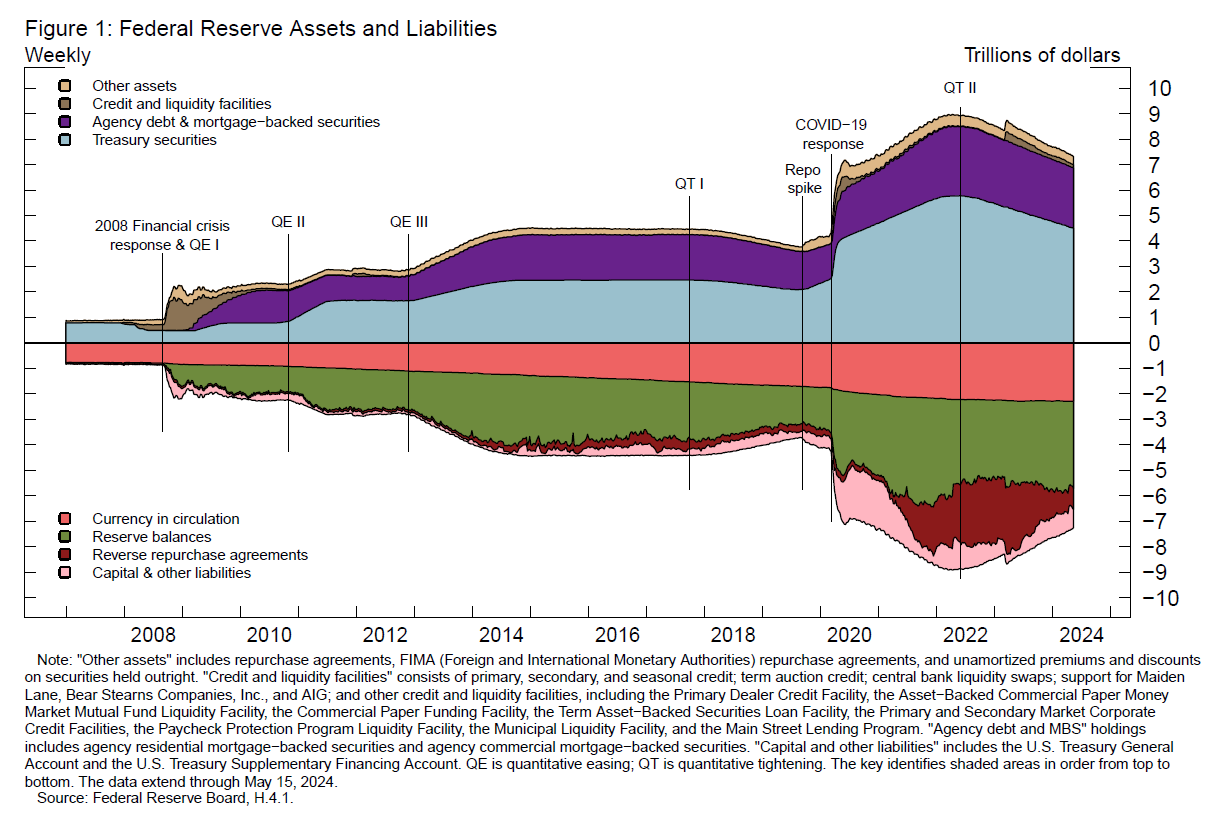

The Federal Reserve purchased both Treasury securities and agency mortgage-backed securities (MBS) as part of its QE programs from 2009 to 2014. Figure 1i shows the evolution of the Federal Reserve balance sheet assets and liabilities from before the 2008 financial crisis to the present. The Fed's Treasury and agency securities holdings increased from around half a trillion dollars to around $4.25 trillion by the end of the third round of QE, which ended in 2014. A range of studies indicate that the Fed's asset purchases were effective in raising the prices of and lowering the yields on the targeted class of securities.2 Research suggests that these asset purchases also helped lower term and risk premia across other asset classes, including corporate securities.3 The impact on the MBS pricing and credit flow was significant since securities prices in this asset class were especially impacted during the financial crisis. Financial institutions holding MBS on their balance sheets, including banks, were also significantly affected.

{kind=link}

Some studies have documented that the Fed's agency MBS purchases encouraged banks to continue to lend as the prices of their on-balance-sheet MBS holdings rose in response to QE.4 Overall, the evidence indicates that the Fed's LSAPs following the financial crisis helped support the economic recovery. The progress on the FOMC's dual mandate of maximum employment and price stability was assisted by the further easing of financial conditions after the federal funds rate had reached its effective lower bound.5 The post–financial crisis period experience showed that securities purchases in a specific asset class could be effective for those asset classes that had experienced stress, as was the case with MBS during that period.

The Federal Reserve concluded its asset purchases in 2014, after initiating the tapering process in 2013. In 2017, the Fed began to reduce its securities holdings, which is often referred to as quantitative tightening (QT). In January 2019, the FOMC voted to operate monetary policy in an "ample reserves" environment.6 This change in the policy implementation framework had the effect of keeping the size of the balance sheet much larger and providing more liquidity to the banking system in normal times than had been the case before the financial crisis. The FOMC ended QT in August 2019, and balance sheet growth resumed in October 2019 through the purchase of U.S. Treasury bills and securities following a brief period of stress in money markets in which the interest rates on repurchase agreements and other short-term funding instruments jumped, as noted by the line labeled "Repo Spike" in figure 1. This stress was interpreted as an indication that the level of reserves had fallen below ample levels.7

Overall, one could deem the post–financial crisis use of the Federal Reserve's balance sheet as a monetary policy tool as a success. Unemployment fell and inflation remained near 2 percent through the period over which LSAPs were conducted. The FOMC was able to end LSAPs and eventually was able to partially unwind them, though the overall terminal size of the Fed's securities holdings as a share of GDP following the end of QT was much greater than before the financial crisis. This much larger end state was a direct result of the FOMC's decision to implement monetary policy in an ample-reserves operating framework and had the effect of lowering the likelihood of future volatility in short-term funding markets.8

COVID-19 pandemic balance sheet policy

Given the effectiveness of the balance sheet as a monetary policy tool over the previous decade, the FOMC rapidly deployed LSAPs in March 2020 as part of its response to the pandemic.9 These purchases followed the onset of the COVID-19 pandemic at that time, and the FOMC returned the federal funds rate to its effective lower bound. Following an initial higher level of Treasury and agency MBS purchases motivated both by restoring market functioning following a period of severe stress and by providing monetary policy accommodation, the FOMC began to purchase $80 billion of Treasury securities and $40 billion of agency MBS per month. In its December 2020 post-meeting statement, the FOMC communicated that it intended to continue this pace of asset purchases "until substantial further progress has been made toward the Committee's maximum employment and price stability goals."10 By the end of the pandemic period asset purchases, total securities held by the Federal Reserve stood at around $8.5 trillion.

The pace of asset purchases during the pandemic period was much greater than in the previous QE episodes. Conditions in the economy and financial system were also different than those that prevailed following the 2008 financial crisis in significant ways. The stabilizing actions taken by the Federal Reserve to restore market functioning and to support financial stability in the first half of 2020, in addition to the much higher capital levels in the banking system relative to 2008, enabled the financial system to remain resilient. Credit continued to be available to households, businesses, and local governments following the pandemic's onset.

The U.S. Congress and the Administration also provided extraordinary fiscal support in response to the pandemic—which included stimulus checks sent to households, expanded unemployment insurance, and the Paycheck Protection Program—that bolstered household and business balance sheets.11 The housing market—recently recovered from the buildup of poorly underwritten mortgage debt in the lead-up to the 2008 financial crisis and a subsequent steep decline in house prices—remained in sound condition. And as households and families sought larger living spaces and amenities as they worked from home during the pandemic, house prices increased sharply.

In hindsight, the sharp contrast between the economic and financial system conditions during the pandemic period and those following the 2008 financial crisis raise questions about the similarities in the response of the Federal Reserve and FOMC to these events. Was such a strong balance sheet policy response during the pandemic appropriate, and to what extent did such a strong balance sheet policy response contribute to the buildup of inflationary pressures and the post-pandemic inflation surge? Given the underlying strength in the housing market, should the FOMC have conducted such large purchases of agency MBS into late 2021? Given the strong fiscal response to support spending by households and businesses and large issuance of Treasury debt, should the FOMC have conducted such large purchases of Treasury securities into late 2021? I look forward to our conversation today and to future studies on these questions, such as those conducted regarding the effectiveness of balance sheet policies following the 2008 financial crisis.

My own view is that the FOMC would likely have benefited from an earlier discussion and decision to begin tapering and subsequently end asset purchases in 2021 given the signs of emerging inflationary pressures.12 Doing so would have allowed the FOMC the option to have begun to tighten monetary policy earlier by raising the target range for the federal funds rate. While a robust and rapid response by the FOMC was appropriate in 2020, I think it is worth asking whether such a robust response for so long was appropriate. The economic and financial system conditions were very different during the pandemic and included a strongly accommodative fiscal backdrop.

Could the FOMC have reduced its pace of asset purchases earlier once it was clear that market turmoil had subsided, just as the 13(3) emergency lending facilities established in 2020 were allowed to expire and exit plans developed for those programs? A thorough discussion of these questions will be a useful reference for the FOMC and other central banks as they consider future use of QE as a monetary policy tool. This perspective would be helpful for historical reference when formulating appropriate balance sheet policy as a monetary policy response to future episodes when the conventional interest rate tool is near zero.

Another important difference between the FOMC's balance sheet policy following the pandemic and its balance sheet policy following the 2008 financial crisis was the speed and timing of the subsequent reduction in the size of the Federal Reserve's securities holdings during the period of QT.13 This difference reflects the larger amount of securities purchases compared to the earlier periods of QE as well as the quite different economic conditions facing the FOMC at the start of QT post-pandemic. These conditions included too-high inflation and a desire by the FOMC to tighten monetary policy through both the federal funds rate and the balance sheet tools.

So far, the rapid and sustained pace of the Federal Reserve's securities runoff has proceeded relatively smoothly. A useful question for further inquiry is to what extent during the post-pandemic period has QT served to further tighten financial conditions. With the understanding that QT is a tool employed beyond conventional monetary policy restriction, how does one measure the incremental increase above the FOMC's concurrent increases in the target range for the federal funds rate and related forward guidance regarding its policy rate? Evidence to date suggests that QT exerts an independent effect on tightening financial conditions, though in some cases it may be asymmetric to the effects of QE.14 Quantifying the effects of QT as well as QE will be helpful to policymakers in their future deliberations regarding use of the balance sheet in setting monetary policy.

Future Considerations regarding the Federal Reserve's Balance Sheet Policy

Looking ahead, the FOMC continues to reduce the size of its balance sheet as it seeks to maintain a sufficiently restrictive stance of monetary policy to bring inflation back down to its 2 percent goal. Recently, the FOMC voted to slow the pace of securities runoff by around half beginning in June.15 In its Plans for Reducing the Size of the Federal Reserve's Balance Sheet released in May 2022, the FOMC noted that it would eventually slow and then stop securities runoff when reserve balances are somewhat above the levels it judges to be consistent with ample reserves to ensure a smooth transition to ample-reserves levels.16 Aggregate reserve levels currently stand at around the levels at the start of balance sheet runoff in June 2022, and there are still sizable balances in the overnight reverse repurchase agreement (ON RRP) facility. In light of these conditions, I would have supported either waiting to slow the pace of balance sheet runoff to a later point in time or implementing a more tapered slowing in the pace of runoff.17

While it is important to slow the pace of balance sheet runoff as reserves approach ample levels, in my view we are not yet at that point, especially with still sizable take-up at the ON RRP.18 In my view, it is important to continue to reduce the size of the balance sheet to reach ample reserves as soon as possible and while the economy is still strong. Doing so will allow the Federal Reserve to more effectively and credibly use its balance sheet to respond to future economic and financial shocks.

As balance sheet runoff proceeds, however, it will eventually be appropriate to stop runoff as reserves near an ample level. The FOMC will be monitoring money market conditions and related interest rates as it assesses the point at which reserve levels reach ample.19 It will be important to communicate that any future changes to balance sheet runoff do not reflect a change in the FOMC's monetary policy stance. Not effectively communicating this point might cause the public to interpret the endpoint of QT as a signal that the FOMC would decrease the target range for the federal funds rate, thereby causing financial conditions to inappropriately ease.

Another important issue regarding future balance sheet policy is what the composition of the Federal Reserve's securities holdings should be in the longer run. As noted in the FOMC's January 2022 Principles for Reducing the Size of the Federal Reserve's Balance Sheet, the FOMC intends to hold primarily Treasury securities in the longer run to minimize the effects of the Federal Reserve's holdings on the allocation of credit across the economy.20 I strongly support this principle. Consistent with this statement, the FOMC will reinvest any principal payments from agency MBS holdings above the current runoff cap into Treasury securities. And once balance sheet runoff concludes, my expectation is that proceeds from agency MBS holdings would continue to be reinvested in Treasury securities in order to facilitate a transition of the Federal Reserve's balance sheet holdings to consist of primarily Treasury securities.

The longer-run maturity structure of the Federal Reserve's Treasury securities holdings is also an important consideration. A benefit of a balance sheet Treasury security maturity structure that mirrors the broader Treasury market is that the Fed's holdings would be "neutral" in the sense that they would not disproportionately affect the pricing of any given maturity of Treasury security or provide incentives for the issuance of any given type of Treasury security. However, a balance sheet tilted slightly toward shorter-dated Treasury securities would allow some flexibility in approach. For example, the FOMC could reduce its holdings of shorter-dated Treasury securities in favor of longer-dated Treasury securities in a future scenario in which the FOMC wanted to provide monetary policy accommodation via the balance sheet without expanding the size of its securities holdings. This approach would be similar to the FOMC's maturity extension program in 2011 and 2012, sometimes referred to as "operation twist."21 It will be important to consider such potential costs and benefits to the Federal Reserve's Treasury securities maturity structure and the best ways to achieve the desired maturity structure over time.

It is also important for the FOMC to clearly distinguish when the goal of future asset purchases is restoring market functioning or supporting financial stability. In my view, when the Federal Reserve purchases securities for such purposes, it should communicate that those purchases will be temporary and subsequently unwound when financial market conditions have normalized.22

In conclusion, the FOMC's past experiences with using the Federal Reserve's balance sheet as a monetary policy tool have demonstrated that the central bank balance sheet can be an effective way to ease financial conditions and support the economy in periods in which the conventional monetary policy interest rate tool has reached the zero lower bound. Importantly, the U.S. experience shows that the effects of QE and QT can have varying effects depending on the economic and financial system environment, an important consideration for future episodes.

Just as when using the conventional monetary policy interest rate, monetary policymakers must use the balance sheet judiciously when setting monetary policy. Policymakers must also consider the risks of "doing too little" in balance with the risks of "doing too much" as they pursue their monetary policy mandates.

Thank you, and I look forward to our conversation.

1. The views expressed here are my own and are not necessarily those of my colleagues on the Federal Reserve Board or the Federal Open Market Committee. I would like to thank Rebecca Zarutskie for assistance in preparing these remarks and Neeco Beltran for assistance in preparing the figure. Return to text

2. See, for example, Mark Carlson, Stefania D'Amico, Cristina Fuentes-Albero, Bernd Schlusche, and Paul Wood (2020), "Issues in the Use of the Balance Sheet Tool," Finance and Economics Discussion Series 2020-071 (Washington: Board of Governors of the Federal Reserve System, August); Stefania D'Amico and Thomas B. King (2013), "Flow and Stock Effects of Large-Scale Treasury Purchases: Evidence on the Importance of Local Supply," Journal of Financial Economics, vol. 108 (May), pp. 425–48; and Arvind Krishnamurthy and Annette Vissing-Jorgensen (2013), "The Ins and Outs of LSAPs," paper presented at "Global Dimensions of Unconventional Monetary Policy (PDF)," a symposium sponsored by the Federal Reserve Bank of Kansas City, held in Jackson Hole, Wyo., August 22. Return to text

3. See, for example, Simon Gilchrist and Egon Zakrajsek (2013), "The Impact of the Federal Reserve's Large-Scale Asset Purchase Programs on Corporate Credit Risk," Journal of Money, Credit and Banking, vol. 45 (s2), pp. 29–57; and Simon Gilchrist, David Lopez-Salido, and Egon Zakrajsek (2015), "Monetary Policy and Real Borrowing Costs at the Zero Lower Bound," American Economic Journal: Macroeconomics, vol. 7 (January), pp. 77–109. Return to text

4. See, for example, Alexander Rodnyansky and Olivier M. Darmouni (2017), "The Effects of Quantitative Easing on Bank Lending Behavior," Review of Financial Studies, vol. (November), pp. 3858–87; Indraneel Chakraborty, Itay Goldstein, and Andrew MacKinlay (2020), "Monetary Stimulus and Bank Lending," Journal of Financial Economics, vol. 136 (April), pp. 189–218; Robert Kurtzman, Stephan Luck, and Tom Zimmermann (2022), "Did QE Lead Banks to Relax their Lending Standards? Evidence from the Federal Reserve's LSAPs," Journal of Banking and Finance, vol. 138 (May). Return to text

5. See for example Eric Engen, Thomas Laubach, and David Reifschneider (2015), "The Macroeconomic Effects of the Federal Reserve's Unconventional Monetary Policies," Finance and Economics Discussion Series 2015-005 (Washington: Board of Governors of the Federal Reserve System, February); Kyungmin Kim, Thomas Laubach, and Min Wei (2020), "Macroeconomic Effects of Large-Scale Asset Purchases: New Evidence," Finance and Economics Discussion Series 2020-047 (Washington: Board of Governors of the Federal Reserve System, June, revised August 2023); and Stephan Luck and Tom Zimmermann (2020), "Employment Effects of Unconventional Monetary Policy: Evidence from QE," Journal of Financial Economics, vol. 135 (March), pp. 678–703. Return to text

6. See the Statement Regarding Monetary Policy Implementation and Balance Sheet Normalization, which is available on the Board's website at https://www.federalreserve.gov/monetarypolicy/policy-normalization.htm. Return to text

7. See the October 2019 FOMC statement, which is available on the Board's website at https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm. Return to text

8. At the end of balance sheet runoff, the Fed's securities holdings totaled around $3.6 trillion. The FOMC had considered other types of operating regimes, including those that would result in a lower level of securities holdings in the longer run. See, for example, the discussion in the November 2018 FOMC minutes, which can be found on the Board's website at https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm. Return to text

9. The Federal Reserve also implemented 13 emergency lending and liquidity facilities under its emergency lending authorities and undertook supervisory and regulatory actions to support the flow of credit to households, businesses, and local governments; see "Funding, Credit, Liquidity, and Loan Facilities" and "Supervisory and Regulatory Actions in Response to COVID-19" on the Board's website at https://www.federalreserve.gov/funding-credit-liquidity-and-loan-facilities.htm and https://www.federalreserve.gov/supervisory-regulatory-action-response-covid-19.htm, respectively. Return to text

10. See the December 2020 FOMC statement, which is available on the Board's website at https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm (quote text in paragraph 4). Return to text

11. The Paycheck Protection Program offered low-interest loans that would be forgiven to small and medium-sized businesses that met certain criteria; see "Paycheck Protection Program" on the U.S. Small Business Administration's website at https://www.sba.gov/funding-programs/loans/covid-19-relief-options/paycheck-protection-program. Return to text

12. The FOMC discussed alternative approaches to slowing asset purchases at the September 2021 meeting; see the September 2021 FOMC minutes, which can be found on the Board's website at https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm. Return to text

13. The pace of balance sheet runoff beginning in 2022 has been roughly double the pace of the balance sheet runoff that occurred from 2017 to 2019. Return to text

14. Du, Forbes, and Luzzetti (2024) argue that the effects of QT are asymmetric to QE. This result may be due, in part, to investor expectations for QT before the authors look at announcement effects. See Wenxin Du, Kristin Forbes, and Matthew N. Luzzetti (2024), "Quantitative Tightening Around the Globe: What Have We Learned?" NBER Working Paper Series 32321 (Cambridge, Mass.: National Bureau of Economic Research, April); and Lorie Logan (2024), "Discussion of 'Quantitative Tightening Around the Globe: What Have We Learned?' by Wenxin Du, Kristin Forbes and Matthew Luzzetti," speech delivered at the 2024 U.S. Monetary Policy Forum sponsored by the University of Chicago Booth School of Business, March 1. Return to text

15. See the May 2024 FOMC statement, which is available on the Board's website at https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm. Return to text

16. See the Plans for Reducing the Size of the Federal Reserve's Balance Sheet, which is available on the Board's website at https://www.federalreserve.gov/monetarypolicy/policy-normalization.htm. Return to text

17. Aggregate reserves stood at around $3.3 trillion just before start of balance sheet runoff in June 2022; see Board of Governors of the Federal Reserve System (2022), Statistical Release H.4.1, "Factors Affecting Reserve Balances of Depository Institutions and Condition Statement of Federal Reserve Banks" (June 2). Return to text

18. Because the ON RRP and reserves are both Federal Reserve balance sheet liabilities, a one-for-one decrease in the ON RRP with securities reductions would leave the level of reserves unchanged. To date, securities runoff has largely been matched by a similarly sized reduction in the ON RRP rather than a reduction in reserves, reflecting the ON RRP's role as an excess liquidity absorbing tool during periods of large asset purchases by the central bank. Return to text

19. See Roberto Perli (2024), "Balance Sheet Reduction: Progress to Date and a Look Ahead," speech delivered at 2024 Annual Primary Dealer Meeting, Federal Reserve Bank of New York, New York, May 8. Return to text

20. See the Principles for Reducing the Size of the Federal Reserve's Balance Sheet, which is available on the Board's website at https://www.federalreserve.gov/monetarypolicy/policy-normalization.htm. Return to text

21. For more details, see "Maturity Extension Program and Reinvestment Policy" on the Board's website at https://www.federalreserve.gov/monetarypolicy/maturityextensionprogram.htm. Return to text

22. See Michelle W. Bowman (2023), "Panel on 'Design Issues for Central Bank Facilities in the Future,' " speech delivered at the Chicago Booth Initiative on Global Markets Workshop on Market Dysfunction, Chicago, March 3. Return to text

i. Note: On May 29, 2024, figure 1 was updated to correct “Credit and liquidity lacilities” to “Credit and liquidity facilities” in the legend and to correct “QE is quantitative tightening” to “QT is quantitative tightening” in the note. Return to text