September 21, 2020

Strengthening the CRA to Meet the Challenges of Our Time

Governor Lael Brainard

At the Urban Institute, Washington, D.C. (via webcast)

It is a pleasure to be back at the Urban Institute with Sarah Rosen Wartell to discuss the Federal Reserve's efforts to strengthen the Community Reinvestment Act (CRA) regulation.1 Today the Federal Reserve Board unanimously approved an advance notice of proposed rulemaking (ANPR) that would strengthen, clarify, and tailor the CRA regulation to better meet the law's core purpose.2

The CRA's History and Purpose in Relation to Today's Challenges

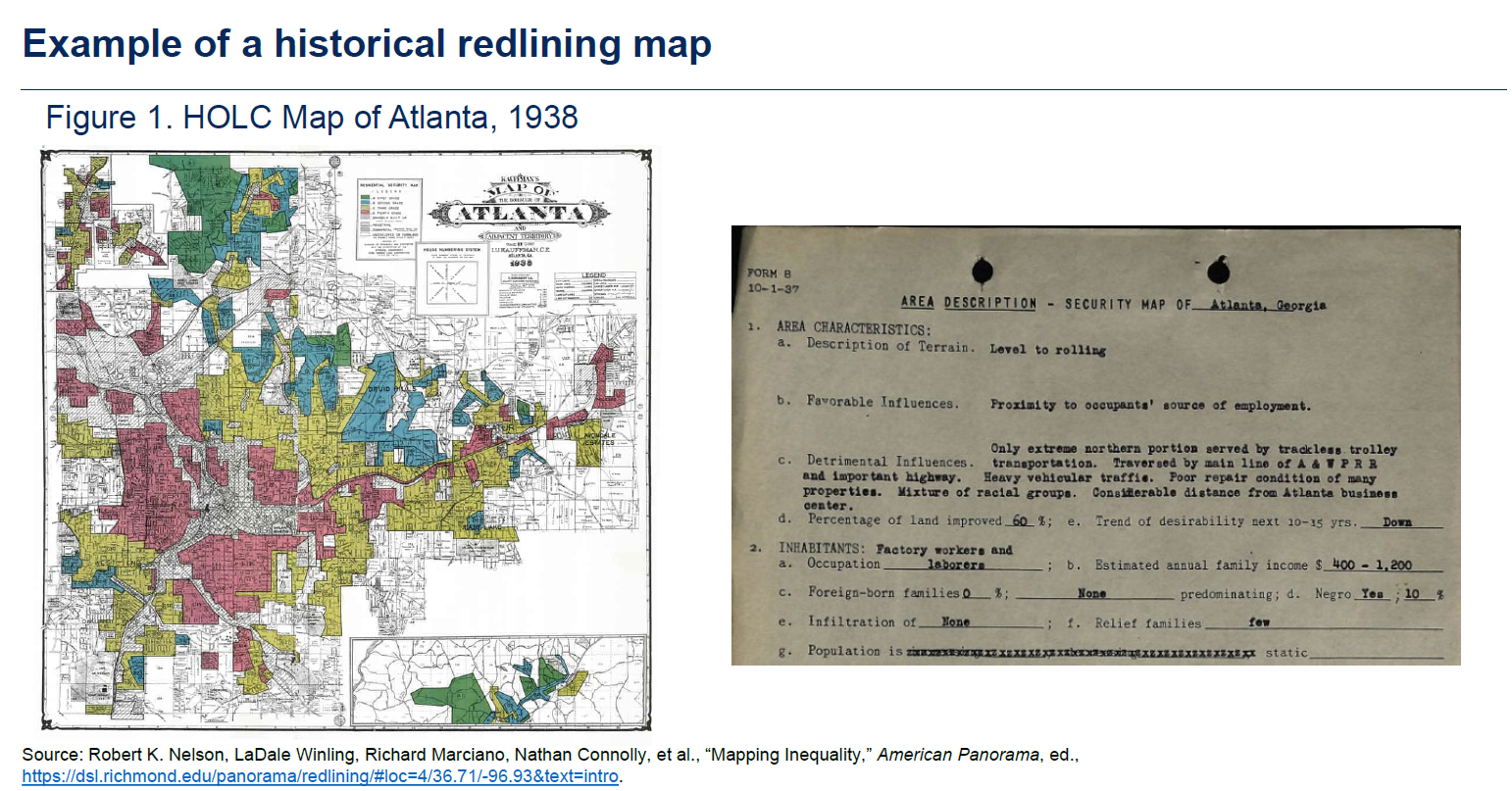

The CRA was one of several landmark civil rights laws to address systemic inequities in credit access.3 The CRA was intended to reinforce the other statutes in addressing redlining, wherein banks declined to make loans or extend other financial services in neighborhoods of largely Black and other minority households, in part based on government maps that literally delimited these neighborhoods in red as high credit risks (figure 1). By enacting the CRA, lawmakers aimed to reverse the disinvestment associated with years of government policies and market actions that deprived lower-income and predominantly minority areas of credit and investment.

{kind=link}

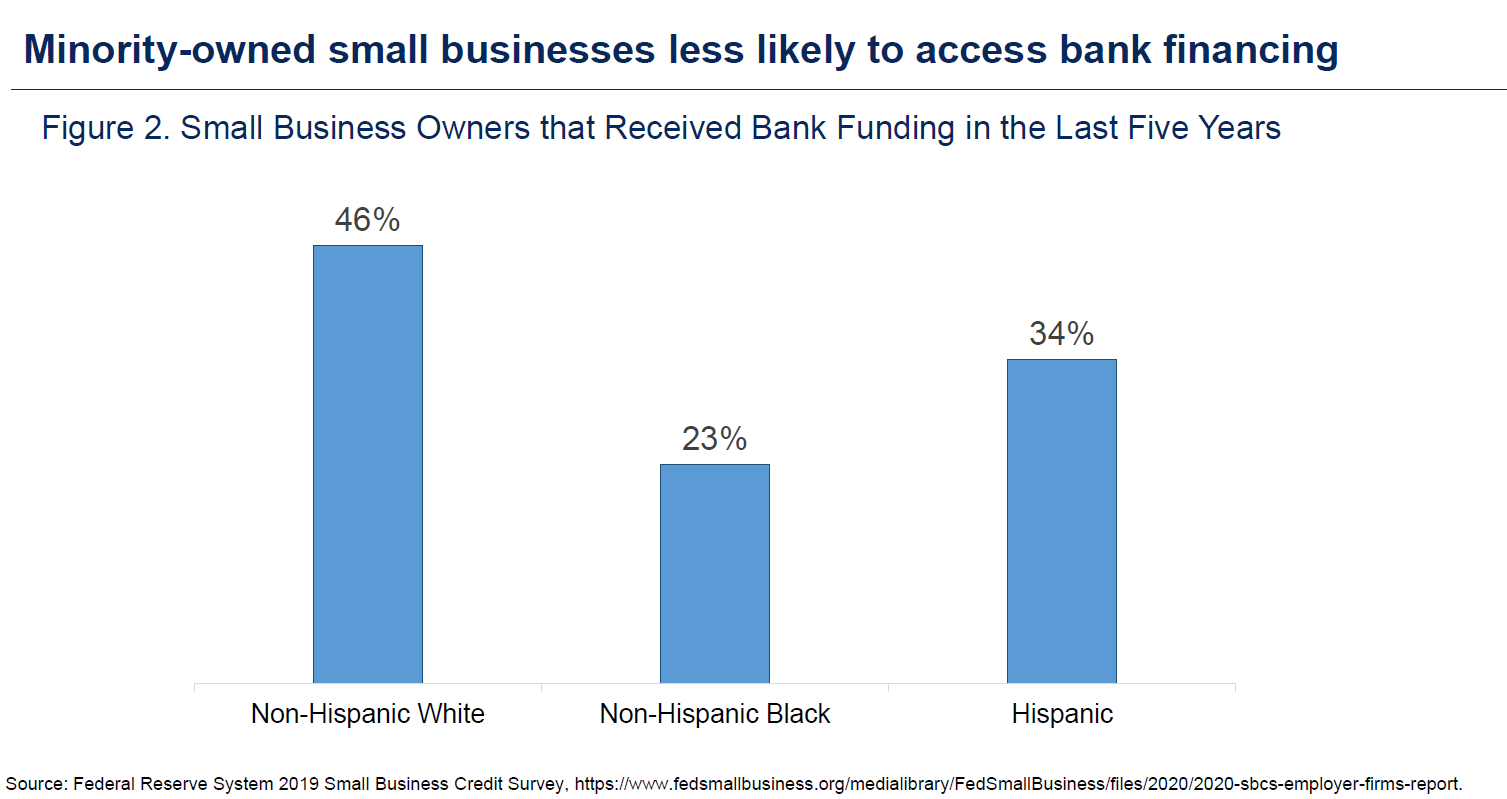

Even with these critical laws, the legacy of discriminatory lending and systemic inequity in credit access remains in evidence today. The typically minority neighborhoods demarcated in red in the old color-coded maps tend to be characterized by worse economic performance and opportunity even today.4 Beyond these specific neighborhoods, research and surveys indicate that there are ongoing racial disparities in access to credit. As of 2019, small businesses with Black ownership were only half as likely as those with White ownership to have obtained bank financing in the previous five years (figure 2).5 In 2016, the "wealth gap [was] roughly the same as in 1962, two years before the passage of the Civil Rights Act of 1964." And the gap in homeownership rates between Black and White households remains significant today, even when controlling for differences in income and education.6

{kind=link}

Recent events have highlighted and exacerbated these challenges. When I last joined you at the Urban Institute to discuss the CRA, 7 we did not know the tremendous hardship and heartache the COVID-19 pandemic would cause, especially for groups with thin financial buffers, including many low- and moderate-income (LMI) neighborhoods, Black and Latinx workers, and workers and entrepreneurs affiliated with small businesses.8 In parallel, the tragic death of George Floyd has ignited a national discussion about racial injustice and a renewed commitment to take action to address systemic inequity.9

The CRA is a seminal statute that remains as important as ever as the nation confronts challenges associated with racial equity and the COVID-19 pandemic. We must ensure that the CRA is a strong and effective tool to address ongoing systemic inequities in access to credit and financial services for LMI and minority individuals and communities.

By conferring an affirmative obligation on banks to help meet the credit needs in all of the neighborhoods they serve, the CRA prompts banks to be not only more active lenders in LMI areas but also important participants in broader efforts to revitalize communities across the country. Research shows the CRA has positive effects on access to capital and financial services for communities, including home mortgages, small business loans, and services offered at local bank branches.10 Reforms to the CRA should strengthen the engagement between banks and their communities and advance the law's core purpose of addressing disinvestment and unequal access to credit.

The ANPR that the Federal Reserve released today incorporates ideas from public comments on past rulemaking notices, research, and our discussions with the other banking agencies. Our proposal also reflects extensive outreach through the 29 CRA roundtables we held across the country with community and industry leaders and community members. I traveled to Colorado to participate in the first roundtable and to hear from women and minority small business owners about the loans that are enabling their businesses to thrive and the bankers who are providing credit and community development activities in their communities.11 I made similar visits to communities in areas ranging from El Paso's colonias to Kansas City, from Pine Ridge to Milwaukee, from the Mississippi Delta to Ferguson, Missouri, and from Hazard, Kentucky, to Rochester, New York. Despite wide variations, in all of these places, I met people working to strengthen their communities.

To ensure its continued effectiveness in supporting these efforts, the CRA regulation must evolve along with the landscape of banking and community development. To that end, the Board's ANPR seeks to advance the CRA's core purpose of addressing inequities in credit access and ensuring an inclusive financial services industry. In addition, the ANPR seeks to provide more certainty and consistency, tailor expectations to local conditions and bank business models, and minimize burden. Finally, we intend for the feedback on the ANPR to provide a foundation for the banking agencies to converge on a consistent regulatory approach that has broad support among stakeholders. Guided by these broad goals, I will discuss the key changes we are proposing.

Advancing the Core Purpose of the CRA

Promoting Financial Inclusion

We seek to modernize the CRA in a way that significantly expands financial inclusion. By being inclusive in their lending and investing, banks help their local communities to thrive, which in turn benefits their core business. The recognition of this mutually beneficial relationship between banks and their local communities is one of the core strengths of the CRA.

To strengthen the CRA's role in financial inclusion, the ANPR proposes to expand and clarify CRA-eligible activities that support minority depository institutions (MDIs), community development financial institutions (CDFIs), women-owned financial institutions, and low-income credit unions. Given the disproportionate impact of COVID-19 on communities of color, it is important to support the institutions that have a mission to serve the families, entrepreneurs, and homeowners in these communities. In May, Governor Miki Bowman and I heard from leaders of Federal Reserve-regulated MDIs about how COVID had hit their communities and the proactive efforts MDIs were taking to bolster their communities' resilience by extending credit to existing and new customers, calling each borrower that applied for a Paycheck Protection Program loan to help them navigate the process, and working with customers to modify and defer payments on existing loans.12 The Board's proposal would clarify that banks can receive credit for partnerships with MDIs and other mission-oriented institutions on a nationwide basis, and that such activities would be considered as part of a potential pathway to an "outstanding" rating. Furthermore, for regulated MDIs, investments in other MDIs and in their own institutions could be considered as enhancing their CRA performance.

Moreover, the ANPR proposes to designate certain areas, based on persistent inequities, where banks could receive credit for community development activities that often lie beyond the boundaries of a bank's branches. For instance, many of the places that I have visited, such as in the colonias, the Mississippi Delta, Appalachia, and Indian Country, have few bank branches and are located outside of branch-based assessment areas. Banks need to be confident about receiving CRA credit to seek out activities and investments in these areas.

The ANPR raises a variety of additional ideas that could be significant for financial inclusion. It proposes giving banks greater certainty that their community development activities will be considered in broader statewide and regional areas, in addition to activities within their local communities, so that banks could help address needs in "credit deserts" if they have the capacity to do so. In considering economic development, the ANPR considers that loans to the smallest businesses, smallest farms, and minority-owned small businesses might be considered impactful and responsive to community needs. In addition, the ANPR proposes elevating the focus on the availability of checking account and savings account products in serving LMI communities.

Finally, in considering how the CRA's purpose and history relate to the nation's current challenges, the Board seeks feedback on what other modifications and approaches would strengthen the CRA regulation in addressing systemic inequities in credit access for minority individuals and communities.

Meeting the Needs of LMI Individuals and Communities

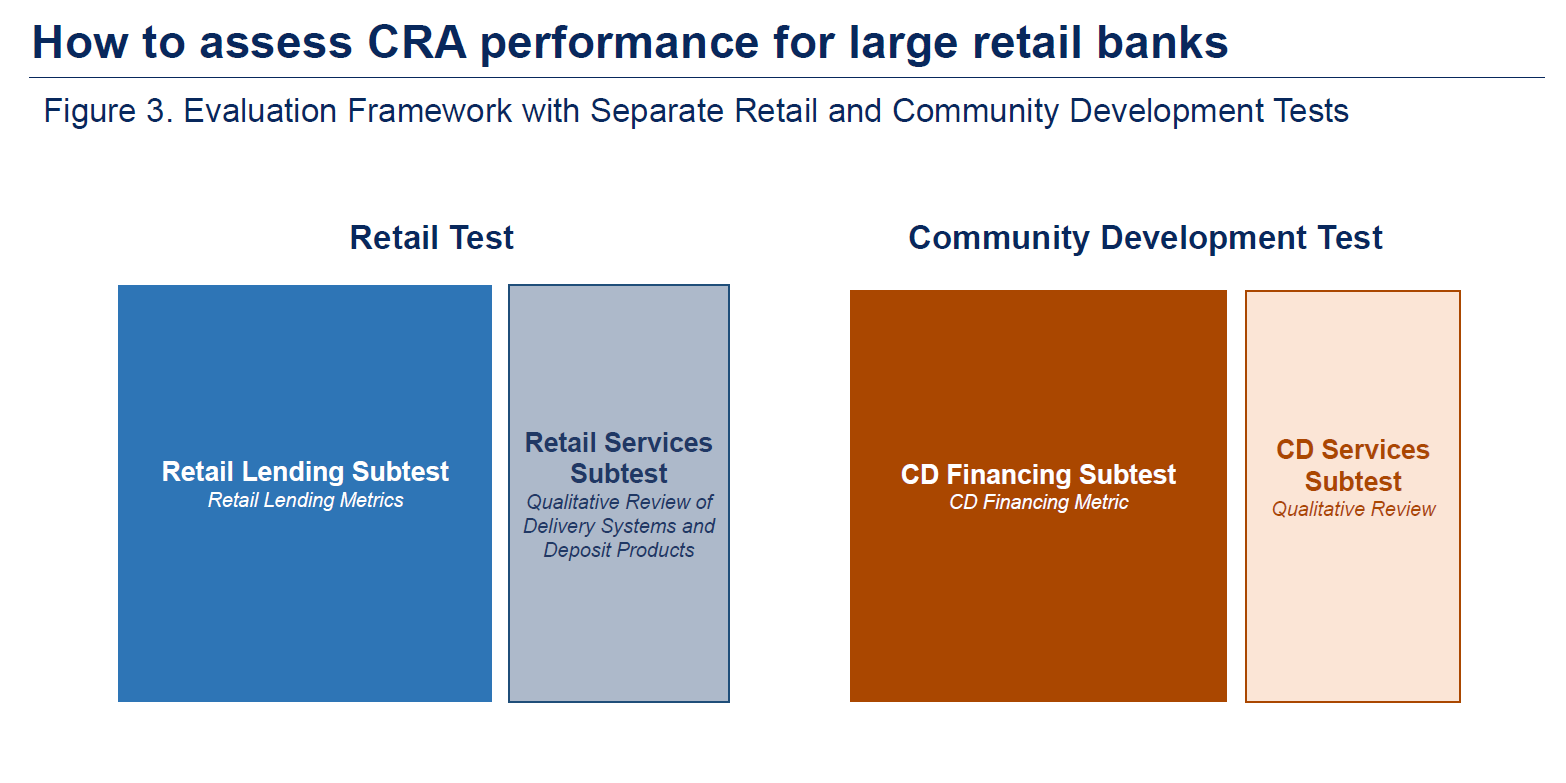

It is important for the CRA to ensure that a wide range of LMI banking needs are met. We heard from stakeholder feedback that both retail and community development activities are important in meeting LMI banking needs. Accordingly, we propose to assess large retail banks using a separate Retail Test and a Community Development Test with separate financing and services subtests (figure 3). Separate assessments of retail lending, retail services, community development financing, and community development services will support robust bank engagement with communities through a variety of channels.

{kind=link}

Stakeholder feedback has highlighted that each of these areas is essential to LMI communities. The standalone Retail Lending Test is important to stay true to the CRA's core focus on providing credit in underserved communities. Retail lending is the channel through which a family can get a mortgage to buy its first house and an entrepreneur can get a loan for a small business. Retail services are the channel through which an LMI household might get access to essential services from a local bank branch, such as a low-cost checking account. Community development financing captures bank lending and investments that create and maintain affordable housing, promote economic development, and revitalize and stabilize LMI communities. Community development services include financial counseling for low-income families and important volunteer activities undertaken by bank staff, such as serving on the board of a local nonprofit.

Some of these activities lend themselves primarily to a qualitative review. For example, the ANPR highlights essential banking services that are responsive to community needs, such as customer support that is provided in multiple languages and flexible branch hours to accommodate LMI customers' work schedules. Although we concluded that the value of services to a local community does not lend itself easily to a monetary value metric, the ANPR proposes introducing quantitative benchmarks where appropriate, such as indicators of whether branch locations are maintained or increased in underserved areas.

Addressing Changes in the Banking Industry

The ANPR proposes to modernize CRA assessment areas in recognition that reliance on mobile and internet banking has increased in the 25 years since the CRA regulation was last substantially revised. The ANPR still maintains a focus on branches, given their importance to individuals and communities. It also proposes to tailor the facility-based assessment area definition based on bank size.

For large banks that conduct a significant amount of lending and deposit-taking outside of their facility-based assessment areas, the ANPR presents options for determining where banks should be assessed outside of where their branches are located. Defining lending-based assessment areas is one option, but the preliminary analysis of this approach provided in the ANPR finds that banks' lending outside of their current assessment areas is widely dispersed and often occurs in places that are already well served. Defining deposit-based assessment areas is another option, but it would entail some additional data reporting burden, and we do not currently have the data to analyze this option closely. For internet banks, which lend across a broad area with few or no branch locations, a nationwide assessment area may advance the CRA's goals more effectively than the current practice of assessing these banks solely where they have a headquarters office.

Providing Certainty and Consistency, Minimizing Burden, and Tailoring Expectations

Providing Clarity, Consistency, and Transparency

The ANPR seeks to provide greater clarity and consistency through tailored performance evaluations. Responding to calls for greater certainty regarding how banks are assessed and rated, the ANPR introduces a metrics-based approach that is calibrated based on over 6,000 written public CRA evaluations.13 Separating the Retail Test and the Community Development Test provides greater scope to tailor the metrics to local market conditions, which often differ for retail lending and community development financing. This approach would create clear quantitative thresholds for the level of retail lending and community development financing that is needed to achieve a "satisfactory" CRA rating.

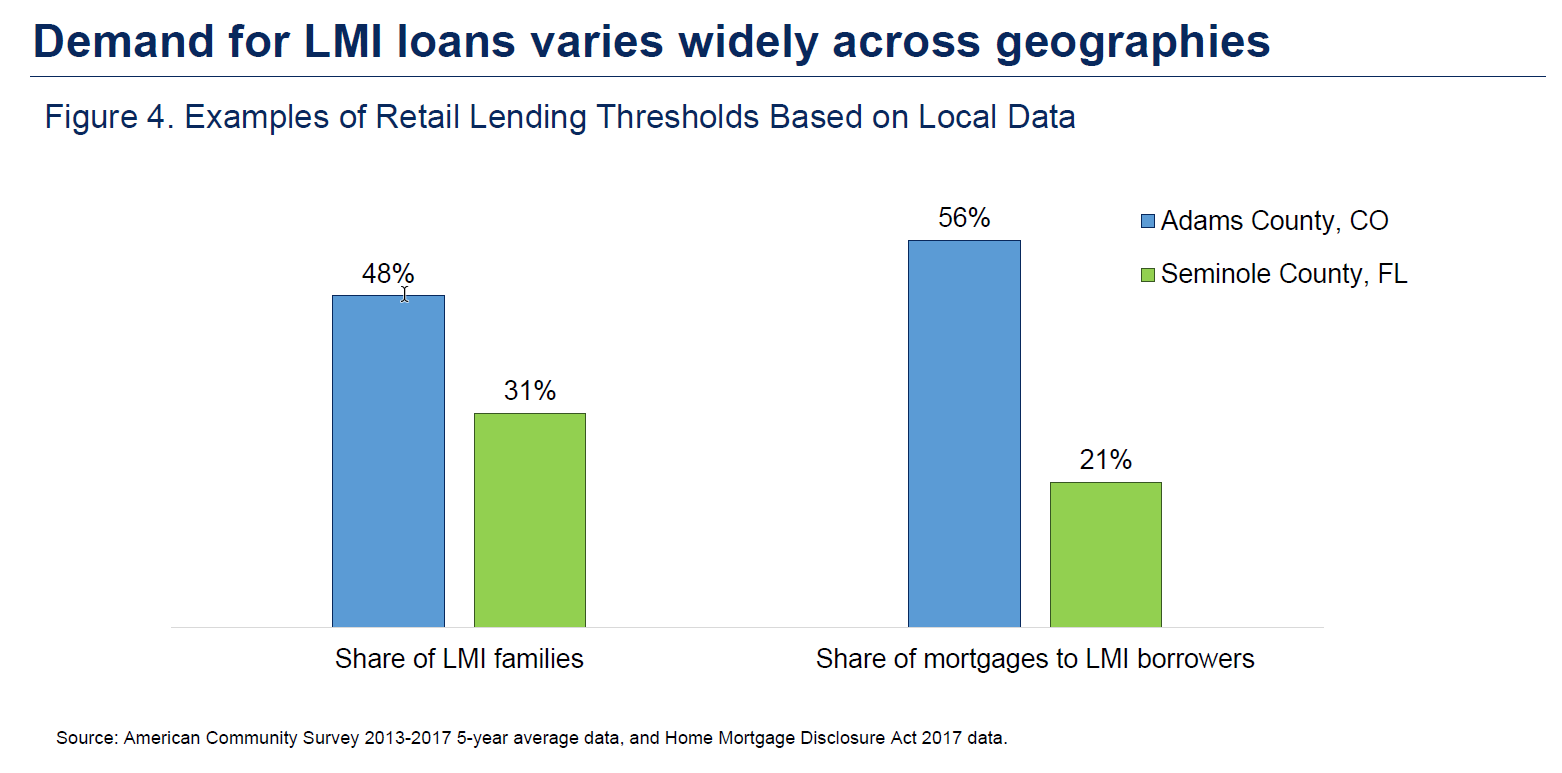

For the Retail Lending Subtest, which would apply to large retail banks and any small banks that choose to opt in, banks could earn a presumption of a "satisfactory" performance conclusion in an assessment area by reaching clear thresholds of lending to LMI borrowers and neighborhoods in each of their major product lines. The thresholds would be tailored to local market conditions and adjust automatically to reflect changes over the business cycle. They would be based on local data that reflect the credit needs and opportunities among LMI individuals, communities, small businesses, and small farms and on market data that reflect the level of LMI lending in the area by all lenders. Federal Reserve analysis confirms there are large differences in LMI lending opportunities among assessment areas, which illustrates the importance of tailoring the retail lending thresholds to the needs of the local community (figure 4). The ANPR also considers using the same metrics relative to performance ranges to produce a recommended Retail Lending Subtest conclusion of "outstanding," "satisfactory," "needs to improve," or "substantial noncompliance." We encourage commenters to make use of the CRA Analytics Data Tables that we published in March in order to evaluate the presumption threshold options and performance ranges and provide feedback.

{kind=link}

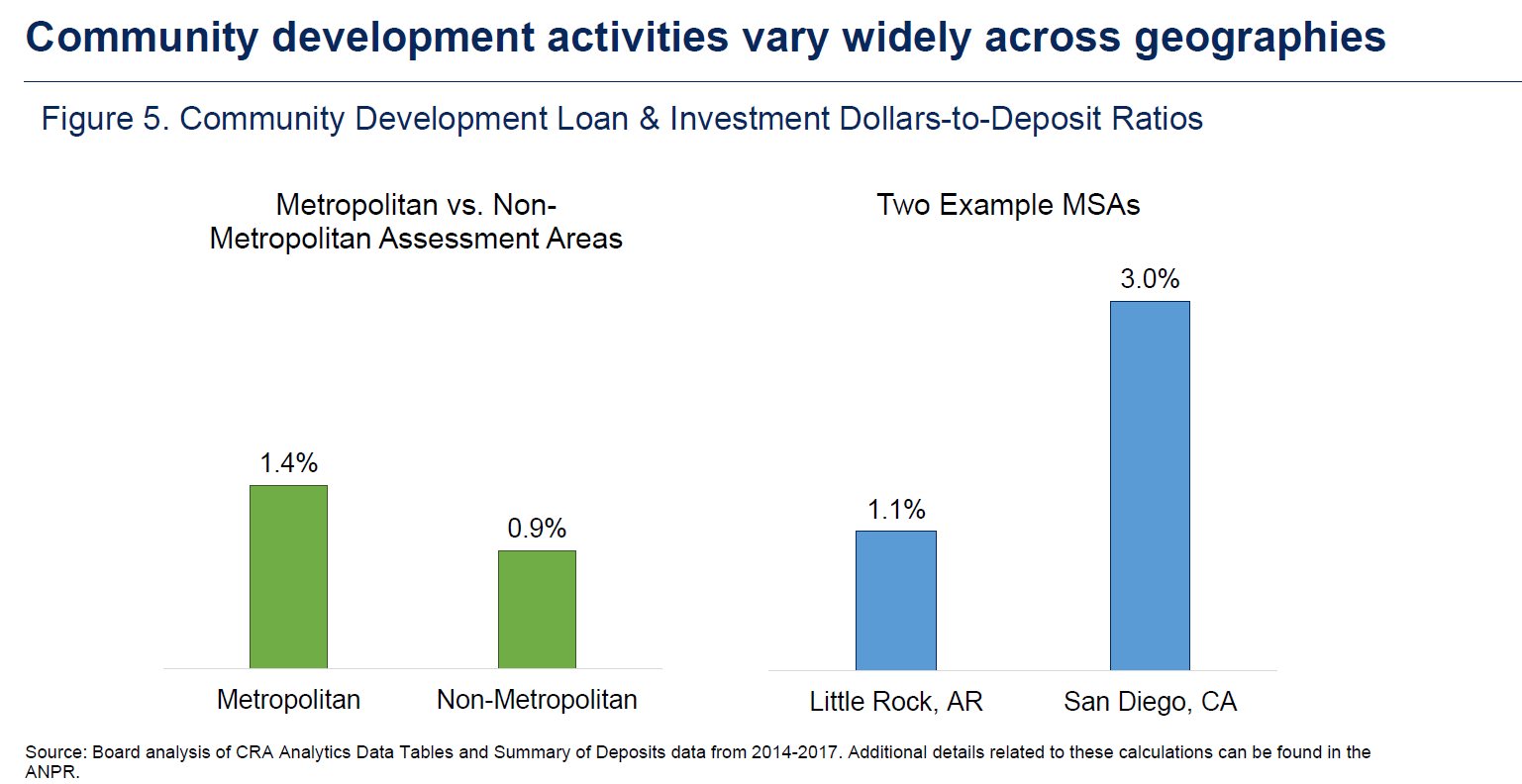

For the Community Development Financing Subtest, the Board is proposing to measure a large retail bank's community development loans and investments relative to its deposits in each assessment area. The thresholds for the Community Development Financing Subtest would be calibrated using local and national data. When we looked at past performance evaluations, we found that community development financing varies widely across different assessment areas, likely reflecting different levels of community development capacity and the unique needs and challenges of different communities. For example, in San Diego, California, the total dollar amount of banks' community financing activities relative to their deposits is three times higher than in Little Rock, Arkansas (figure 5). In addition, metropolitan areas overall have a higher level of community development financing relative to deposits than rural areas overall. For these reasons, it is important to tailor the Community Development Financing Subtest using thresholds that account for these differences and adjust automatically to changes over time.

{kind=link}

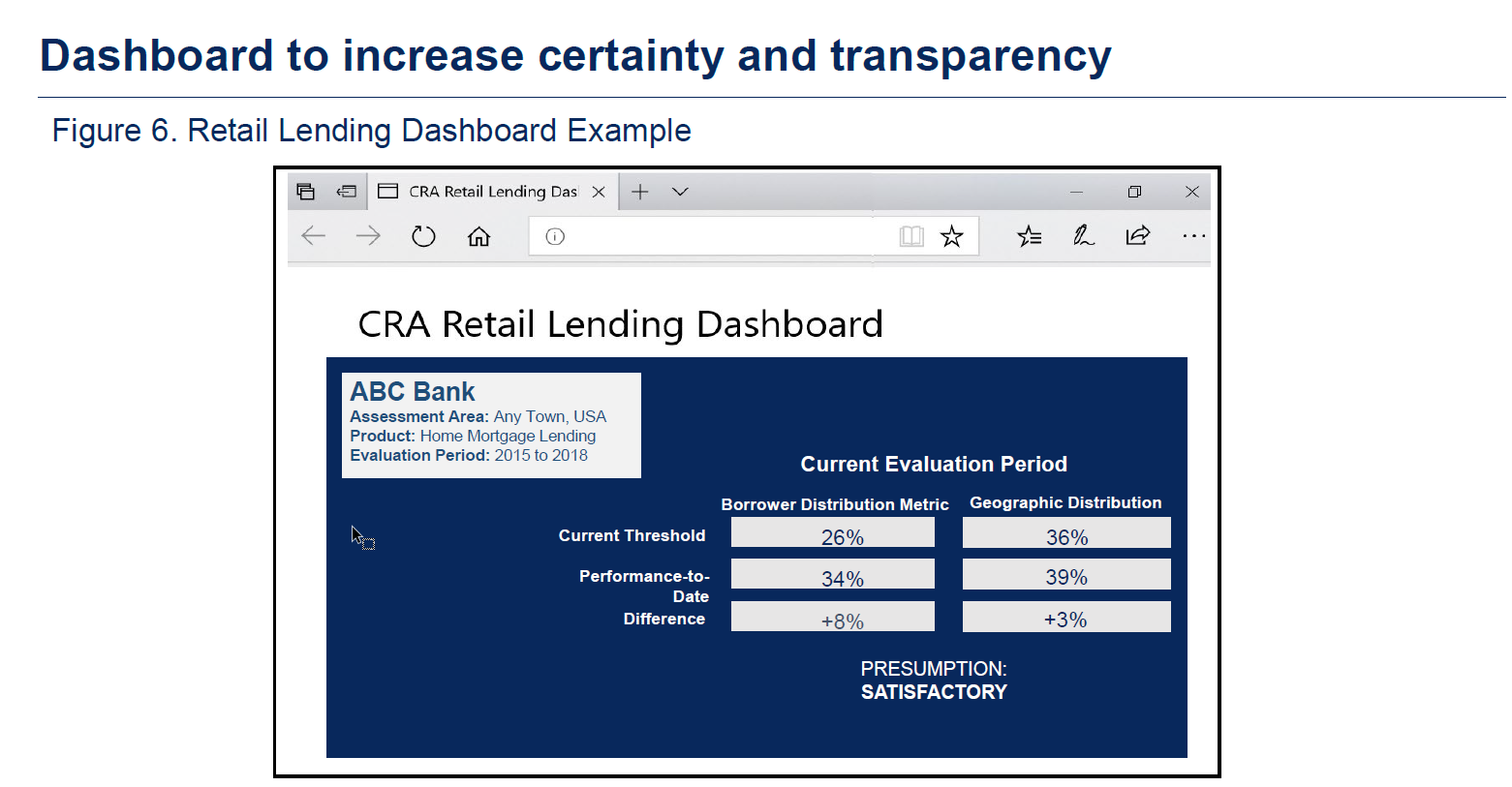

To provide certainty and transparency, the retail lending and community development financing thresholds would be made available in simple, regularly updated dashboards that banks could use to compare their level of activity to the thresholds in each assessment area (figure 6). For example, a dashboard for the Retail Lending Subtest could show the thresholds that a large retail bank should reach for each of its major product lines to receive the presumption of "satisfactory," including the percentage of loans to LMI borrowers and the percentage of loans to LMI neighborhoods.

{kind=link}

Tailoring Performance Evaluations to Bank Size and Business Model

The proposed separate subtests would also ensure expectations are tailored to the size and business models of different banks. It is important for smaller banks to be able to remain under the current more qualitative approach if they so choose. Accordingly, small retail banks could continue to be evaluated under the current CRA framework, but they would have the option to have their retail lending evaluated under the metrics-based Retail Lending Subtest. Small banks could also elect to have their retail services and community development activities evaluated.

Wholesale and limited purpose banks would be evaluated only on their community development activities. The ANPR solicits feedback on options for additional tailoring and flexibility for these institutions, which do not lend themselves to evaluation under the same metrics that would be applicable to large retail banks.

Minimizing Data Collection and Reporting Burden

The ANPR seeks comment on striking an appropriate balance between providing greater certainty for how banks are assessed through the increased use of metrics and minimizing the associated data collection and reporting burden. In an effort to reduce burden, the proposed metrics would rely to the greatest extent possible on existing data collections and public data sources, and the approach would exempt small banks from deposit and certain other data collection requirements.

Large banks currently report community development loans at an aggregated level. A bank may also share information with its examiner on its community development loans and investments in a specific assessment area during a CRA exam. However, the bank does not formally report data on these activities for each assessment area, nor are the data currently available through other sources. Without reporting data more consistently to provide the basis for comparison, it would be difficult to measure and evaluate a large bank's community development performance in a more consistent and predictable way.

Clarify and Expand Eligible CRA Activities to Focus on Communities

The ANPR proposes updating and clarifying which community development activities qualify in order to provide greater certainty to banks and communities about what counts. The ANPR proposes to publish and regularly update an illustrative, but not necessarily exhaustive, list of qualifying activities. To provide additional certainty, the Board also seeks feedback on a preapproval process, so that banks can propose a community development activity to their examiner to determine whether it will qualify before proceeding with the loan, investment, or service activity. This additional certainty could help promote greater investment by banks while retaining a focus on LMI communities.

In addition, the ANPR seeks feedback about clarifying the definitions of qualifying activities and broadening certain definitions in targeted ways. For example, the Board is considering defining CRA-eligible activities that create or preserve naturally occurring affordable housing and is considering whether to broaden the set of volunteer activities that would qualify in rural areas. The Board is also clarifying when a government or tribal plan is required to qualify activities that revitalize and stabilize communities. This is especially important in Indian Country, where we want to encourage banks to make impactful investments that have the support of tribal governments and to increase certainty about how these activities qualify for CRA credit.

Recognizing the Special Circumstances of Small Banks in Rural Areas

Stakeholder feedback emphasized that smaller retail banks play a vital role in many underserved communities, such as in rural areas. Accordingly, the ANPR provides small banks in rural areas operating in just a portion of a large county greater clarity and flexibility in tailoring the facility-based assessment area definition. The ANPR proposes that a small bank would not be required to expand the delineation of an assessment area to include parts of counties where it does not have a physical presence and where it either engages in a de minimis amount of lending or there is substantial competition from other institutions, except in limited circumstances. In addition, the ANPR proposes to revise the definition of community development services to include a wider range of volunteer activities to address the particular needs of rural areas.

The Path Ahead

It has been 25 years since the last significant revision to the CRA regulation, so it is important to get reform right. We are providing an extended 120-day comment period to allow ample time for thoughtful feedback from a broad set of stakeholders. The input from stakeholders thus far has been tremendously valuable, and we appreciate the care and concern expressed in the many comment letters and other forms of input on this important regulation. In the weeks and months ahead, we look forward to reviewing your comments and analyzing options for greater impact, including changes to address the inequities and challenges faced by minority communities and individuals. This feedback is critically important, and we are ready to listen.

Stakeholders have expressed strong support for the agencies to work together to modernize the CRA. By reflecting stakeholder views and providing a long period for public comment, the ANPR is intended to build a foundation for the banking agencies to converge on a consistent approach to strengthening the CRA that has broad support among stakeholders. With your continued ideas and engagement, I am confident we can come together on a stronger, transparent, and tailored approach to the CRA that will benefit LMI communities across the country for years to come.

1. I am grateful to Taz George of the Federal Reserve Bank of Chicago and Amanda Roberts, Joseph Firschein, and Carrie Johnson of the Federal Reserve Board for their assistance in preparing this text. These remarks represent my own views, which do not necessarily represent those of the Federal Reserve Board or the Federal Open Market Committee. Return to text

2. See Federal Reserve Board, "Advance Notice of Proposed Rulemaking: the Community Reinvestment Act," (September 21, 2020). Return to text

3. The Equal Credit Opportunity Act and the Fair Housing Act are fair lending laws that are designed to combat discrimination on prohibited bases such as race, and the Home Mortgage Disclosure Act is designed to bring transparency to mortgage lending practices. Return to text

4. See, e.g., Daniel Aaronson, Daniel Hartley, and Bhashkar Mazumder, "The Effects of the 1930s HOLC 'Redlining' Map," Working Paper No. 2017-12 (Chicago: Federal Reserve Bank of Chicago, revised August 2020). Return to text

5. Specifically, 46 percent of firms with non-Hispanic White ownership have obtained bank funds in the past five years, compared to 23 percent of firms with non-Hispanic Black ownership. See Federal Reserve System, Federal Reserve Small Business Credit Survey: 2020 Report on Employer Firms (2020), p. 3. Return to text

6. See Dionissi Aliprantis and Daniel Carroll, "What Is Behind the Persistence of the Racial Wealth Gap?" Economic Commentary, no 2019-03, February 28, 2019. See also Jung Hyun Choi, "Breaking Down the Black-White Homeownership Gap," Urban Wire: Housing and Housing Finance (blog), Urban Institute, February 21, 2020, which finds that the homeownership rate among White households is 30 percentage points higher than for Black households, and a large gap remains after controlling for differences in income levels. Return to text

7. See Lael Brainard, "Strengthening the Community Reinvestment Act by Staying True to Its Core Purpose" (speech at the Urban Institute, January 8, 2020). Return to text

8. The Census Household Pulse Survey indicates that 23 percent of non-Hispanic Black renters and 20 percent of Hispanic renters reported they were not caught up on their rent in August 2020, compared to 11 percent of non-Hispanic White renters. The Federal Reserve Board's Survey of Household Economics and Decisionmaking (SHED) indicates that one-fourth of workers in low-income families, with incomes below $40,000, who experienced a layoff said they had returned to work for the same employer by July, compared to 32 percent of middle-income and 39 percent of high-income workers, with incomes of between $40,000 and $100,000, and greater than $100,000, respectively. See also Federal Reserve System, FedListens: Perspectives from the Public, (Federal Reserve System, June 2020); Claire Kramer Mills and Jessica Battisto, "Double Jeopardy: COVID-19's Concentrated Health and Wealth Effects in Black Communities" (New York: Federal Reserve Bank of New York, August 2020); and Nishesh Chalise et al., Perspectives from Main Street: The Impact of COVID-19 on Low- to Moderate-Income Communities and the Entities Serving Them (Atlanta: Federal Reserve Bank of Atlanta, August 2020). Return to text

9. See Raphael Bostic, "A Moral and Economic Imperative to End Racism" Federal Reserve Bank of Atlanta (website), June 12, 2020. Return to text

10. See Raphael W. Bostic and Hyojung Lee, "Small Business Lending under the Community Reinvestment Act," Cityscape, 19, no. 2 (2017): 63-84. See also Hyojung Lee and Raphael W. Bostic, "Bank Adaptation to Neighborhood Change: Mortgage Lending and the Community Reinvestment Act," Journal of Urban Economics 116 (March 2020); and Lei Ding and Carolina K. Reid, "The Community Reinvestment Act (CRA) and Bank Branching Patterns," Housing Policy Debate 30, no. 1 (November 2019): 27-45. Return to text

11. See Lael Brainard, "Community Investment in Denver" (speech at the Federal Reserve Bank of Kansas City Denver Branch, October 15, 2018). Return to text

12. Minority Depository Institutions Leadership Forum via Webex with Governors Miki Bowman and Lael Brainard (May 13, 2020). Return to text

13. Federal Reserve staff created a database based on over 6,000 written public CRA performance evaluations from a sample of 3,700 banks of varying asset sizes, business models, geographic areas, and bank regulators. The database includes the location, number, and amount of CRA-eligible loans and investments and the ratings associated with each bank's performance from 2005 to 2017. See Federal Reserve Board, "CRA Analytics Data Tables," March 6, 2020. Return to text