FEDS Notes

Print

PrintMarch 24, 2015

The Federal Reserve's Overnight and Term Reverse Repurchase Agreement Operations in the Financial Accounts of the United States

Ralf R. Meisenzahl1

This note explains how the Federal Reserve's overnight and term reverse repurchase agreement (RRP) operations are reported in the Federal Reserve's Financial Accounts of the United States (formerly known as the Flow of Funds Accounts). Beginning with the March 2015 publication of the Financial Accounts, the securities repurchase transactions of the monetary authority, which include monetary authority repurchase agreements (RPs) and RRPs, will show, as separate line items (in tables F.109, link, and L.109, link), (1) RRP operations that have been conducted as part of the Federal Reserve's Overnight Reverse Repurchase Agreement Operational Exercise since September 2013, combined with term RRP operations that were first conducted in December 2014, and (2) other RPs and RRPs.2 The overnight and term RRP operations will be also appear as memo items on the federal funds and security repurchase agreements instrument tables (F.207, link, and L.207, link). Further details are provided below.

Background on the Federal Reserve's overnight and term RRP operations

Federal Reserve RPs and RRPs are conducted by the Open Market Trading Desk (the "Desk") at the Federal Reserve Bank of New York. In an RP transaction, the Desk purchases a U.S. government security from an eligible counterparty that agrees to repurchase the same security at a specified price at a specific time in the future. An RRP transaction is the opposite of an RP: The Desk sells a U.S. government security and agrees to repurchase it later. For an overnight RP / RRP, the time between the purchase and repurchase is one business day, while for term RPs / RRPs, the interval can be as many as 65 business days.

The Federal Open Market Committee (FOMC) first authorized the Desk to conduct a series of fixed-rate overnight RRP operations involving U.S. Government securities, including agency securities, in September 2013.3 The FOMC has indicated that it plans to use an overnight RRP facility to help control the federal funds rate during the monetary policy normalization process.4

The overnight RRP operational exercise started on September 23, 2013. Take-up was initially limited to $0.5 billion per counterparty, although this limit was raised to $1 billion a few days later. The limit was subsequently raised in a series of steps, and reached $30 billion per counterparty by late September 2014, when an aggregate limit of $300 billion was also imposed on each overnight RRP operation. The total number of eligible RRP counterparties has increased over the duration of the exercise from 140 in September 2013 to 164 in March 2015.5

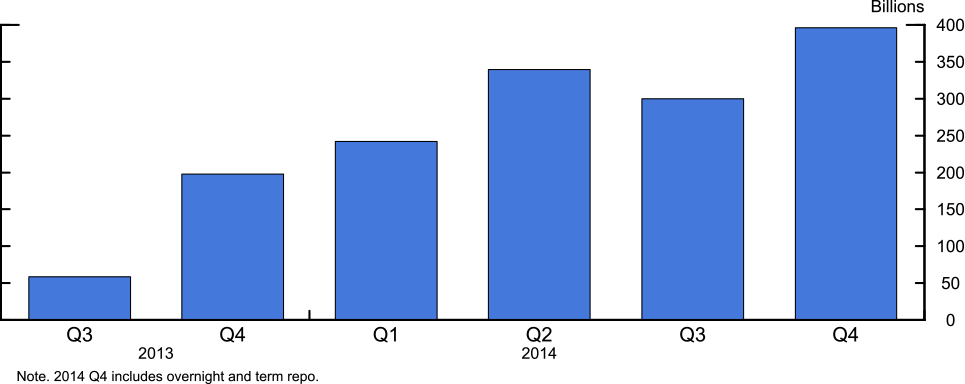

In October 2014, the FOMC authorized a series of term RRP operations with an aggregate limit of $300 billion to begin in December 2014 and mature in early January 2015.6 In January 2015, the FOMC authorized the Desk to conduct $200 billion of term RRPs over the March 2015 quarter-end.7 Figure 1 shows combined quarter-end take-up of overnight and term RRP (small amounts of term RRPs that were conducted in testing prior to the fourth quarter of 2014 are not included).

| Figure 1: Quarter-end Take-up in Federal Reserve RRP operations |

|---|

|

Source: Federal Reserve Bank of New York: http://www.ny.frb.org/markets/omo/dmm/historical/tomo/search.cfm.

Reporting overnight and term RRP operations in the Financial Accounts

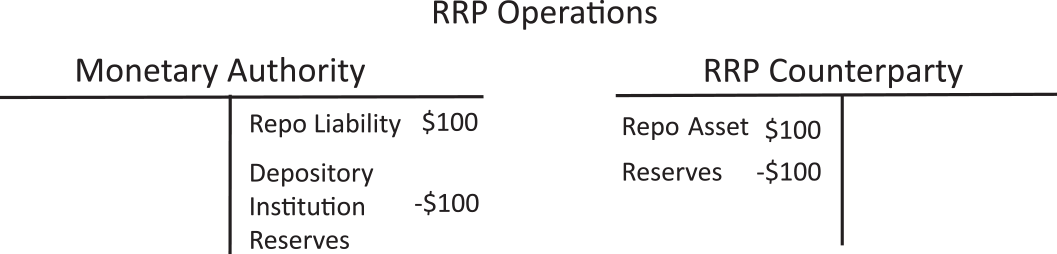

Figure 2 shows the effects of an RRP transaction on the monetary authority's and an RRP counterparty's balance sheets. The asset side of the monetary authority's balance sheet is unaffected; it continues to show the securities that have been sold temporarily under the RRP operations. The effect of the RRP is to shift the composition of the monetary authority's liabilities. Its RP ("repo") liabilities expand by $100 (recall that RPs are the opposite of RRPs). At the same time, its reserve liabilities--deposits held by banks and other depository institutions in their accounts at the Federal Reserve--decrease by $100. That is, when a counterparty lends cash to the Federal Reserve through RRPs, the Federal Reserve receives the cash by debiting the reserve account of the bank that clears the counterparty's trade. The RRP operational exercise therefore does not change the overall size of the monetary authority's balance sheet.

Starting with the March 2015 publication of the Financial Accounts of the United States, the balance sheet of the monetary authority (table L.109, link) includes two memo items under securities repurchase agreements. These items are (1) the combined amount of Federal Reserve liabilities in the overnight and term RRP operations as of the last day of each quarter, as shown in figure 1, and (2) Federal Reserve net liabilities under other RPs, which mostly have foreign official and international accounts as counterparties.

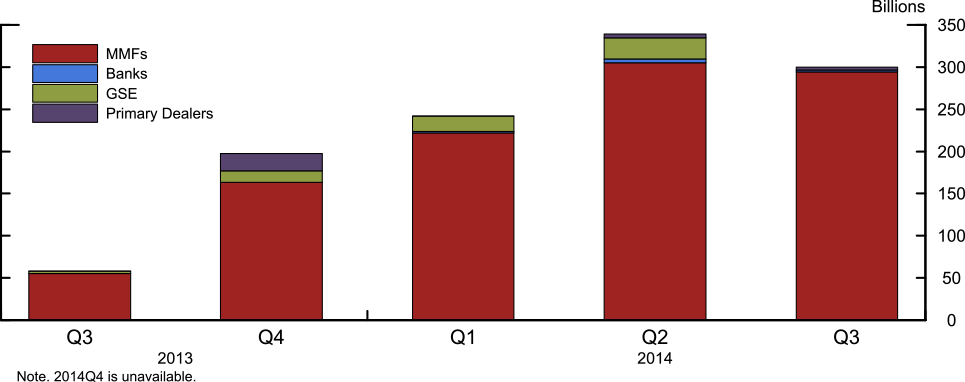

Eligible counterparties for Federal Reserve's overnight and term RRP operations include four types of financial institutions: primary dealers, banks (domestic and foreign banking offices in the United States), government-sponsored enterprises (GSE), and money market mutual funds. Figure 3 shows that the dominant type of counterparty for the quarter-end overnight RRP operations has been money market mutual funds.8

| Figure 3: Quarter-end RRP Take-up by Type of Financial Institution |

|---|

|

Source: Federal Reserve Bank of New York: http://www.newyorkfed.org/markets/omo/DMM/temp/file/Reverse%20Repo%20Data%20by%20Counterparty%20Type.xlsx.

In addition to the monetary authority sector table, The Financial Accounts of the United States also reports volumes of overnight and term RRP operations on the instrument table for Federal Funds and Security Repurchase Agreements (table L.207, link). On this table, the RRP operations appear as a memo item showing the monetary authority's RRP liabilities and money market funds' and other financial institutions' RRP assets.9

References

Frost, Josh, Lorie Logan, Antoine Martin, Patrick McCabe, Fabio Natalucci, and Julie Remache (2015). "Overnight RRP Operations as a Monetary Policy Tool: Some Design Considerations (PDF)," Finance and Economics Discussion Series 2015-010. Board of Governors of the Federal Reserve System (U.S.).

1. I would like to thank Brian Bonis, Jane Ihrig, Patrick McCabe, John McGowan, Maria Perozek, William Riordan and Paul Smith for helpful comments. Return to text

2. Other RPs and RRPs include those conducted with foreign official and international counterparties. Weekly Federal Reserve's balance sheet data, including all RPs and RRPs, are reported in the Federal Reverse's H.4.1 release (www.federalreserve.gov/releases/h41/Current/). Return to text

3. The Minutes from the September 2013 FOMC meeting, which report the first authorization of overnight RRP operations, can be found at www.federalreserve.gov/monetarypolicy/fomcminutes20130918.htm. In December 2014, the FOMC authorized overnight RRP operations until January 29, 2016 (www.federalreserve.gov/monetarypolicy/fomcminutes20141217.htm). For a detailed description of the RRP operational exercise, see Frost et al (2015). Return to text

4. See the FOMC's Policy Normalization Principles and Plans, published in September 2014, which can be found at www.federalreserve.gov/newsevents/press/monetary/20140917c.htm. Return to text

5. Lists of currently eligible counterparties is published by the Federal Reserve Bank of New York. The list of primary dealers serving as trading counterparties for the implementation of monetary policy can be found at www.newyorkfed.org/markets/pridealers_current.html. The expanded list of counterparties that are also eligible for participation in RRP operations can be found at www.ny.frb.org/markets/expanded_counterparties.html. Return to text

6. The FOMC authorization of the term RRP operations is included in the Minutes from the October 2014 FOMC meeting, available at www.federalreserve.gov/monetarypolicy/fomcminutes20141029.htm. Term RRP amounts can be retrieved from www.ny.frb.org/markets/omo/dmm/historical/tomo/search.cfm. Return to text

7. See www.federalreserve.gov/monetarypolicy/fomcminutes20150128.htm. Return to text

8. The Federal Reserve Bank of New York publishes the composition of the daily overnight RRP take-up data with a three month delay at www.newyorkfed.org/markets/omo/DMM/temp/file/Reverse%20Repo%20Data%20by%20Counterparty%20Type.xlsx. Return to text

9. Other include primary dealers, banks (domestic and foreign banking offices in the United States), and government-sponsored enterprises. Return to text

Please cite as:

Meisenzahl, Ralf (2015). "The Federal Reserve's Overnight and Term Reverse Repurchase Agreement Operations in the Financial Accounts of the United States," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, March 24, 2015. https://doi.org/10.17016/2380-7172.1510

Disclaimer: FEDS Notes are articles in which Board economists offer their own views and present analysis on a range of topics in economics and finance. These articles are shorter and less technically oriented than FEDS Working Papers.