July 10, 2024

Common Inflation and Monetary Policy Challenges across Countries

Governor Lisa D. Cook

At the Australian Conference of Economists 2024, Adelaide, Australia

Thank you, Jacky. I am happy to be here in Adelaide and appreciate the opportunity to speak with all of you.1 Considering the significant developments in the global economy over the past few years, now is an appropriate time to reflect on the economic reverberations the COVID-19 shock caused around the world. Examining the common inflation experiences and monetary policy challenges across several countries, including Australia and the United States, is a helpful exercise for policymakers and economists alike. Today, I will first talk about how monetary policymakers responded in similar fashion to the COVID-19 pandemic and, later, to high inflation during the recovery. I will discuss common features of the recent inflation experience across countries and the importance of global shocks. With disinflation in train across most countries, I will consider what we can learn from past cycles of monetary easing. I will finish with a discussion of how the use of alternative scenarios could help monetary policymakers communicate how they might respond to a range of possible economic outcomes.

Common Monetary Policy Response to the Pandemic

In the spring of 2020, economies around the world shut down or sharply limited business activity, especially for in-person services, including dining out and traveling. Governments introduced extraordinary fiscal support aimed at alleviating the socioeconomic effects of the pandemic. And, to prevent sharp financial and economic deterioration, most central banks responded aggressively by lowering policy rates, ramping up asset purchases, and taking other actions to support the flow of credit to households and businesses. Those efforts were sustained throughout 2020 and much of 2021, as the initial turmoil in financial markets subsided but the health situation remained uncertain.

{kind=link}

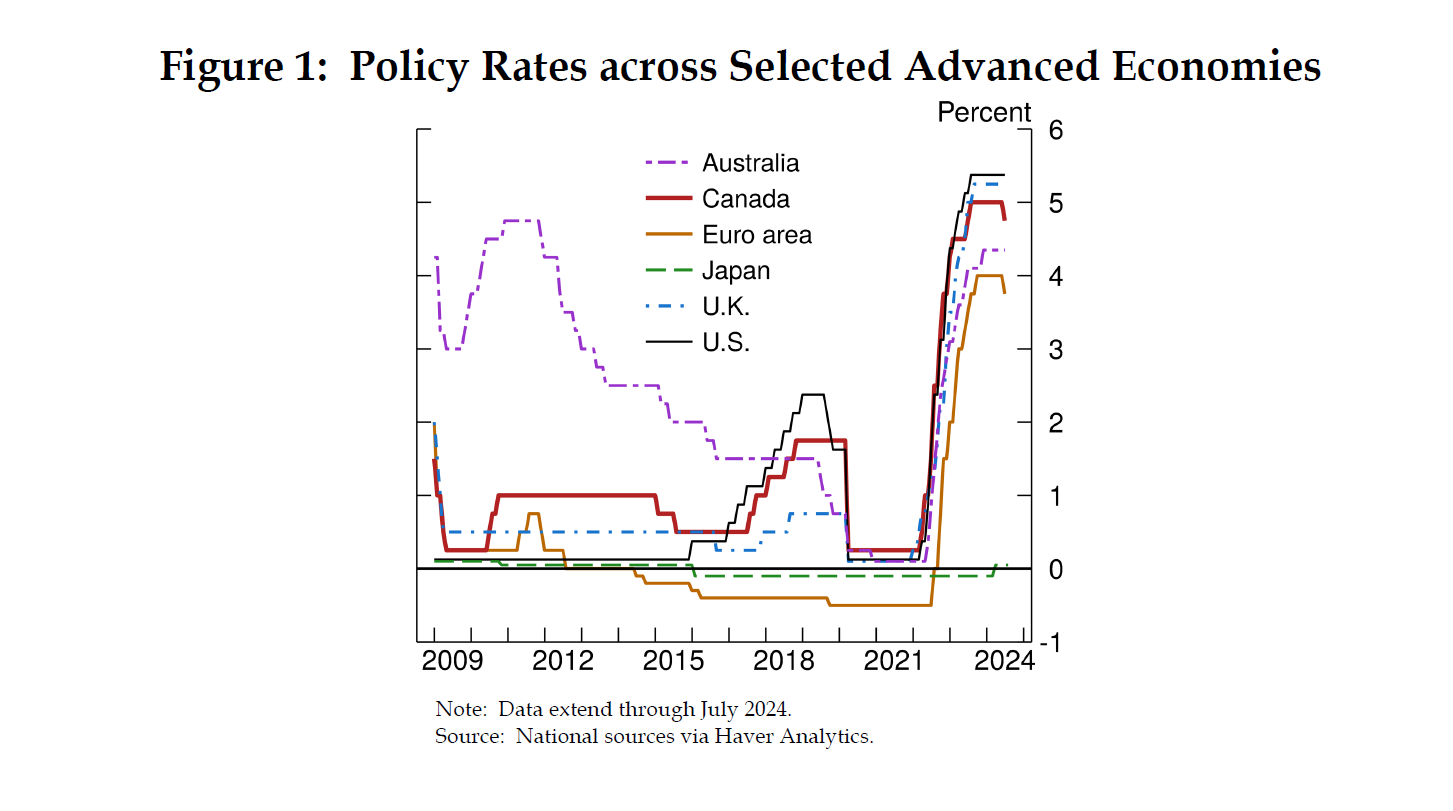

Advanced economy central banks that had positive policy rates before the pandemic, including the Fed and the central banks of Australia, Canada, and the United Kingdom, cut these rates to near zero, as shown in figure 1. Central banks that entered the pandemic with policy rates already at zero, such as Sweden, or negative—including the euro area, Japan, and Switzerland—left their rates unchanged. Meanwhile, almost all emerging market economy (EME) central banks cut their policy rates. Although central banks acted quickly to reduce rates, policymakers cited a few reasons to refrain from deeper cuts: Among EME policymakers, concerns were expressed that further lowering rates risked exacerbating capital outflows, while some advanced economy central banks commented that further rate cuts, particularly in negative territory, could harm banks' financial health or would provide little additional monetary stimulus.

{kind=link}

Many central banks also conducted significant asset purchases. These purchases were initially aimed at restoring market functioning and providing liquidity, but they also were seen as lowering long-term yields and easing broader financial conditions. The Fed and the Bank of England (BOE) restarted their purchases, while the European Central Bank (ECB) and the Swedish Riksbank increased the pace of their existing programs. And here, the Reserve Bank of Australia began asset purchases and introduced a target for the three-year government bond yield at the same level as its overnight rate.

The Rise of Inflation and the Common Monetary Policy Response

Over the course of 2021, as financial conditions improved, a strong recovery in consumer demand outpaced still constrained supply capacity in many countries, leading to production and transportation bottlenecks, which ultimately resulted in inflation. The surge in inflation was initially mostly concentrated in finished goods and commodities but later spread to services.2 As the economy started reopening with the lifting of lockdowns and rollout of vaccines, demand for services picked up. Similar to what played out with goods, the pickup in demand for services ran into a constrained supply of service workers. As services are more labor intensive than goods, and labor supply was still reeling from the consequences of the pandemic, the rebalancing of consumption from goods to services led to higher rates of inflation and nominal wage growth.

In response to rising inflation, central banks around the world started to remove some of the support that they provided during the height of the pandemic. As a first step, central banks let many of the emergency support programs—in which they had bought assets other than national government bonds—expire. Next, central banks generally began to taper their purchases of government securities and then to end net purchases late in 2021 or the first half of 2022.

Then some central banks began to raise interest rates. The first to do so were EME central banks that saw particularly sharp increases in inflation driven by exchange rate depreciation and by the surge in prices for food, which makes up a large part of the consumption baskets in their economies. Advanced economy central banks generally were more patient on raising interest rates in 2021, as inflation expectations in their economies were better anchored than in emerging economies. Among advanced economy central banks, the first to hike in the autumn of 2021 were central banks in Norway and New Zealand, whose economies had strong recoveries. The BOE first raised its policy rate in December 2021, citing a strong labor market and sharply rising inflation. The Bank of Canada and the Fed began to raise rates in March 2022, and the ECB first raised its deposit rate (from negative 0.5 percent to zero) in July 2022. Most advanced economy central banks undertook a sequence of policy actions in which they first began to raise their policy rates and later began to reduce the size of their balance sheets over time.

Understanding the Rise and Fall of Inflation in Recent Years

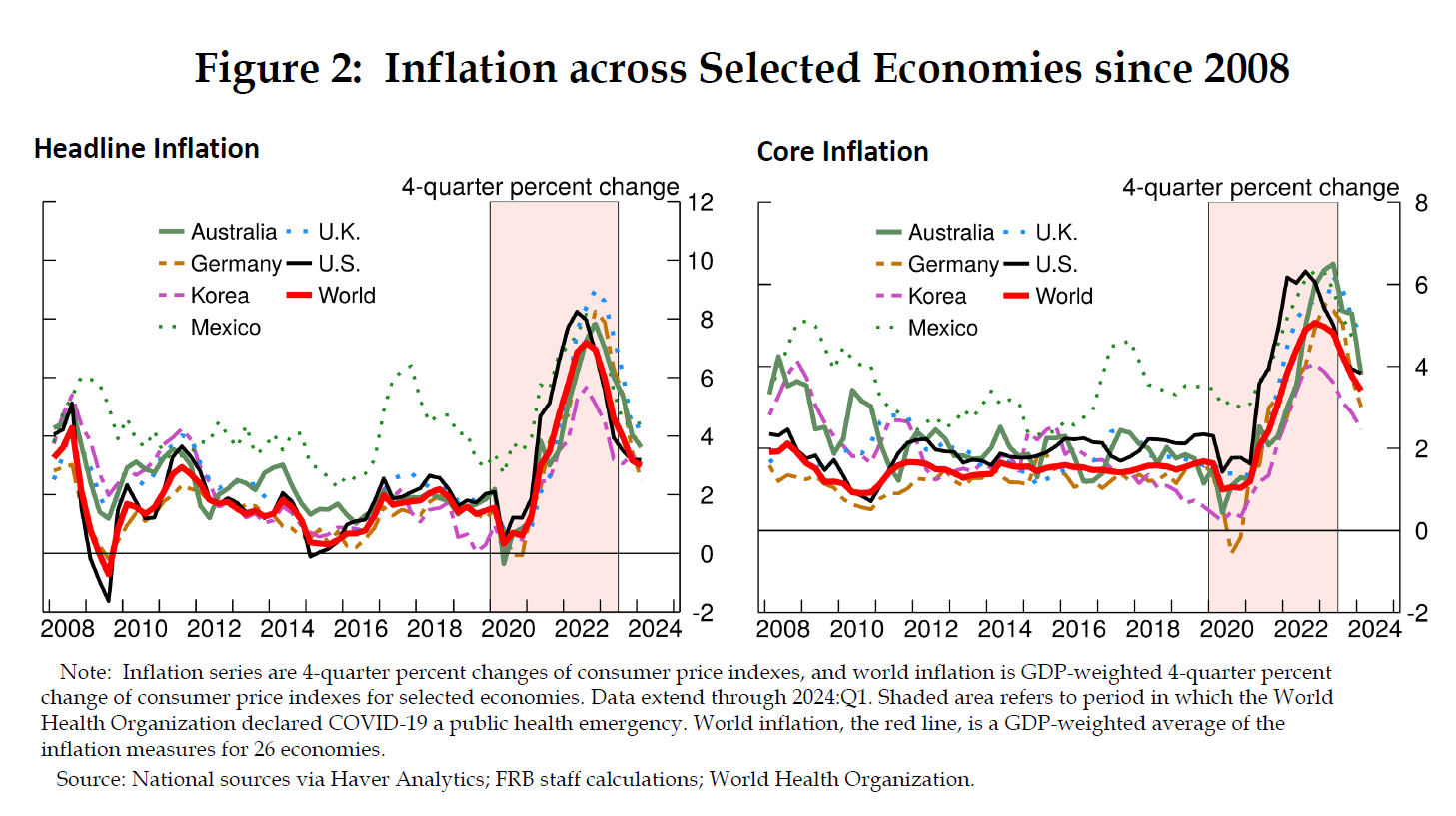

The inflation surge in the aftermath of the COVID-19 pandemic was synchronized across advanced and emerging economies, as figure 2 illustrates. The rapid increase in prices reflected an upswing in demand for goods, strained supply chains, tight labor markets, and sharp hikes in commodity prices exacerbated by Russia's February 2022 invasion of Ukraine. The run-up was not only for overall headline inflation, but also for its core components.

{kind=link}

A plethora of factors can explain the global co-movement in headline and core inflation. First, fluctuations in global food and energy prices broadly pass through to consumer prices in individual countries. But there are other possible explanations, including global supply constraints and synchronous policy responses. The pandemic experience was also a stark reminder of the importance of international trade and input-output linkages for the propagation of supply shocks—for example, production and shipping disruptions in the semiconductor industry in Asia constraining production and creating important price pressures in downstream markets, such as motor vehicles in the U.S.

Research on the recent inflation episode is still very much in its infancy, and I look forward to learning from the ongoing work on the subject. One important contribution already is Ben Bernanke and Olivier Blanchard's analysis of pandemic-era inflation in 11 economies. Separate teams for each of the 11 economies estimated a comparable model of inflation and its drivers. They find for the U.S. and, with some variation, for other countries that "relative price shocks and sectoral shortages drove the initial surge in inflation, but as these effects have reversed, tight labor markets in most (although not all) countries have become a relatively more important factor."3

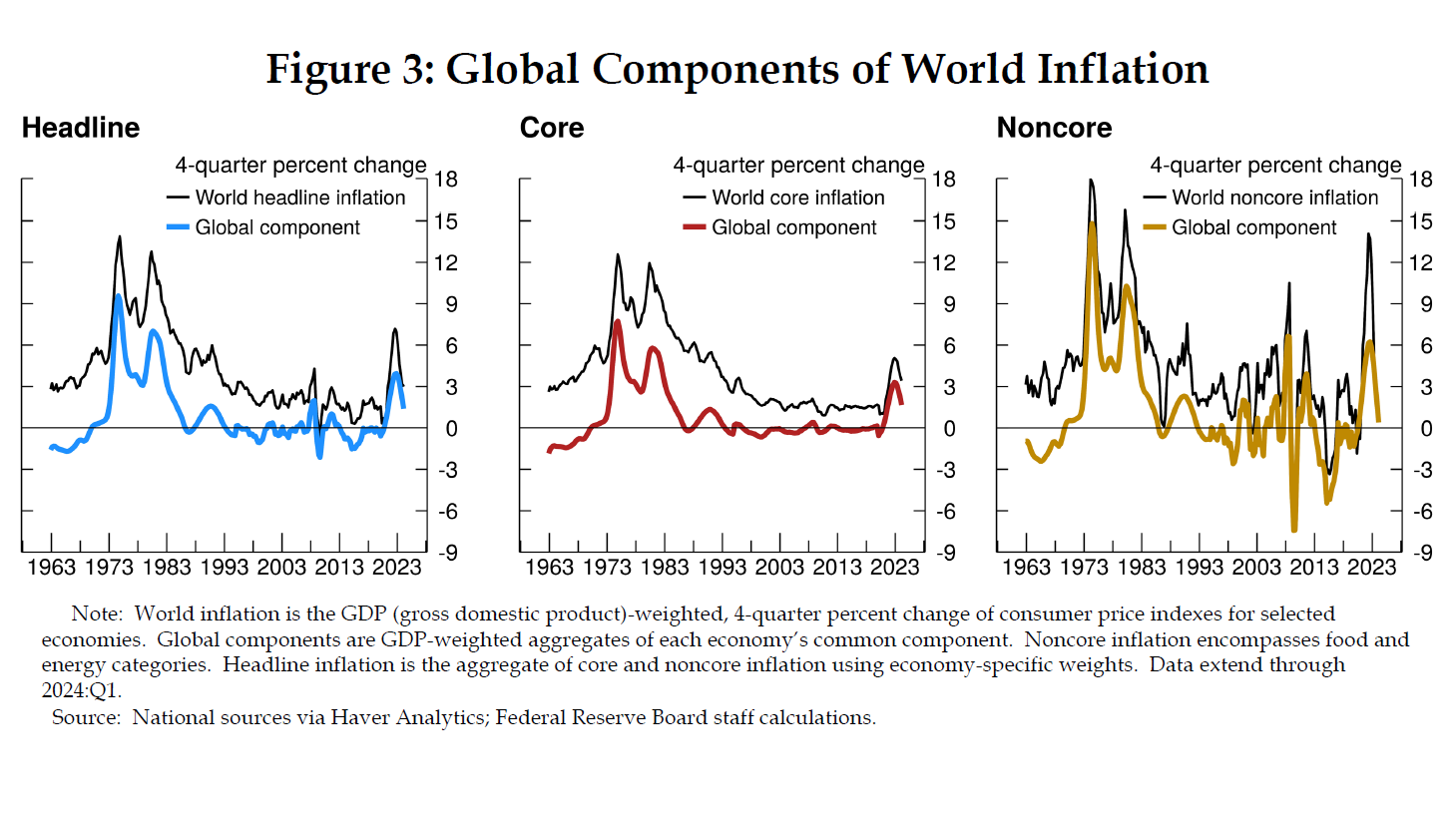

In a recent FEDS Notes article, economists at the Federal Reserve Board took head-on the task of decomposing world inflation into common and country-specific components and using this decomposition to analyze the sources of inflation around the world.4 Despite the different approach, they reached conclusions broadly in line with those of Bernanke and Blanchard. As shown in figure 3, they find that the global components of inflation accounted for a large part of the variation in the average inflation around the world during the post-COVID period. This is an experience with precedents during the oil price shocks of the 1970s and the 1980s.

{kind=link}

This study also found that the global components of inflation also predict the path of near-term inflation. Historically, once global components start moving, they maintain the course and take time to reverse. This persistence and the recent decline in global components of core and noncore inflation suggest that the world disinflationary process will continue, as shown in figure 4. The predicted path is in line with a gradual return of inflation toward central bank targets.

{kind=link}

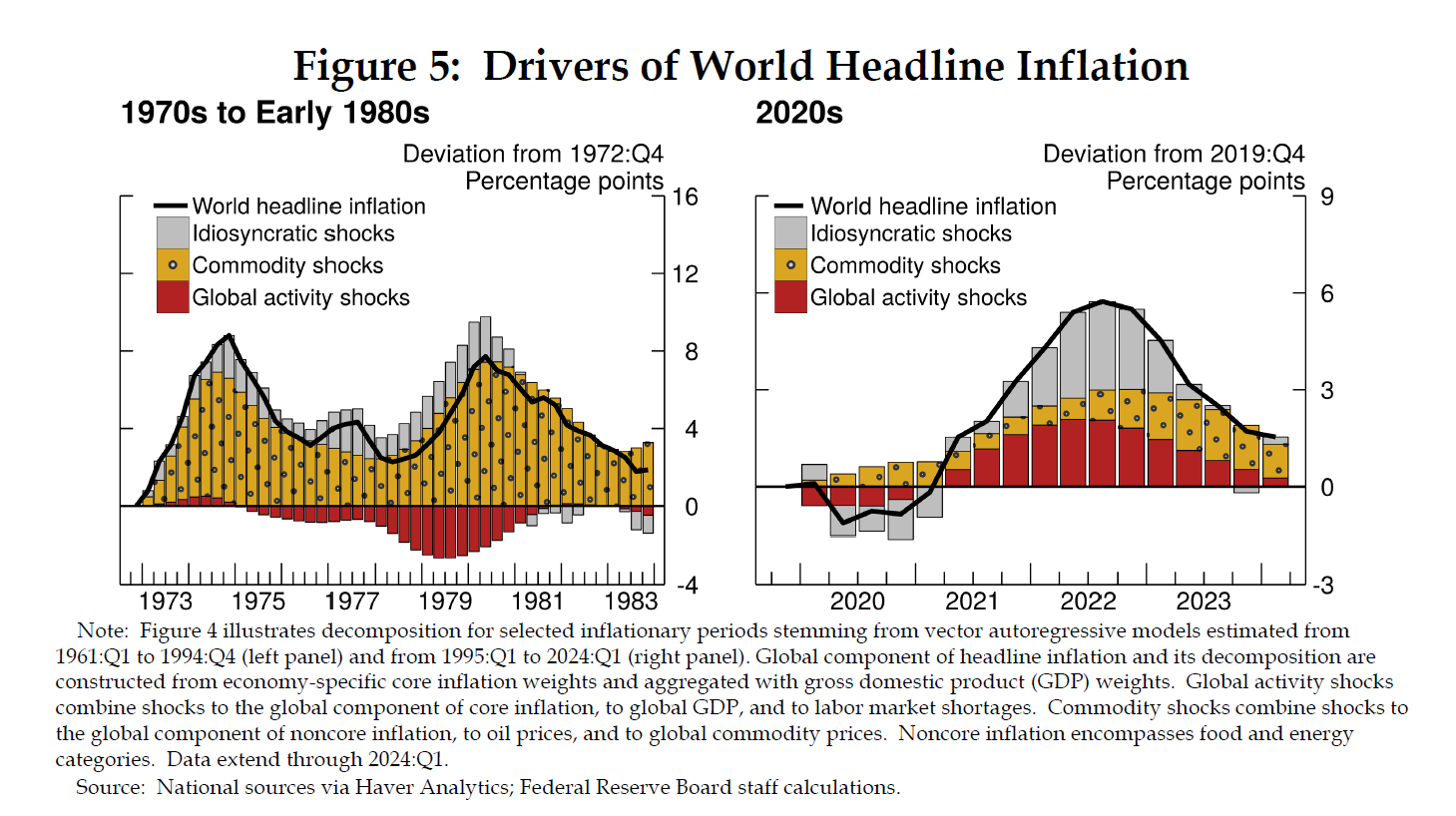

Of note, as shown in figure 5, the authors find that the post-pandemic rise in global inflation was linked to both commodity-driven price shocks and shocks to global economic activity—such as the sharp decline and rebound in activity due to the COVID‑19 pandemic and the associated labor market shortages. This situation contrasts with the 1970s and 1980s, when commodity price shocks played a prominent role in inflation's fluctuations. Additionally, idiosyncratic shocks were important drivers of the surge in global inflation in 2022 and its decline in 2023. These shocks may capture economy-specific forces, including natural gas disruptions that more greatly affected European economies than others in the aftermath of Russia's war on Ukraine.

{kind=link}

In sum, through the lens of the model, the ongoing disinflation is driven by waning effects of commodity price shocks and by a gradual normalization of global economic activity, amid the resolution of shortages and imbalances in labor markets.

Current Common Monetary Policy Challenges

With global components of inflation turning down, most countries have experienced a significant fall in inflation relative to its peak. Similarly, most central banks stopped raising their policy rates over the past year. Some are considering how long to keep rates at restrictive levels or, if inflation picks up again, whether to raise rates further. The Bank of Canada, the ECB, the Swedish Riksbank, and the Swiss National Bank, have begun to cut policy rates, highlighting progress toward meeting inflation goals amid sustained softness in economic activity. Indeed, unlike in the U.S., the level of gross domestic product (GDP) in some advanced economies remains well below what would be implied by their respective pre-COVID GDP trends.5 Even among those cutting rates, however, the future path of the policy rate is generally seen as dependent on a continuing decline of inflation toward target levels.

For all central banks, the question is how best to ensure continued disinflation while avoiding unnecessary damage to the economy. The generally desired outcome is a soft landing, in which inflation returns to the central bank's target inflation level or range without inducing a recession or a large increase in unemployment. How likely is such a scenario? It may be too soon to definitively say for the current economic cycle. But Fed Board staff have examined past episodes of monetary policy easing in 13 advanced economies over the past five decades. They find that soft landings are rare, according to their analysis published in another recent FEDS Notes article.6 In most of the cases that they studied, central banks were not successful in bringing inflation back to near target in a timely manner. And when they were successful in taming inflation, it often was associated with a recession.

However, soft landings are not unprecedented. When such a landing occurred, on average it was associated with a smaller preceding policy tightening. Soft landings were also more likely when policy easing began with inflation already close to target and when there was a relatively firm growth backdrop. In the U.S., what I have seen so far appears to be consistent with a soft landing: Inflation has fallen significantly from its peak, and the labor market has gradually cooled but remains strong. Of course, I am closely monitoring incoming data to see how the economy further develops.

It is possible that some features of the recent inflation episode may make a soft landing more likely in countries around the globe. As I discussed, Bernanke and Blanchard found that much of the inflation episode came from relative price shocks and sectoral shortages that have since been resolved. And while they found that tight labor markets have since taken over as the main drivers of inflation, there are signs that such tightness is easing. For instance, in the U.S., the ratio of vacancies to unemployment has fallen back to its pre-pandemic level and the rate of voluntary quits has declined, as workers are less confident of finding a better job. Thus, my baseline forecast (and that of many outside observers) is that inflation will continue to move toward target over time, without much further rise in unemployment.

Monetary Policy Communications

Of course, forecasts are subject to considerable uncertainty, and policymakers must consider a range of possible outcomes. A key challenge of monetary policy communications is discussing how policy would respond to changes in the economic outlook. Central bankers are faced with a tradeoff between predictability and flexibility. On the one hand, many observers would like to know in advance what the path for the policy rate will be, while, on the other hand, a central bank needs to remain nimble and data dependent. As a result, central bankers often try to convey their "reaction function" so observers understand how policy might adapt to incoming data and the implications for the economic outlook.

In his recent review of forecasting for monetary policymaking and communications at the BOE, Ben Bernanke suggested that the Bank consider supplementing its published forecasts with the use of alternative scenarios to help the public understand its policy reaction function.7 For similar reasons I try to incorporate a discussion of alternative scenarios in my own speeches. Fed policymakers, like those at many other central banks, also benefit from staff analysis using models to explore how the forecast would change relative to the baseline if certain assumptions are changed. The challenge is how to use such alternative scenarios in our official communications.

Policy communications are an area where we can learn a lot from what other central banks have done, and communication practices have developed over time. The BOE was an early innovator with its fan charts, which emphasized that its forecasts for GDP and inflation were subject to growing uncertainty the longer the time horizon. Of course, forecasts for economic variables need to be conditioned on some assumption of the path of policy rates. While early practice was to condition on unchanged rates or on the path of rates implied by market pricing, some central banks innovated by publishing their own forecasts for policy rates. This was originally done by the Reserve Bank of New Zealand and later by the Norges Bank and the Riksbank. Since 2012, the Federal Reserve's Summary of Economic Projections also includes the path of the policy rate that each policymaker "deems most likely to foster outcomes for economic activity and inflation that best satisfy his or her individual interpretation of the statutory mandate to promote maximum employment and price stability."8 I continue to take great interest in communications and other monetary policy practices by foreign central banks.

In conclusion, I think it is clear we have learned much from the experience of the past few years. I must stress that the human toll of the pandemic cannot and should not be overlooked. Purely in terms of economics, the recent period does stand out as an unusual case study. Economies around the world effectively faced the same shock at nearly the same moment. We were then able to observe how various economies around the world responded to the shock, including the actions of central banks and fiscal policymakers. I am glad to have highlighted some of the interesting research that has begun to explore this space, and I am sure much more study on this unique time in our history will soon occur, and that can be powerful. What is not unique to the pandemic is that we often have common macroeconomic experiences and face common monetary policy challenges, which is what makes discussions like the one today so valuable.

Thank you. It is a pleasure to be here in Adelaide. I look forward to continuing our conversation.

1. The views expressed here are my own and not necessarily those of my colleagues on the Federal Open Market Committee. Return to text

2. See François de Soyres, Alexandre Gaillard, Ana Maria Santacreu, and Dylan Moore (2024), "Supply Disruptions and Fiscal Stimulus: Transmission through Global Value Chains," AEA Papers and Proceedings, vol. 114 (May), pp. 112–17. Return to text

3. See Ben Bernanke and Olivier Blanchard (2024), "An Analysis of Pandemic-Era Inflation in 11 Economies (PDF)," Hutchins Center Working Paper 91 (Washington: Brookings Institution, May), quoted text on p. 1. Return to text

4. See Danilo Cascaldi-Garcia, Luca Guerrieri, Matteo Iacoviello, and Michele Modugno (2024), "Lessons from the Co-Movement of Inflation around the World," FEDS Notes (Washington: Board of Governors of the Federal Reserve System, June 28). Return to text

5. See François de Soyres, Joaquin Garcia-Cabo Herrero, Nils Goernemann, Sharon Jeon, Grace Lofstrom, and Dylan Moore (2024), "Why Is the U.S. GDP Recovering Faster Than Other Advanced Economies?" FEDS Notes (Washington: Board of Governors of the Federal Reserve System, May 17). Return to text

6. See François de Soyres and Zina Saijid (2024), "Lessons from Past Monetary Easing Cycles," FEDS Notes (Washington: Board of Governors of the Federal Reserve System, May 31). Return to text

7. See Ben S. Bernanke (2024), Forecasting for Monetary Policy Making and Communication at the Bank of England: A Review (London: Bank of England, April). Return to text

8. See the June 2024 Summary of Economic Projections (quoted text on p. 1), available on the Board's website at https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20240612.pdf. Return to text